Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Canadian Real Estate 2025 Why Nova Scotia’s Housing Market Outshines Major Cities

Canadian Real Estate 2025: Why Nova Scotia’s Housing Market Outshines Major Cities

The Canadian real estate landscape in 2025 tells a tale of two markets: while major metropolitan centers struggle with declining prices and buyer uncertainty, Nova Scotia and Atlantic Canada are emerging as the unexpected winners in the housing market. If you’re considering buying or selling property in 2025, understanding these regional differences could be the key to making smart real estate decisions.

Consider pairing this national overview with our long-term data deep dives in Ten Years of Nova Scotia Real Estate in Five Key Charts and Five Years of Nova Scotia Real Estate Market Analysis (2021–2025) to see exactly how Nova Scotia’s market has evolved over time.

Canada’s Housing Market Split: Winners and Losers in 2025

The Canadian housing market in 2025 is experiencing unprecedented regional divergence. Major urban centers that once drove national real estate trends are now facing significant challenges, while smaller markets across the Prairies and Atlantic Canada are posting remarkable gains.

For a province-by-province breakdown focused specifically on Nova Scotia, including price trends and units sold, see our Nova Scotia Housing Market 2025: Comprehensive Analysis.

Major Cities Face Reality Check

The Greater Toronto Area (GTA) and Metro Vancouver, traditionally Canada’s hottest real estate markets, are experiencing notable downturns. Toronto condo prices have plummeted nearly 12%, hitting their lowest levels since 2018. The situation is even more dramatic in suburban GTA markets, with Hamilton seeing a staggering 24% decrease in detached home prices.

Vancouver’s market tells a similar story, with Burnaby detached homes down 12% to $791 per square foot. This urban cooldown reflects broader economic uncertainty, trade tariff impacts, and a prevalent “wait and see” approach among both buyers and sellers.

For investors comparing these big-city slowdowns to Atlantic Canada’s trajectory, our long-run charts in Ten Years of Nova Scotia Real Estate in Five Key Charts offer valuable context on how Nova Scotia has performed versus major metros.

The Rise of Smaller Communities

In stark contrast, smaller markets across Alberta, Saskatchewan, Manitoba, and especially Atlantic Canada are experiencing explosive growth. Many of these markets are posting price increases in the 10–30% range, though their price per square foot remains significantly lower than major metropolitan centers.

Buyers looking for a closer look at Nova Scotia’s price, volume, and days-on-market shifts can dive into Five Years of Nova Scotia Real Estate Market Analysis (2021–2025).

Halifax Real Estate: Steady Growth in Uncertain Times

Halifax Housing Market Performance

Halifax, Nova Scotia’s largest city, continues to demonstrate remarkable resilience in the face of national market volatility. The city’s detached house price per square foot increased by 5.3% in 2024, reaching $436 per square foot. This growth maintains the substantial gains achieved during the significant 2021–2022 market surge.

The Halifax condo market shows a more nuanced picture, with prices dipping slightly by 1.3% to $461 per square foot. However, these prices remain near their all-time post-pandemic highs, indicating underlying market strength.

For a decade-long view of how Halifax fits within the broader provincial story, review the price and days-on-market trends in Ten Years of Nova Scotia Real Estate in Five Key Charts.

Why Halifax Appeals to Homebuyers

Halifax has established itself as a stable and appealing destination for several key reasons:

-

Affordability Advantage: Despite recent growth, Halifax remains significantly more affordable than Toronto or Vancouver, where average prices dwarf Atlantic Canadian markets.

-

Quality of Life: The city offers an attractive combination of urban amenities, natural beauty, and a more relaxed pace of life that appeals to buyers seeking work–life balance.

-

Economic Stability: Halifax’s diversified economy, including strong sectors in technology, healthcare, and education, provides employment stability that supports housing demand.

If you want Halifax-specific surprises and neighbourhood insights beyond the numbers, check out articles like your Halifax-focused market insights (for example “Halifax Real Estate Market Insights: 4 Surprises” if published) linked from the main C21 Optimum Realty blog.

Atlantic Canada’s Real Estate Boom

Record-Breaking Growth in New Brunswick

The Atlantic Canada real estate story extends well beyond Nova Scotia. New Brunswick markets are posting exceptional gains, with Saint John recording a remarkable 32.3% increase in detached home prices, while Fredericton saw 26.5% growth. These double-digit increases reflect strong regional momentum and growing recognition of Atlantic Canada’s value proposition.

For a side-by-side look at how Nova Scotia’s performance compares to these regional neighbours, the visualizations in Ten Years of Nova Scotia Real Estate in Five Key Charts are a useful starting point before you drill into other provinces.

Continued Affordability Despite Growth

Even with significant price increases, Atlantic Canadian markets like Charlottetown and St. John’s remain among Canada’s most affordable metropolitan areas. This continued affordability acts as a powerful magnet for buyers from other provinces seeking better value for their housing dollar.

Nova Scotia’s role in this affordability story is explored in more depth in Nova Scotia Housing Market 2025: A Comprehensive Analysis of Home Prices and Trends.

Migration Trends Driving Market Changes

Pandemic-Era Movement Continues

The trend toward seeking more affordable, livable communities outside traditional urban hubs, which accelerated during the pandemic, shows no signs of slowing. Buyers are increasingly prioritizing:

-

Lower cost of living

-

Better quality of life

-

More space for their money

-

Reduced urban stress

For a data-backed look at how these preferences translated into actual sales and price movements from 2021–2025, refer to Five Years of Nova Scotia Real Estate Market Analysis.

Out-of-Province Interest Remains Strong

Local real estate agents throughout Atlantic Canada report sustained interest from buyers outside the region. Many are seeing a surge in activity, particularly in summer months, with buyers attracted by Nova Scotia’s stable growth history and lifestyle appeal.

These migration and demand patterns are also reflected in the long-run “units sold” and “value of solds” charts in Ten Years of Nova Scotia Real Estate in Five Key Charts.

Market Opportunities and Investment Insights

For Homebuyers

-

Halifax Market: Represents an opportunity for buyers seeking long-term value in a stable, growing market. The city offers the amenities of a major center while maintaining relative affordability.

-

Condo Market Adjustment: The slight cooling in Halifax condo prices may present opportunities for buyers as new inventory emerges and the single-family market stabilizes.

-

Atlantic Canada Value: The region continues to offer exceptional value compared to major Canadian cities, with strong appreciation potential as migration trends persist.

If you’re evaluating timing, the five-year performance and current days-on-market data in Five Years of Nova Scotia Real Estate Market Analysis can help you understand whether now aligns with your strategy.

For Sellers

-

Timing Advantage: Sellers in Nova Scotia and Atlantic Canada are operating from a position of strength, with sustained buyer interest and limited inventory in many markets.

-

Market Stability: Unlike volatile major markets, Atlantic Canadian real estate offers more predictable selling conditions.

To see how today’s conditions compare to peak 2021–2022 seller leverage, review the sold-to-ask ratio trends in Ten Years of Nova Scotia Real Estate in Five Key Charts.

Economic Factors Shaping the Market

National Economic Headwinds

Several factors are contributing to the mixed national real estate picture:

-

Economic uncertainty affecting buyer confidence

-

Trade tariff impacts on major markets

-

Interest rate considerations

-

Employment market changes

For how these national headwinds played out specifically in Nova Scotia’s 2025 numbers, see Nova Scotia Real Estate Market Statistics 2025: A Year of Transition.

Regional Economic Strengths

Atlantic Canada’s relative isolation from some national economic pressures, combined with growing recognition of the region’s lifestyle and economic advantages, continues to support housing demand.

Our article on the federal response, “Canada’s Government Housing Strategy: Lessons from International Success Stories and What It Means for Nova Scotia” (linked on the C21 Optimum Realty homepage), explores how policy changes may further shape the region’s trajectory.

Looking Ahead: 2025 Market Predictions

Continued Regional Divergence

The split between major urban centers and smaller markets is likely to persist throughout 2025. Atlantic Canada’s momentum appears sustainable, supported by:

-

Ongoing migration trends

-

Relative affordability

-

Quality of life advantages

-

Economic diversification

For how these themes extend into 2026 and beyond, the concluding sections of Five Years of Nova Scotia Real Estate Market Analysis outline expectations for price growth and sales volumes.

Investment Considerations

For real estate investors and homebuyers, the data suggests Atlantic Canada, particularly Nova Scotia, offers compelling opportunities. The combination of steady growth, relative affordability, and strong lifestyle appeal positions the region well for continued success.

Investors who want to see the long-run wealth-building impact visually can reference the equity example in Ten Years of Nova Scotia Real Estate in Five Key Charts, where a 2017 buyer’s potential equity gain is quantified.

Conclusion: Nova Scotia’s Real Estate Advantage

As Canada’s real estate market navigates uncertainty in 2025, Nova Scotia and Atlantic Canada stand out as beacons of stability and opportunity. Halifax’s steady 5.3% growth, combined with the region’s broader appeal to out-of-province buyers, suggests this trend will continue.

Whether you’re a first-time homebuyer, looking to relocate, or considering real estate investment opportunities, Nova Scotia’s housing market offers the rare combination of growth potential and affordability that has become increasingly scarce in Canada’s major metropolitan areas.

The numbers don’t lie: while Toronto and Vancouver grapple with declining prices and market uncertainty, Atlantic Canada is writing a different story – one of steady growth, sustainable appreciation, and genuine opportunity for those smart enough to recognize it.

Looking to explore Nova Scotia’s real estate opportunities? Connect with local agents who understand the market dynamics and can help you navigate this exciting regional growth story by reaching out to the team at Century 21 Optimum Realty.

GST Relief for First-Time Home Buyers in Canada

GST Relief for First-Time Home Buyers in Canada: A Game-Changer for New Homeowners

The Canadian housing market has long been a significant barrier for first-time buyers, with high prices and additional costs making homeownership seem out of reach for many young Canadians. However, the federal government has introduced a groundbreaking initiative that promises to change the landscape: the First-Time Home Buyers’ GST Rebate (FTHB GST Rebate). This comprehensive relief measure is designed to make homeownership more accessible while simultaneously stimulating new home construction across the country.

What Is the First-Time Home Buyers’ GST Rebate?

The FTHB GST Rebate represents one of the most significant tax relief measures for homebuyers in recent Canadian history. This program allows eligible first-time home buyers to recover up to $50,000 of the Goods and Services Tax (GST) or the federal portion of the Harmonized Sales Tax (HST) paid on new homes.

The scope of this initiative is substantial, with the government projecting it will deliver $3.9 billion in tax savings to Canadians over five years, beginning in the 2025-26 fiscal year. This significant investment demonstrates the federal government’s commitment to addressing housing affordability challenges and supporting Canadians in achieving their homeownership dreams.

Who Qualifies for the FTHB GST Rebate?

Understanding the eligibility criteria is crucial for potential applicants. To qualify for the FTHB GST Rebate, buyers must meet several specific requirements:

Age and Residency Requirements:

- Must be at least 18 years old

- Must be a Canadian citizen or permanent resident

First-Time Buyer Status: The most critical requirement involves proving first-time buyer status. Applicants must not have owned or lived in a home owned by themselves, their spouse, or their common-law partner during the calendar year of purchase or the four preceding years. This five-year lookback period ensures the rebate targets genuine first-time buyers rather than those who have recently sold properties.

Property Types Covered: The rebate applies to various types of new housing arrangements, including:

- New homes purchased directly from builders

- Owner-built homes (whether built by the buyer or through hiring a builder)

- Shares in cooperative housing corporations where the co-op paid GST/HST on new housing

How the Rebate Structure Works

The FTHB GST Rebate operates on a tiered system based on the home’s purchase price, ensuring maximum benefit for buyers in different price ranges:

Full Rebate (100% GST Recovery): First-time buyers purchasing new homes valued up to $1 million receive a complete rebate of all GST paid. For a $800,000 home, this means recovering the full $40,000 in GST, representing substantial savings that can significantly impact affordability.

Partial Rebate (Linear Phase-Out): For homes priced between $1 million and $1.5 million, the rebate phases out linearly. For example, a buyer purchasing a $1.25 million home would receive a 50% rebate, recovering up to $25,000 in GST. This graduated approach ensures that buyers in higher price brackets still receive meaningful benefits while targeting maximum relief to those purchasing more moderately priced homes.

No Rebate: Homes valued at $1.5 million or more are not eligible for the rebate, focusing the program’s benefits on first-time buyers purchasing in more accessible price ranges.

Important Conditions and Timeline Requirements

Several critical conditions govern the FTHB GST Rebate that potential buyers must understand:

Purchase Agreement Timing: The agreement of purchase and sale must be entered into on or after May 27, 2025, and before 2031. This six-year window provides ample opportunity for eligible buyers to take advantage of the program.

Construction Timeline: For the rebate to apply, construction must begin before 2031 and be substantially completed before 2036. These timelines ensure the program stimulates new construction while providing reasonable completion deadlines.

Lifetime Limitation: The rebate can only be claimed once in a lifetime per individual. Additionally, if a spouse or common-law partner has already claimed the rebate, the other partner cannot claim it separately. This prevents double-dipping while ensuring each household can benefit once.

Assignment Restrictions: The rebate is not available if the original purchase agreement was entered into before May 27, 2025, even if the agreement is subsequently assigned to a first-time buyer. This prevents retroactive claims and ensures the program applies only to new transactions.

Cooperative Housing Exceptions: The rebate is not available for cooperative housing shares if the cooperative housing already qualifies for the 100% GST rebate for purpose-built rental housing, preventing double benefits.

Why This Initiative Matters for Canadian Homebuyers

The FTHB GST Rebate addresses several critical challenges in the Canadian housing market:

Reducing Upfront Costs: For many first-time buyers, the GST represents a significant additional cost that can strain already tight budgets. By recovering up to $50,000 in GST, buyers can redirect these funds toward down payments, moving costs, or home improvements, making the overall purchase more manageable.

Encouraging New Construction: By applying specifically to new homes, the rebate incentivizes construction companies to build more housing units. This increased supply can help address Canada’s housing shortage while providing buyers with modern, energy-efficient homes.

Supporting Market Entry: The program specifically targets first-time buyers, helping young Canadians and newcomers enter the housing market. This support is crucial for building long-term wealth and stability for Canadian families.

Maximizing Your Benefit: Key Considerations

To make the most of the FTHB GST Rebate, potential buyers should:

Plan Your Timeline: Ensure your purchase agreement falls within the eligible timeframe and that construction can be completed within the required deadlines.

Verify Eligibility: Carefully review the five-year ownership history requirement and ensure you meet all citizenship and age requirements.

Consider Home Value: Understanding the rebate structure can help you make informed decisions about your price range and potential savings.

Consult Professionals: Work with qualified real estate professionals, tax advisors, and legal counsel to navigate the application process and ensure compliance with all requirements.

Special Impact for Nova Scotia Home Buyers

Nova Scotia presents unique opportunities for first-time home buyers to maximize the benefits of the FTHB GST Rebate. The province’s housing market characteristics make this federal initiative particularly advantageous for Maritime buyers.

HST Considerations in Nova Scotia: Nova Scotia uses the Harmonized Sales Tax (HST) at 15%, which includes the 5% federal GST component. The FTHB GST Rebate applies to the federal portion of the HST, meaning Nova Scotia buyers can recover 5% of their new home’s purchase price (up to the $50,000 maximum). For a typical $400,000 new home in Halifax, this represents $20,000 in savings—a substantial amount that can significantly impact affordability in the region.

Market Advantages: Nova Scotia’s relatively more affordable housing market compared to Ontario and British Columbia means more homes fall within the full rebate range. With average new home prices in many Nova Scotia communities under $500,000, buyers can often access the complete 5% GST rebate, maximizing their benefit from this federal program.

Supporting Local Construction: The rebate’s focus on new construction aligns well with Nova Scotia’s growing population and increased demand for housing. The province has experienced significant in-migration in recent years, and this federal incentive could help stimulate new home construction to meet growing demand while providing relief to local first-time buyers.

Combined with Provincial Programs: Nova Scotia first-time buyers may also be eligible for provincial programs that complement the federal GST rebate, creating a comprehensive support system for new homeowners. This combination of federal and potential provincial benefits makes Nova Scotia an attractive destination for those seeking affordable homeownership.

Looking Ahead: The Impact on Canada’s Housing Market

The FTHB GST Rebate represents a significant policy shift that could reshape Canada’s housing landscape. By providing substantial financial relief to first-time buyers while encouraging new construction, this initiative addresses both demand-side affordability and supply-side challenges.

The program’s five-year, $3.9 billion commitment demonstrates the federal government’s recognition that homeownership remains a cornerstone of financial security for Canadian families. As the program launches in 2025-26, its success will likely influence future housing policy decisions and could serve as a model for other jurisdictions facing similar affordability challenges.

Conclusion: A New Era for First-Time Homebuyers

The First-Time Home Buyers’ GST Rebate marks a pivotal moment in Canadian housing policy, offering unprecedented relief to those taking their first steps into homeownership. With the potential to save up to $50,000 in GST, this program can transform the financial equation for first-time buyers, making homeownership accessible to thousands of Canadians who might otherwise be priced out of the market.

As the program’s implementation approaches, prospective buyers should begin preparing by reviewing eligibility requirements, understanding the timeline restrictions, and connecting with qualified professionals who can guide them through the process. The FTHB GST Rebate represents more than just tax relief—it’s an investment in the future of Canadian homeownership and a recognition that every Canadian deserves the opportunity to build equity and stability through homeownership.

For those considering their first home purchase, the message is clear: the path to homeownership in Canada just became significantly more accessible. With careful planning and proper guidance, the FTHB GST Rebate can help turn the dream of homeownership into reality for a new generation of Canadian families.

The Complete Guide to Property Taxes in Nova Scotia

The Complete Guide to Property Taxes in Nova Scotia: What Every Homeowner and Buyer Needs to Know in 2026

Last updated: April 2026 | Tax rate examples in this guide reflect 2025 data. Municipal rates and CAP percentages are updated annually, always confirm current figures with your municipality and PVSC.

Are you buying your first home in Nova Scotia or trying to understand your property tax bill? You’re not alone. Property taxes are one of the largest ongoing expenses for homeowners, yet many people don’t fully understand how they’re calculated or what programs might help reduce their burden.

This comprehensive guide breaks down everything you need to know about Nova Scotia’s property tax system, including the money-saving Capped Assessment Program that could significantly impact your tax bill.

How Property Taxes Work in Nova Scotia: The Basics

Property taxes in Nova Scotia fund essential municipal services like roads, water systems, fire protection, and community facilities. Unlike income taxes, property taxes are calculated based on your property’s assessed value rather than your ability to pay.

Here’s the simple formula every Nova Scotia property owner should know:

Property Tax = Assessed Value × Municipal Tax Rate

But as you’ll see, there’s more to the story thanks to special programs designed to protect homeowners.

Who’s Responsible for Your Property Tax Bill?

Three key organizations work together to determine and collect your property taxes:

Property Valuation Services Corporation (PVSC)

- Assesses every property in Nova Scotia annually

- Uses market value as of January 1st of the previous year

- Determines your property’s assessed value

Your Municipality

- Sets local tax rates (which vary significantly across the province)

- Calculates your actual tax bill

- Issues bills and collects payments

- May add area rates for specific services

Nova Scotia Government

- Creates property tax legislation

- Oversees programs like the Capped Assessment Program

- Sets provincial education tax rates

Understanding Property Assessment: How Your Home’s Value is Determined

PVSC uses three main methods to assess your property’s value:

Market Approach (Most Common for Residential Properties) Your home’s value is based on recent sale prices of similar properties in your area. This reflects what buyers are actually willing to pay.

Income Approach (For Rental Properties) Used for apartments and commercial buildings based on the income they generate.

Cost Approach (For Unique Properties) When there aren’t enough comparable sales, assessors estimate what it would cost to rebuild your property, minus depreciation.

The Capped Assessment Program: Nova Scotia’s Property Tax Protection

Nova Scotia’s Capped Assessment Program (CAP) is one of the most important features of the provincial property tax system, yet many homeowners don’t fully understand how it works.

What is the CAP?

Introduced in 2005, the CAP protects owner-occupied homeowners from sudden tax increases when property values rise rapidly. Instead of your taxes jumping dramatically with market increases, your assessed value for tax purposes can only increase by the Nova Scotia Consumer Price Index (CPI) each year.

CAP Eligibility Requirements

To qualify for the CAP, you must:

- Own and live in your home as your primary residence

- Have lived in the property for at least one year

- The property must be residential (not commercial)

Important: New construction and non-owner-occupied properties don’t qualify for the CAP.

How the CAP Saves You Money

PVSC publishes the CAP rate annually based on Nova Scotia’s CPI. Recent published rates have been: 3.2% for 2024, 1.5% for 2025, and 2.6% for 2026. This means your assessed value for tax purposes can only rise by that percentage each year, regardless of how much your market value increases.

Example (illustrative only): If your home’s market value jumped from $350,000 to $420,000 in one year, but you’re protected by the CAP, your assessed value for tax purposes might only increase by the applicable CAP rate for that year, potentially a fraction of the actual market movement.

Always check PVSC’s website for the current year’s CAP percentage before estimating your tax bill.

When the CAP Resets

The protection ends when:

- You sell the property

- You complete major renovations

- The property changes from owner-occupied to rental

Buyer Beware: When you purchase a home that was previously capped, your taxes will be calculated based on current market value, potentially resulting in a significant increase from what the previous owner paid. This is one of the most important things to research before making an offer.

2025 Sample Property Tax Rates Across Nova Scotia

Tax rates vary significantly depending on where you live. The table below shows 2025 sample rates for reference only, Halifax and other municipalities have since approved budget changes for 2025–26 and 2026–27. Always check your municipality’s current website for the rate that applies to your tax bill.

| Municipality | Residential Rate (per $100) | Commercial Rate (per $100) |

|---|---|---|

| Halifax (Urban) | $0.661 | $2.738 |

| Lunenburg District | $0.81 | $1.957 |

| Colchester | $0.885 | $2.28 |

Note: Halifax Regional Municipality has approved meaningful tax bill increases in both its 2025 and 2026–27 budgets. These sample figures are no longer current for HRM and are shown for illustrative purposes only.

Remember: Additional area rates may apply for services like fire protection, public transit, community facilities, and provincial education taxes.

Calculating Your Property Tax: A Real Example

Let’s walk through a typical calculation for a Halifax property:

Property Details:

- Assessed value: $400,000

- Location: Urban Halifax

- Municipal rate: $0.661 per $100 (2025 sample rate — confirm current rate with HRM)

Calculation: $400,000 ÷ 100 × $0.661 = $2,644 in municipal taxes

Plus any applicable area rates for additional services.

A Note on Deed Transfer Tax (Non-Resident Buyers)

Property tax is an ongoing annual cost, but buyers should also be aware of a separate one-time cost: the Deed Transfer Tax, paid at closing when you purchase a property.

Nova Scotia increased the Non-Resident Deed Transfer Tax from 5% to 10% effective April 1, 2025, for non-resident buyers of residential property, unless the buyer relocates to Nova Scotia within six months. If you’re a Nova Scotia resident purchasing a home, the standard municipal deed transfer tax applies instead.

This is distinct from your annual property tax bill, but it’s a meaningful upfront cost to account for in your buying budget. Your real estate lawyer will confirm which rate applies to your purchase.

Property Tax Bills and Payment in Nova Scotia

When You’ll Receive Your Bill

Most municipalities issue property tax bills once or twice per year. Due dates and instalment options vary, always check your municipality’s specific billing schedule, as it differs across HRM, Colchester, East Hants, and other areas.

Late Payment Penalties

Don’t miss these deadlines. Late payments typically incur daily interest at 15% per annum, which adds up quickly.

Available Rebates and Exemptions

Some municipalities offer property tax relief for low-income residents, senior citizens, veterans, and properties with accessibility modifications. Check with your local municipality to see what programs are available in your area.

Essential Tips for Property Buyers

If you’re buying property in Nova Scotia, keep these important points in mind.

Before You Buy

- Check if the property is capped This information is crucial for estimating your future tax liability

- Use online tools like mypropertyreport.ca to compare capped and market values

- Request a tax estimate from the municipality before closing

- Factor in potential increases if the cap will reset after your purchase

If you’re a first-time buyer, it’s also worth reviewing Nova Scotia’s 2% Down Payment Program and the full range of federal and provincial programs available to you, your total cost of ownership includes property tax, and knowing these programs can affect how much home you can afford.

After Purchase

- Understand that your taxes may be higher than the previous owner’s if they benefited from the CAP

- Keep records of any major home improvements that might affect your assessment

- Consider appealing your assessment if you believe it’s inaccurate

How to Research Property Values and Taxes

Before buying or if you’re questioning your current assessment, these resources can help:

- mypropertyreport.ca — Compare capped and market values

- Your municipality’s website — Find current tax rates and area charges

- PVSC website — Understand assessment methods and appeal processes

- Nova Scotia market statistics — Track local price trends to understand whether your assessment reflects current market conditions

Understanding Assessment Appeals

If you believe your property has been over-assessed, you have the right to appeal. The process typically involves:

- Reviewing your assessment notice carefully

- Gathering evidence of your property’s actual value

- Filing an appeal within the specified timeframe

- Presenting your case to an assessment review board

The Impact of Market Changes on Property Taxes

Nova Scotia’s real estate market has seen significant changes in recent years, average sale prices have climbed substantially since 2021, with the provincial average now sitting in the mid-$460,000 range as of early 2026. You can see the full picture in our Nova Scotia Real Estate Market Statistics 2025 year-end report.

While the CAP protects existing homeowners, new buyers face the reality of current market values. This creates a two-tiered system where:

- Long-term homeowners with capped assessments pay lower taxes

- New homeowners pay taxes based on current market values

- The tax burden increasingly shifts to newer residents

Planning for Property Tax Increases

Whether you’re a current homeowner or prospective buyer, it’s wise to plan for potential tax increases.

For Current Homeowners

- Budget for annual CAP rate increases each year (PVSC publishes the rate in January)

- Be prepared for reassessment after major renovations

- Consider the tax implications before selling and buying elsewhere

For Buyers

- Factor property taxes into your overall housing budget

- Don’t rely on the seller’s current tax bill for your planning

- Get official tax estimates from the municipality

- If you’re thinking about selling to buy elsewhere, review our seller’s guide to understand the full financial picture

Frequently Asked Questions

Q: Can I get the CAP on a second home or cottage? A: No, the CAP only applies to your primary residence where you live year-round.

Q: What happens to my CAP if I rent out part of my home? A: As long as you live in the home as your primary residence, partial rental doesn’t affect your CAP eligibility.

Q: How do I know if a property I’m buying is currently capped? A: Check the property report at mypropertyreport.ca or ask your real estate agent to verify the capped vs. market value.

Q: Can property taxes be included in my mortgage payment? A: Yes, many lenders offer escrow services where they collect property taxes monthly and pay them on your behalf. Speak with your lender or mortgage broker about this option when getting pre-approved.

Conclusion: Making Informed Property Decisions in Nova Scotia

Understanding Nova Scotia’s property tax system is essential for making smart real estate decisions. The Capped Assessment Program provides valuable protection for long-term homeowners, but buyers need to understand the full tax implications of their purchase — including what the CAP reset means for their budget on day one.

Key takeaways:

- Property taxes are calculated using assessed value and municipal tax rates

- The CAP can significantly reduce tax burden for eligible homeowners, but the rate changes annually based on CPI; check PVSC’s site each January for the current figure

- Tax rates vary substantially across different municipalities, and several have increased meaningfully in 2025–26

- Non-resident buyers face an increased deed transfer tax of 10% since April 2025

- New buyers should expect to pay taxes based on current market values

- Professional advice and thorough research are essential before major property decisions

Whether you’re buying your first home or your fifth, taking time to understand the property tax implications will help you make better financial decisions and avoid unwelcome surprises. If you’d like to talk through how property taxes factor into a specific purchase, our team is happy to help.

For the most current tax rates, CAP percentages, and regulations, always consult your local municipality and PVSC directly, and consider speaking with a qualified real estate professional or tax advisor.

By Rob Lough, Broker/Owner | Century 21 Optimum Realty | Halifax-Dartmouth, Nova Scotia

Rising Mortgage Rates and the Bank of Canada’s Next Move

Rising Mortgage Rates and the Bank of Canada’s Next Move: What Canadian Homeowners Need to Know

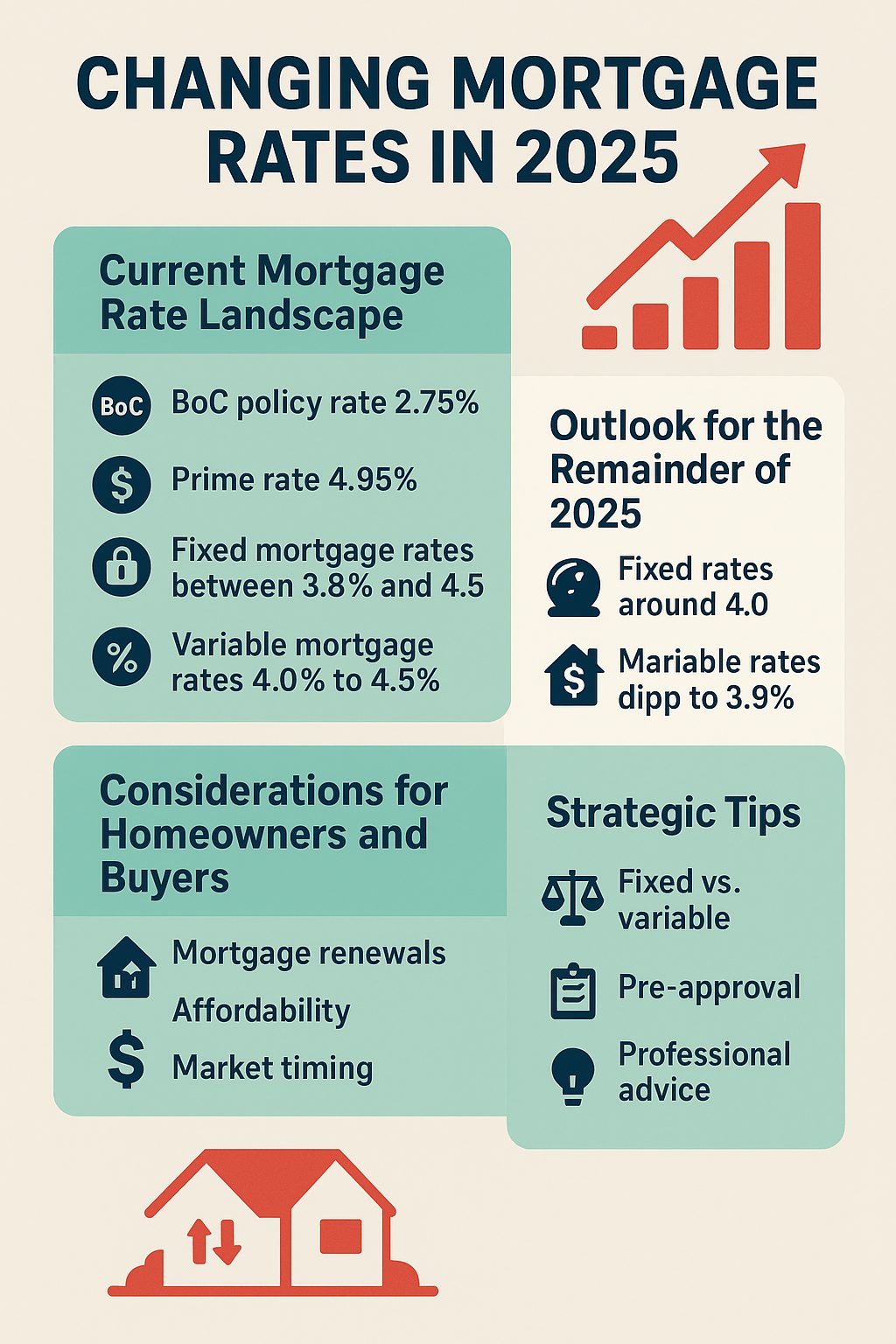

Canadian mortgage rates are rising while the Bank of Canada prepares its next rate decision. Learn what homeowners and buyers need to know about changing mortgage rates in 2025. Homebuyers and homeowners across Canada are navigating a shifting mortgage landscape as fixed mortgage rates climb and the Bank of Canada prepares for its next critical rate decision. With bond yields rising and lenders adjusting their strategies, understanding these changes is essential for making informed financial decisions.

Why Canadian Fixed Mortgage Rates Are Rising

Lenders Respond to Market Pressures

Canadian lenders have begun raising fixed mortgage rates after months of competitive pricing. This significant shift stems from several key factors:

- Higher bond yields directly impact fixed-rate mortgage costs

- Global inflation concerns affecting international lending markets

- Central bank caution worldwide signaling tighter monetary policy

- Reduced lender competition as aggressive pricing strategies wind down

The end of ultra-low fixed mortgage rates means Canadian borrowers face a new reality. Those seeking new mortgages or approaching renewal dates may encounter rates significantly higher than recent years, directly impacting monthly payment calculations.

Impact on Borrowing Costs

For mortgage shoppers, the most competitive rates that defined 2024 are becoming harder to find. This rate environment particularly affects:

- First-time homebuyers stretching affordability limits

- Homeowners with upcoming mortgage renewals

- Investors considering real estate purchases

- Those planning to refinance existing mortgages

Bank of Canada Rate Decision: What to Expect

Steady Policy Rate Likely

Despite rising fixed rates in the broader market, the Bank of Canada is expected to maintain its key overnight rate at the upcoming policy meeting. Several economic indicators support this measured approach:

Positive Economic Signals:

- Stronger-than-expected Canadian economic growth

- Resilient consumer spending patterns

- Stable employment levels

- Controlled inflation trends

Variable Rate Mortgage Stability

If the Bank of Canada holds rates steady, variable-rate mortgage holders can expect:

- No immediate payment changes on existing mortgages

- Continued affordability compared to fixed-rate options

- Stability amid market volatility

- Time to assess long-term mortgage strategies

Strategic Implications for Canadian Homeowners

Fixed-Rate Mortgage Holders

Homeowners with fixed-rate mortgages approaching renewal should prepare for potentially higher costs. Key considerations include:

- Review renewal timeline and current rate environment

- Explore early renewal options if beneficial

- Compare lenders for competitive offerings

- Consider switching to variable rates if appropriate

New Home Buyers

Prospective buyers face increased monthly payment obligations compared to earlier periods. Important factors include:

- Budget adjustment for higher mortgage costs

- Down payment strategies to reduce borrowing needs

- Pre-approval timing to secure current rates

- Market timing considerations

Variable-Rate Mortgage Holders

Current variable-rate borrowers enjoy short-term stability but should monitor:

- Future Bank of Canada decisions and economic indicators

- Payment shock preparation for potential rate increases

- Conversion options to fixed rates if needed

- Stress testing financial capacity for rate changes

Housing Market Outlook and Predictions

Market Cooling Expected

Higher mortgage rates typically influence housing market dynamics through:

- Reduced buyer affordability limiting demand

- Price stabilization in overheated markets

- Inventory increases as fewer buyers compete

- Regional variations based on local economic conditions

Economic Fundamentals Provide Support

Despite rate pressures, several factors may support housing market stability:

- Strong employment levels maintaining buyer confidence

- Population growth driving housing demand

- Limited housing supply in key markets

- Economic diversification supporting regional markets

Expert Recommendations for Canadian Homeowners

Immediate Action Steps

- Review current mortgage terms and renewal dates

- Monitor rate trends and Bank of Canada communications

- Assess financial capacity for higher payments

- Explore mortgage options with qualified professionals

Long-Term Planning Strategies

- Build payment flexibility into household budgets

- Consider mortgage acceleration during stable periods

- Maintain emergency funds for economic uncertainty

- Stay informed about policy changes and market trends

Professional Mortgage Guidance

Given the complexity of current mortgage markets, consulting with qualified mortgage professionals becomes increasingly valuable. Experienced advisors can help with:

- Rate comparison across multiple lenders

- Strategy development for individual circumstances

- Risk assessment for different mortgage products

- Timing optimization for renewals and purchases

Conclusion: Navigating Canada’s Changing Mortgage Landscape

Canadian mortgage markets are experiencing significant transitions as fixed rates rise and monetary policy remains cautious. While the Bank of Canada’s measured approach provides some stability for variable-rate borrowers, the overall trend suggests higher borrowing costs ahead.

Homeowners and prospective buyers must stay informed, plan strategically, and seek professional guidance to navigate these changes successfully. By understanding market dynamics and preparing for various scenarios, Canadians can make confident mortgage decisions despite economic uncertainty.

Stay updated on Bank of Canada announcements and mortgage rate trends to make the most informed decisions for your financial future.

For personalized mortgage advice and current rate information, consult with a licensed mortgage professional in your area.

Halifax & Bedford Housing Boom

🏡 Halifax & Bedford Housing Boom: Dreams Coming True! 🚀

Exciting times ahead! Halifax and Bedford are about to experience a game-changing housing revolution! 🎉 The Nova Scotia government has just given the green light for up to 19,500 new homes in two amazing growth hotspots: the beautiful Sandy Lake area in Bedford and the bustling Highway 102 west corridor in Halifax! 💫

This incredible move follows thorough community studies that looked at everything from protecting our precious environment 🌲 to making sure we have all the infrastructure we need. Now, Halifax Regional Municipality (HRM) can dive into detailed planning that will shape these wonderful new neighborhoods where families will create memories for generations! 👨👩👧👦

Why should you be excited? 🤔 With Halifax’s population booming like never before and housing needs skyrocketing 📈, these developments are designed to bring homes to market faster—cutting through red tape and saving up to two whole years in approval time! Imagine that! These aren’t just any homes either—they’ll be part of thoughtfully designed, sustainable communities where infrastructure and environmental protection take center stage. 🌱

Minister Colton LeBlanc, who shared this fantastic news, highlighted just how important smart planning is:

“With thoughtful, well-informed planning, we can create vibrant, sustainable communities that will provide the homes Nova Scotians need and help protect the environment for all to enjoy.” 💚

What’s coming next for locals and developers? 🔍 HRM will soon kick off an exciting secondary planning process for both areas, including technical reviews and opportunities for YOU to get involved! Look forward to comprehensive master plans for roads, water systems, and wastewater management, plus amazing strategies to protect our beloved parklands and natural spaces. 🌳

This announcement is just one piece of a bigger provincial vision, with 16 special planning areas now designated across HRM and more than 60,000 housing units in the works! 😮 The province is backing these incredible initiatives with funding and regulatory changes to ensure projects move forward quickly but responsibly. 💪

Stay connected! As planning moves forward, you’ll have plenty of chances to share your thoughts and help shape the future of these wonderful communities. For those dreaming of buying or renting, the future of diverse housing options in Halifax and Bedford has never looked brighter! ✨

Want to know more? Visit the Halifax Regional Municipality’s special planning areas page and check out Nova Scotia’s housing action plan for all the exciting details! 📱

Halifax Water Rate Increases Are Drowning Household Budgets

The Rising Tide: How Halifax Water Rate Increases Are Drowning Household Budgets 💧

Another Wave of Costs Hits Halifax Residents 🌊

Just when Halifax residents thought their budgets couldn’t be stretched any thinner, Halifax Water has announced significant rate increases that will impact households across the municipality. In a time when many are already struggling with the rising cost of living, this news comes as yet another financial burden for homeowners, landlords, and tenants alike.

The Numbers: Brace for Impact 📊

Halifax Water has applied for a substantial 16.2% increase in residential bills for the 2025-26 fiscal year, followed by an additional 17.6% increase in 2026-27. This translates to an estimated increase of $148.01 in 2025-26 and $186.56 in 2026-27 for the average household. These aren’t small adjustments – they represent significant jumps that will be felt by everyone who receives a water bill in Halifax.

Why the Increase? 🤔

According to Halifax Water, the utility is facing “significant operating deficits” – projected to be $18.7 million for 2024-25 and a whopping $34.1 million for 2025-26. The utility cites several factors contributing to these deficits:

- 🔄 Inflation impacting operational costs

- 💰 Depleted reserve funds

- 🏗️ Aging infrastructure requiring expensive maintenance and upgrades

- 🌱 Population growth in the HRM requiring system expansion

The Ripple Effect on Halifax Residents 🏠

For Homeowners 🏡

Homeowners in Halifax are already contending with:

- Rising property taxes

- Increased insurance premiums

- Higher mortgage interest rates

- Growing maintenance costs

Adding significant water rate increases to this mix puts even more pressure on household budgets that are already stretched to their limits. For many, these combined increases mean difficult choices about where to cut back spending.

For Landlords 🔑

Landlords face a challenging position:

- Absorb the increased costs themselves, reducing already thin profit margins

- Pass costs along to tenants, potentially making units less affordable

- Find other places to cut corners on property maintenance or improvements

With rental rates already high and many landlords working with tight margins, these increases may ultimately lead to higher rents across the board as property owners try to maintain profitability.

For Tenants 🏢

Perhaps hardest hit will be tenants, who:

- May face rent increases as landlords pass along higher water costs

- Are already dealing with Nova Scotia’s housing affordability crisis

- Often have less financial flexibility to absorb additional costs

For those already spending a large percentage of their income on housing, these increases could push some tenants into housing insecurity.

The Historical Context 📜

This isn’t the first time Halifax Water has increased rates, but the scale of the current proposal is concerning. Previous increases were more modest:

- 3.6% in December 2022

- Another 3.6% in April 2023

These past increases didn’t fully cover costs according to Halifax Water, leading to the current situation where much larger jumps are deemed necessary.

Finding Solutions in a Sea of Costs 💡

Water Conservation Tips ✅

With water becoming more expensive, conservation becomes even more important:

- Fix leaky faucets and toilets promptly

- Install low-flow fixtures where possible

- Consider rainwater collection for gardens

- Run dishwashers and washing machines only when full

- Take shorter showers

Support Programs 🤝

Halifax Water does offer some assistance:

- The H2O (Help to Others) Fund for residential customers struggling with bill payments

- Customer Connect tools to help monitor consumption and detect leaks

Community Action 👥

As rates continue to climb, community advocacy becomes increasingly important:

- Attend public hearings about rate increases

- Contact local representatives about affordability concerns

- Join or form community groups focused on utility affordability

- Support neighbors who may be struggling with bills

The Bigger Picture 🌎

Water rate increases in Halifax are part of a broader trend happening across Canada as municipalities deal with aging infrastructure and climate change impacts. However, that doesn’t make the financial strain any easier for residents to bear.

As essential as clean water is, these significant rate increases highlight the growing tension between necessary infrastructure investment and affordability for everyday citizens. For many Halifax residents, this is just one more wave in a rising tide of costs that threatens to overwhelm household budgets.

The question remains: how many more financial pressures can Halifax residents absorb before something has to give? 💭

Have you been affected by the rising water rates in Halifax? Share your experience in the comments below or reach out to your local councilor to make your voice heard!

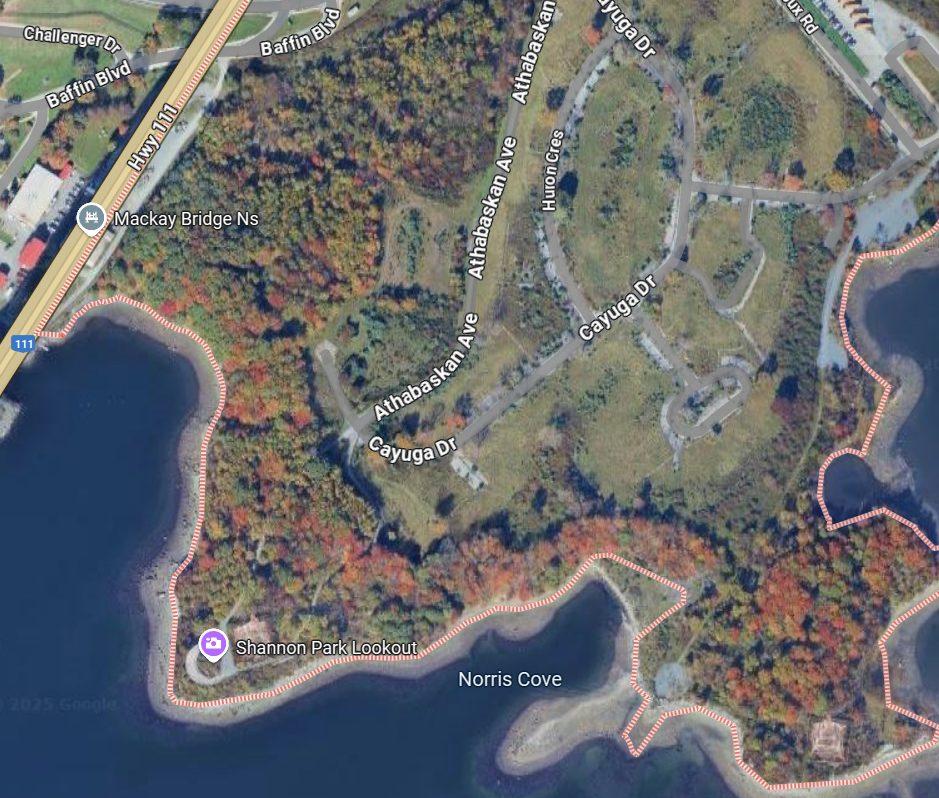

Shannon Park: Nova Scotia’s Bold Step Toward Affordable Housing

Shannon Park: Nova Scotia’s Bold Step Toward Affordable Housing 🏘️

Big news for Dartmouth residents! The Nova Scotia government has made a power move in addressing the province’s housing crisis by purchasing land at Shannon Park for a cool $16.8 million. 🏠 This price tag sits significantly below market value, making it quite the deal.

What’s Happening at Shannon Park? 🔍

The province has acquired over 9,000 square meters of prime real estate—picture two football fields side by side—within a larger 34-hectare property that has sat mostly vacant since 2017. Military housing once stood tall here before being demolished, leaving behind potential waiting to be unlocked. The land acquisition represents hope for thousands of Nova Scotians currently struggling to find affordable places to call home.

Let’s break it down. 💰

The Numbers Tell a Story 📊

The provincial government envisions approximately 600 affordable housing units rising from this land. Think about it: 600 families or individuals who might otherwise struggle to afford housing will have new options. These units will be part of a much grander vision approved by the Halifax Regional Municipality in 2023 that includes:

- 3,000 total housing units across the development

- Commercial spaces for local businesses

- A transit hub connecting residents to the broader city

- Public parks for community gathering and recreation

At least 20% of all housing will be designated as affordable. That’s a commitment worth celebrating! 🎉

Why This Matters Now ⏰

Nova Scotia isn’t just facing a housing challenge—it’s navigating a full-blown crisis. Over 7,000 people currently sit on public housing waitlists across the province. Families wait. Individuals struggle. The need grows daily.

This purchase couldn’t come at a more critical time.

The Path Forward Remains Somewhat Foggy 🌫️

While the land acquisition represents a significant step forward, questions linger about exactly how the government plans to develop or manage these housing units. Will they partner with non-profit organizations? How will they ensure affordability “in perpetuity” as housing advocates hope? The answers remain unclear.

Non-profit housing organizations are eager to participate. They bring expertise and commitment to the table that could prove invaluable in maximizing the impact of this investment.

Part of a Bigger Plan 🗺️

The Shannon Park project isn’t happening in isolation. It’s one piece of a much larger provincial strategy that includes:

- Doubling new public housing units across Nova Scotia

- Investing $136.4 million in affordable housing development

- Focusing resources on high-demand areas like Halifax

- Supporting private developers and community organizations through programs like the Affordable Housing Development Program (AHDP)

What’s Next for Shannon Park? 🚧

Construction timelines haven’t been announced yet. The land is secured. The vision is approved. Now comes the hard work of turning plans into places where people can live and thrive.

With redevelopment approvals already in place and provincial ownership secured, Shannon Park could become a shining example of how government intervention can meaningfully address housing needs while creating vibrant, mixed-use communities. The potential impact cannot be overstated.

The Bottom Line 💡

Nova Scotia’s purchase of Shannon Park land represents more than just a real estate transaction—it symbolizes a commitment to addressing one of the province’s most pressing challenges. Affordable housing isn’t just about putting roofs over heads; it’s about creating stable foundations upon which individuals and families can build their lives.

The coming months and years will reveal whether this bold step delivers on its promise. For now, there’s reason for cautious optimism. Stay tuned! 🏡

Halifax Real Estate: A Smart Alternative in Uncertain Markets

Halifax Real Estate: A Smart Alternative in Uncertain Markets 🏠

Stock markets are shaking. 📉 Investors worldwide are feeling the tremors of recent tariff-related selloffs and growing economic uncertainties that have rattled global equities to their core. This turbulence has many seasoned investors looking beyond traditional market investments toward more tangible alternatives that offer both stability and growth potential during volatile times.

Enter Halifax real estate. 🌊

Nova Scotia’s capital city represents an increasingly attractive investment opportunity for those seeking refuge from stock market uncertainty. Halifax’s property market has demonstrated remarkable resilience and steady growth, creating a compelling case for investors looking to diversify their portfolios with physical assets.

Why Halifax? Why Now? 🤔

Market Stability During Global Uncertainty

The contrast couldn’t be clearer. While stock markets experience daily swings and sudden drops triggered by geopolitical tensions, Halifax’s real estate market maintains its steady upward trajectory. Property values in the city show consistent appreciation patterns that defy the erratic movements seen in equity markets today.

Homes sell quickly here. 🏃♂️ Supply struggles to meet demand.

Promising Property Value Growth 📈

Numbers don’t lie. The average Halifax home resale price is projected to climb from $580,000 in 2024 to $605,000 in 2025, representing solid appreciation for property owners. This growth isn’t happening in a vacuum—it’s driven by fundamental factors including population increases and economic development that strengthen the market’s foundation.

Strong Rental Fundamentals

Immigration fuels Halifax’s rental market. More than 10,000 new residents arrived between mid-2023 and mid-2024 alone! This population surge maintains rental vacancy rates at a tight 2.5%, creating ideal conditions for rental property investors seeking reliable income streams.

Average rents continue climbing. 💰 Two-bedroom units now command approximately $1,740 monthly.

Investment Opportunities That Stand Out 🌟

The “Missing Middle” Housing Advantage

Halifax is getting smart about housing. Recent zoning reforms now permit multi-unit properties like duplexes and fourplexes in previously single-family neighborhoods. This creates exceptional opportunities for small-scale investors who can convert older single-family homes into multiple rental units, maximizing both property value and rental income potential.

The North End and West End neighborhoods show particularly strong demand for these property types.

Luxury Market Momentum

High-end properties are moving fast. 🏆 Sales of homes priced over $1.2 million have surged nearly 43% year-over-year, indicating robust demand from affluent buyers and newcomers with substantial financial resources. This luxury market strength elevates the entire Halifax real estate ecosystem.

Challenges to Consider Before Diving In ⚠️

No investment comes without considerations. Current mortgage rates hovering between 5-6% create tighter margins for leveraged investors compared to previous years. Construction costs have also risen significantly, impacting renovation budgets and new build expenses.

Regulatory factors matter too. 📋

Halifax’s 5% annual rent increase cap limits how quickly landlords can raise rents on existing tenants. Additionally, non-resident investors face a doubled deed transfer tax of 10%, substantially increasing acquisition costs for out-of-province buyers.

Smart Investment Strategies for Today’s Halifax Market 🧠

Focus on affordable and mid-priced rental properties where demand remains strongest. Explore high-potential neighborhoods like the Peninsula and Bedford, where infrastructure improvements such as rapid transit projects could significantly boost property values in coming years.

Consider small multi-unit developments. 🏘️ Halifax’s pro-density policies create opportunities for investors willing to pursue property conversions or small-scale developments that address the city’s housing shortage.

The Bottom Line 💼

When stock markets tremble, real assets often provide stability. Halifax’s real estate market offers a compelling alternative for investors seeking to diversify away from volatile equities while maintaining growth potential. The combination of population growth, housing demand, and limited supply creates favorable conditions for long-term real estate investment success.

Timing matters in real estate. 🕰️ With Halifax’s current market fundamentals and the contrast against stock market instability, now presents a strategic moment to consider adding Halifax properties to your investment portfolio.

Just remember to factor in financing costs, regulatory considerations, and your personal investment goals before taking the plunge into this promising maritime market!

What’s your experience with real estate investing? 🤔 Have you considered diversifying into property markets like Halifax? If so, please click here to look for properties to invest in!

Halifax Burger Bash April 3-12 2025

Halifax Burger Bash April 3-12 2025: A Decade-Plus of Burger Bliss and Giving Back

Halifax has been renamed Burger Town once again! Halifax Burger Bash is back, and it’s bigger and better than ever. This city-wide burger-eating phenomenon, presented by The Coast, isn’t just about devouring creative and delicious burgers; it’s also a major fundraiser for Feed Nova Scotia.

What is Burger Bash?

For the uninitiated, Halifax Burger Bash is a culinary celebration where restaurants across the city craft unique burger offerings. Some have a special set price, while others donate a portion of the proceeds from each burger sold to Feed Nova Scotia. It’s a win-win: you get to explore new restaurants and revisit old favorites, all while supporting a vital cause.

Burgers for a Cause

Over the past 12 years, Halifax Burger Bash has raised an incredible $993,821 for Feed Nova Scotia! Every $2 raised translates to three meals worth of donated food distributed to those in need. In a province where 1 in 3 households face food insecurity, the impact of Burger Bash is truly significant.

Get Your Passport and Win!

Want to add some extra excitement to your Burger Bash adventure? Pick up a printed passport at any of the participating restaurants. Collect stamps or initials from at least three locations, and you could win $1000 in Garrison Gift Cards!

Thank You to the Partners

The success of Burger Bash wouldn’t be possible without the generous support of our partners. Their contributions are the special sauce that makes this city-wide patty party so special.

So, get ready to embark on a burger journey, Halifax! With every bite, you’ll be savoring not only delicious flavors but also the satisfaction of knowing you’re making a difference in your community. For a list of participating Restaurants, please click here

Mortgage Rates Hit 3-Year Low: What This Means for Halifax Homebuyers

Mortgage Rates Hit 3-Year Low: What This Means for Halifax Homebuyers 🏠💰

In a housing market that’s been on a rollercoaster ride since the pandemic, there’s finally some good news for homebuyers. Mortgage rates have dropped to their lowest point since 2021! 📉 But what does this mean for Halifax’s real estate landscape? Let’s dive in.

Current Mortgage Rates: A Welcome Breath of Fresh Air 😮💨

The numbers don’t lie. Five-year fixed mortgage rates have fallen to 3.89%, marking the first time rates have dipped below 4% since 2021. This dramatic shift didn’t happen overnight. The Bank of Canada’s recent 0.25% rate cut in March 2025, coupled with softening inflation expectations, has created the perfect storm for lower borrowing costs.

Remember those pandemic-era rates? While we’re not quite back to the days of 0.88% variable rates that had homebuyers scrambling in 2020-2021, the current downward trend signals a significant improvement from the peak rates we’ve endured over the past few years.

Halifax’s Housing Market: Ready for Takeoff? 🚀

1. Buyers Are Back in Action

Lower mortgage rates mean improved affordability. A family that could afford a $450,000 home last year might now qualify for something closer to $500,000. This shift is particularly significant in Halifax, where housing remains relatively affordable compared to Toronto or Vancouver’s astronomical prices.

First-time buyers who’ve been saving diligently during the higher-rate environment are now eyeing their opportunity. Investors, too, are taking a fresh look at Halifax’s potential. The math simply works better when borrowing costs drop.

2. Price Stabilization After the Cooling Period ❄️➡️☀️

Halifax’s median home price of approximately $535,000 in early 2025 tells a story of moderation after years of pandemic-fueled growth. The cooling trend of 2023-2024 appears to be reversing course. With renewed buyer interest and still-limited inventory, we’re likely to see prices stabilize and potentially increase moderately through 2025.

Long-time Halifax residents who weathered the market’s ups and downs may find this an opportune moment to either upgrade or cash out, depending on their circumstances.

3. What About Renters? 🏢

The rental market presents an interesting dilemma. Logic suggests that as more renters become homeowners, rental demand should decrease. However, Halifax’s extraordinarily tight vacancy rate of just 1.8% in 2024 creates a floor effect. There simply isn’t enough rental supply to allow for significant rent decreases, even if some renters do make the jump to homeownership.

For landlords, the reduced borrowing costs on investment properties could potentially improve cash flow without necessitating further rent increases.

Crystal Ball: Will Rates Drop Further? 🔮

The Case for More Cuts

Economic indicators are sending mixed signals, but several factors point toward additional rate cuts:

- GDP growth limped along at just 0.2% in Q4 2024

- Unemployment has been creeping upward

- Core CPI inflation fell to 2.8% year-over-year in February 2025, inching closer to the Bank of Canada’s 2% target

These signs of economic weakness may prompt the BoC to continue its easing cycle to stimulate growth.

The Case for Caution ⚠️

It’s not all smooth sailing ahead. March 2025 brought an inflation surprise, with CPI jumping to 3.1%, driven primarily by energy costs and holiday-season spending patterns. This uptick might give the BoC pause.

Adding complexity to the analysis is the Trudeau government’s temporary holiday sales tax suspension in late 2024. This GST cut may have artificially inflated consumer spending data, making it harder for the BoC to get a clear read on underlying inflation trends.

What Does This Mean for Halifax Homebuyers? 🤔

If you’ve been waiting for the “right time” to enter Halifax’s housing market, the current environment offers compelling reasons to take action. The spring market is heating up with increased sales volumes, but inventory remains limited. This combination typically leads to competitive bidding scenarios, especially for well-located, move-in-ready properties.

The Bank of Canada will likely pause its rate-cutting cycle if inflation persists above 3%. However, once the temporary effects of the tax cuts fade from the data, further reductions become more probable. Waiting for even lower rates could mean facing higher home prices and more competition.

For existing homeowners, this might be an excellent time to consider refinancing options, especially if you locked in at significantly higher rates in recent years.

The bottom line? Halifax’s housing market is regaining momentum. Those 3.89% mortgage rates won’t last forever, and neither will today’s home prices if buyer demand continues to strengthen. 🏡💪

What’s your next move in this changing real estate landscape? Check out homes for sale in HRM. Click here