Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

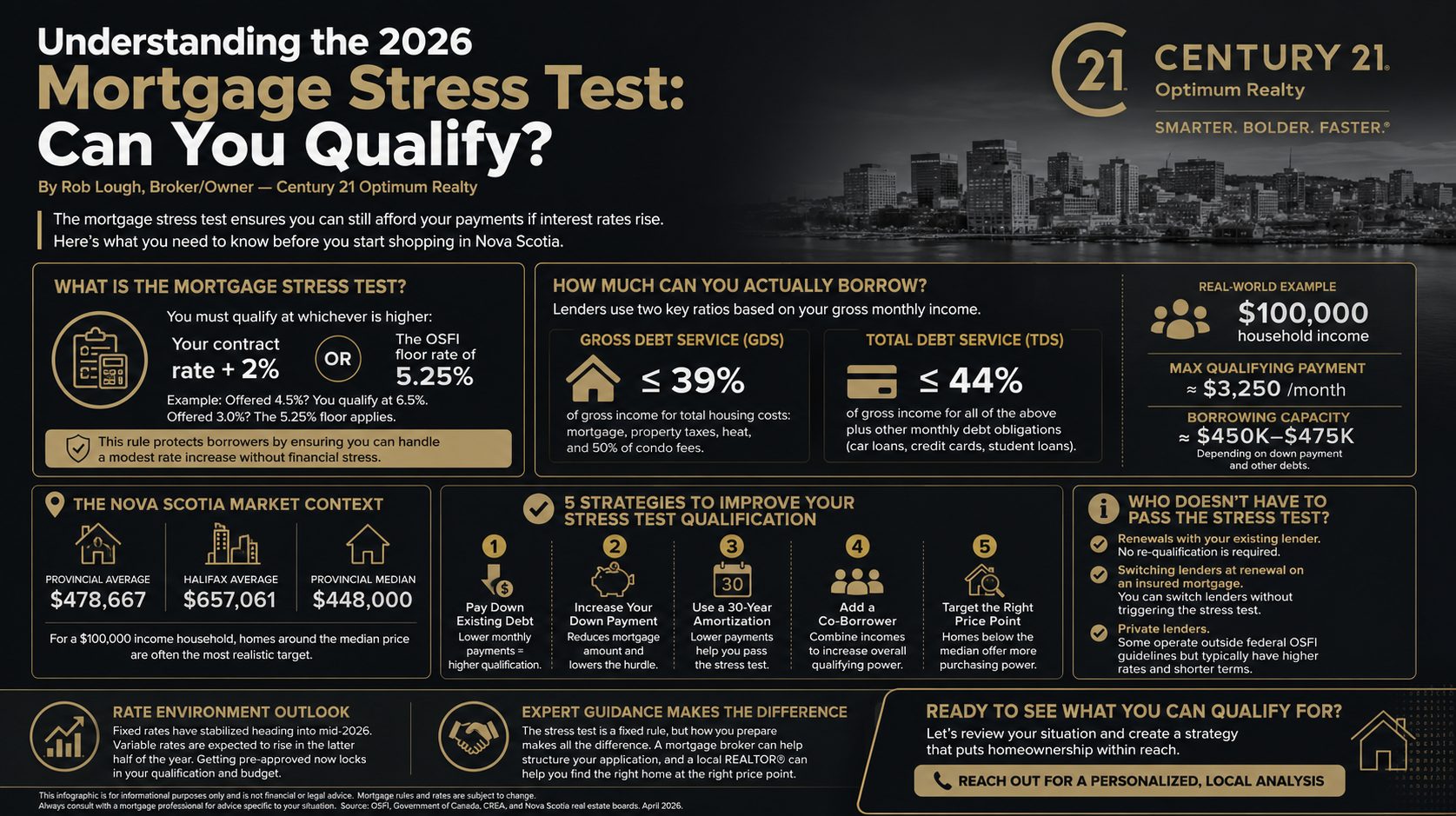

Understanding the 2026 Mortgage Stress Test Can You Qualify

Understanding the 2026 Mortgage Stress Test: Can You Qualify?

By Rob Lough, Broker/Owner — Century 21 Optimum Realty

If you’re planning to buy a home in Nova Scotia this year, the mortgage stress test is one of the first hurdles you’ll need to clear. It’s not a credit check or a property appraisal, it’s a math test designed to make sure you can still afford your mortgage payments if interest rates rise after you sign.

Here’s what you need to know before you start shopping.

What Is the Mortgage Stress Test?

The stress test requires that you qualify for your mortgage at a higher rate than the one you’ll actually pay. Specifically, federally regulated lenders, banks, credit unions, and most mortgage companies, must qualify you at whichever is higher: your contract rate plus 2%, or the OSFI floor rate of 5.25%.

So if you’re offered a 4.5% fixed rate, you’ll need to qualify as if your rate is 6.5%. If rates were to drop and you secured a 3.0% rate, the 5.25% floor would apply instead.

This rule exists to protect borrowers, not to penalize them. The goal is to make sure you’re not stretched so thin that a modest rate increase forces a financial crisis. For a full look at what changed heading into 2026, see our article on OSFI’s 2026 Mortgage Changes.

How Much Can You Actually Borrow?

Two ratios govern how much a lender will approve you for:

Gross Debt Service (GDS): Your total housing costs, mortgage payment, property taxes, heat, and 50% of condo fees, cannot exceed 39% of your gross monthly income.

Total Debt Service (TDS): All of the above, plus your other monthly debt obligations (car loans, credit cards, student loans), cannot exceed 44% of your gross income.

Here’s a real-world example: On a household income of $100,000 per year, your maximum qualifying payment at the stress test rate works out to roughly $3,250/month. That typically translates to a borrowing capacity of approximately $450,000–$475,000, depending on your down payment and other debts.

Use our Mortgage Calculator to plug in your own numbers and see where you stand.

What This Means in the Nova Scotia Market

The stress test hits hardest in higher-priced markets and Halifax is exactly that.

The provincial average home price sits at $478,667. The Halifax average is $657,061. The median sale price across Nova Scotia is around $448,000 and that’s often where a household with a $100,000 income is realistically shopping.

For buyers with typical incomes, Halifax’s price point may require a larger down payment, a co-borrower, or a shift in search area. For full current pricing data across the province, see our Nova Scotia Real Estate Market Stats April 2026.

5 Strategies to Improve Your Stress Test Qualification

1. Pay Down Existing Debt

Your TDS ratio includes every monthly debt obligation. Eliminating $200/month in debt payments can increase your mortgage qualification by $30,000–$40,000. If you’re carrying a car payment or credit card balance you can realistically eliminate before applying, do it first.

2. Increase Your Down Payment

A larger down payment reduces the mortgage amount, which directly lowers the stress test hurdle. Nova Scotia buyers have access to two provincial programs worth knowing: the Nova Scotia 2% Down Payment Program and the Nova Scotia Down Payment Assistance Program, which offers a 5% interest-free loan for eligible buyers.

3. Use a 30-Year Amortization

First-time buyers now qualify for 30-year amortizations on insured mortgages. Spreading payments over 30 years lowers your monthly payment, which makes it easier to pass the stress test even at the qualifying rate. This stacks well with other programs, see How Nova Scotia First-Time Buyers Can Stack Federal and Provincial Programs for a full breakdown.

4. Add a Co-Borrower

Combining incomes is one of the most effective ways to increase qualifying power. Both applicants must pass the stress test individually, but the combined income and debt picture is what the lender uses to set the limit.

5. Target the Right Price Point

Sometimes the most practical move is adjusting where you’re shopping. Properties priced below the median ($448K) see more balanced competition, and areas outside HRM, offer significantly more purchasing power at equivalent income levels.

Who Doesn’t Have to Pass the Stress Test?

There are a few scenarios where the stress test doesn’t apply:

- Renewals with your existing lender. If you’re renewing and staying with the same lender, no re-qualification is required.

- Switching lenders at renewal on an insured mortgage. You can now switch lenders at renewal without triggering the stress test on insured mortgages, a meaningful change for many homeowners.

- Private lenders. Some private lenders and provincially regulated credit unions operate outside federal OSFI guidelines, though these typically come with higher rates and shorter terms.

For more on how renewal rules have changed, see our breakdown of New Mortgage Rules in Canada.

A Word on the Current Rate Environment

Fixed rates have stabilized heading into mid-2026, and variable rates are expected to see some upward movement in the latter half of the year. Getting pre-approved now locks in your qualification and gives you a defined budget before rate conditions shift.

For context on where rates have been and where they may be heading, our article Mortgage Rates Hit 3-Year Low: What This Means for Halifax Homebuyers provides useful historical perspective.

Working With the Right Team Matters

The stress test is a fixed rule, but how you position yourself before applying makes a significant difference. An experienced mortgage broker can help you time your application, structure your down payment, and identify which lender profile fits your situation.

On the real estate side, working with an agent who understands the local market means identifying properties that fit your real budget, not just your pre-approval ceiling. Browse our Buying & Selling Tips for more practical guidance, or reach out directly to talk through where you stand.

Related Resources

Spring 2026 Nova Scotia Real Estate

Spring 2026 Nova Scotia Real Estate: Balanced Market, Normal Seasonality, and More Room to Negotiate

By Rob Lough, Broker/Owner | Century 21 Optimum Realty | April 2026

March’s numbers are in, and they confirm what the winter data was already pointing toward: Nova Scotia’s real estate market is entering spring 2026 in a more measured, negotiable environment than we saw a year ago. The frenzy of mid-2025 has given way to a more deliberate pace, with longer days on market, softer sold-to-ask ratios, and fewer transactions across the board.

But before anyone mistakes “slower” for “broken,” the headline worth holding onto is this: prices have held. That +1.0% year-over-year return we tracked through the winter tells an important story, this is not a market in freefall. It’s a market finding its footing after a busy year, and spring is already showing signs of the seasonal uptick we’d expect.

If you missed the winter months’ context, our Nova Scotia Real Estate Market Stats for February 2026 walks through the data in detail, and our Nova Scotia Real Estate Market Stats March 2026 report covers the earliest signs of spring stabilization. For the full year-end story of how we got here, our Nova Scotia Real Estate Market Statistics 2025 article provides the complete picture.

Prices: Firm, Not Falling

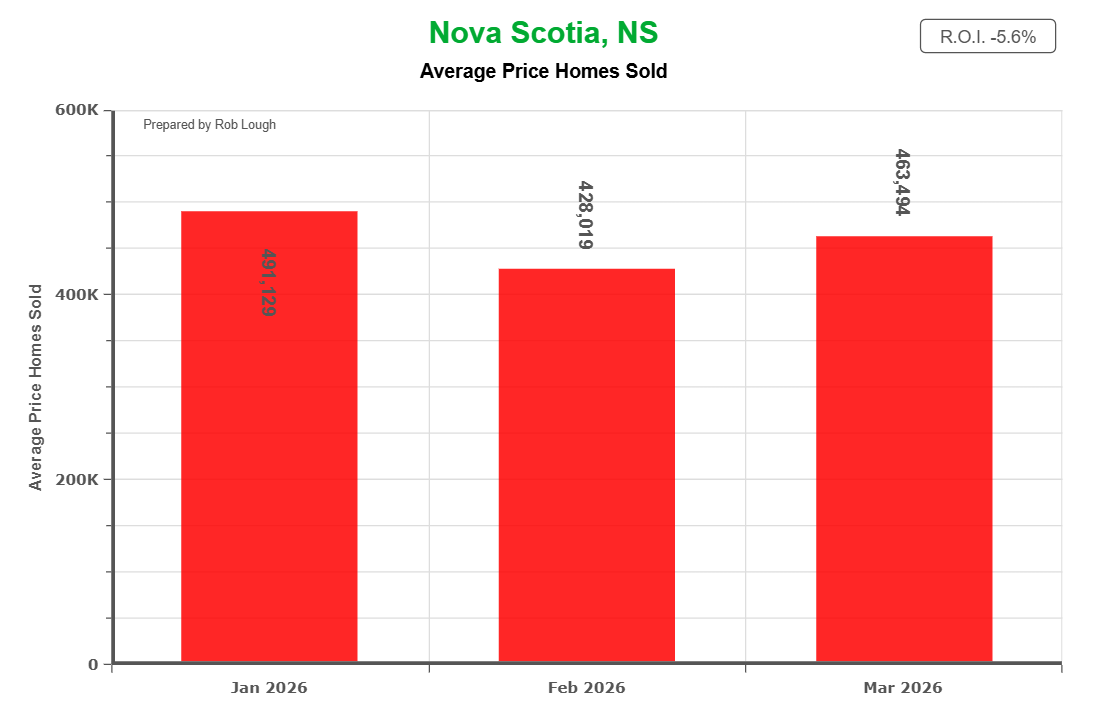

Average Price of Homes Sold Spring 2026 Nova Scotia Real Estate

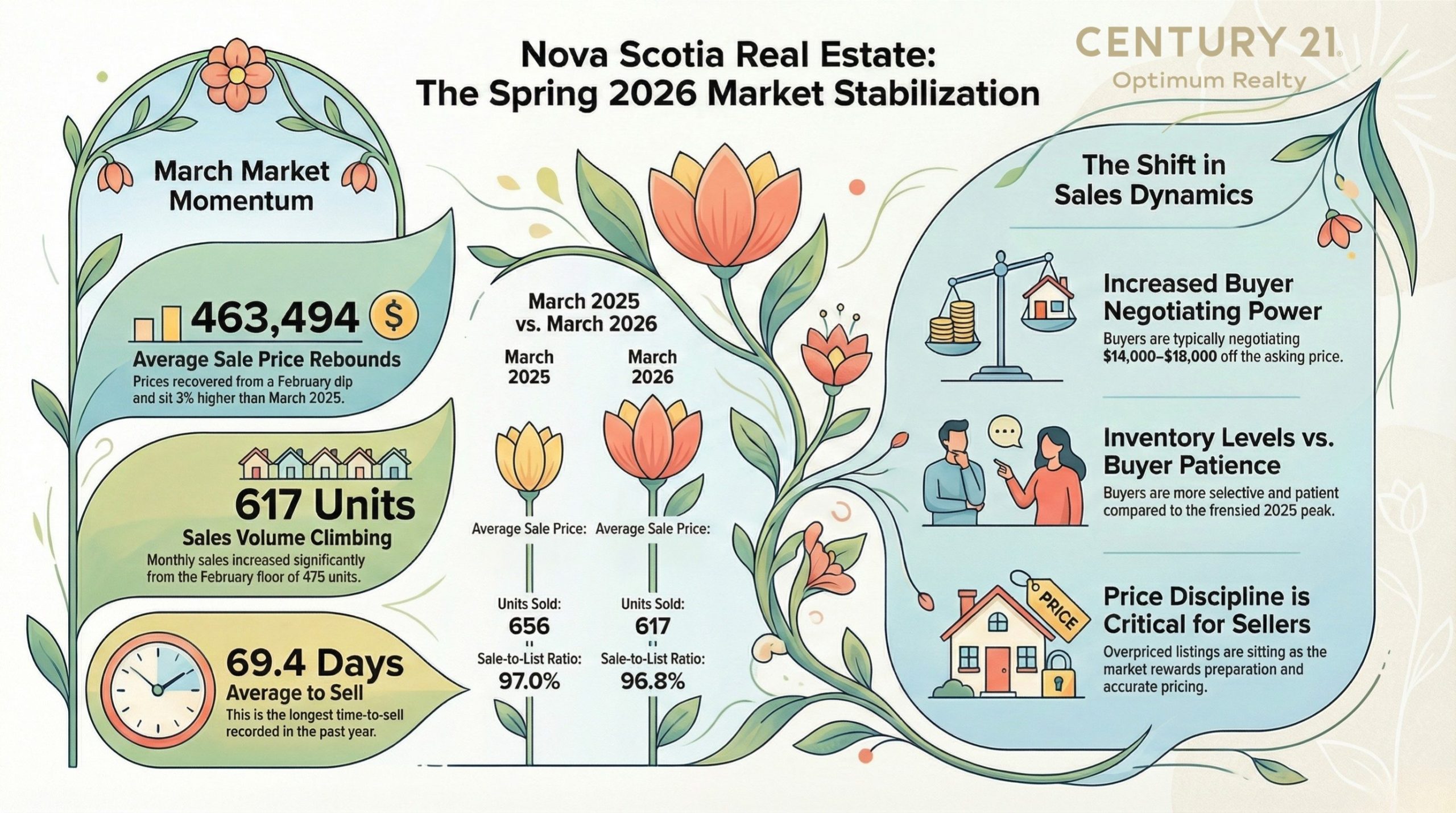

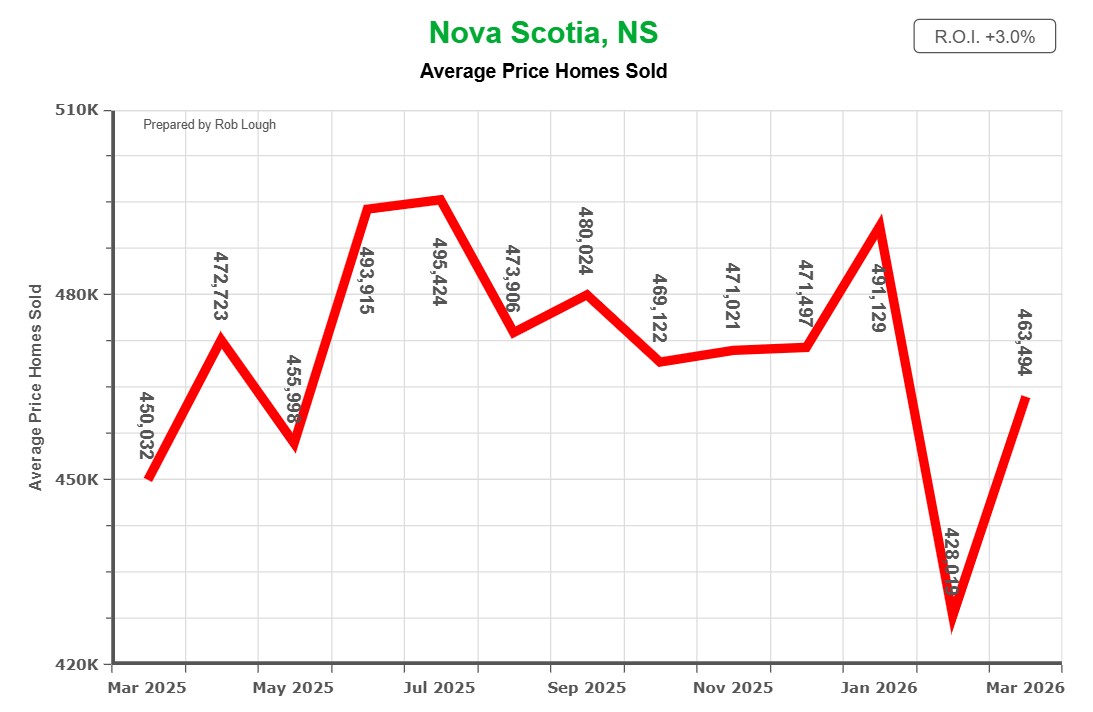

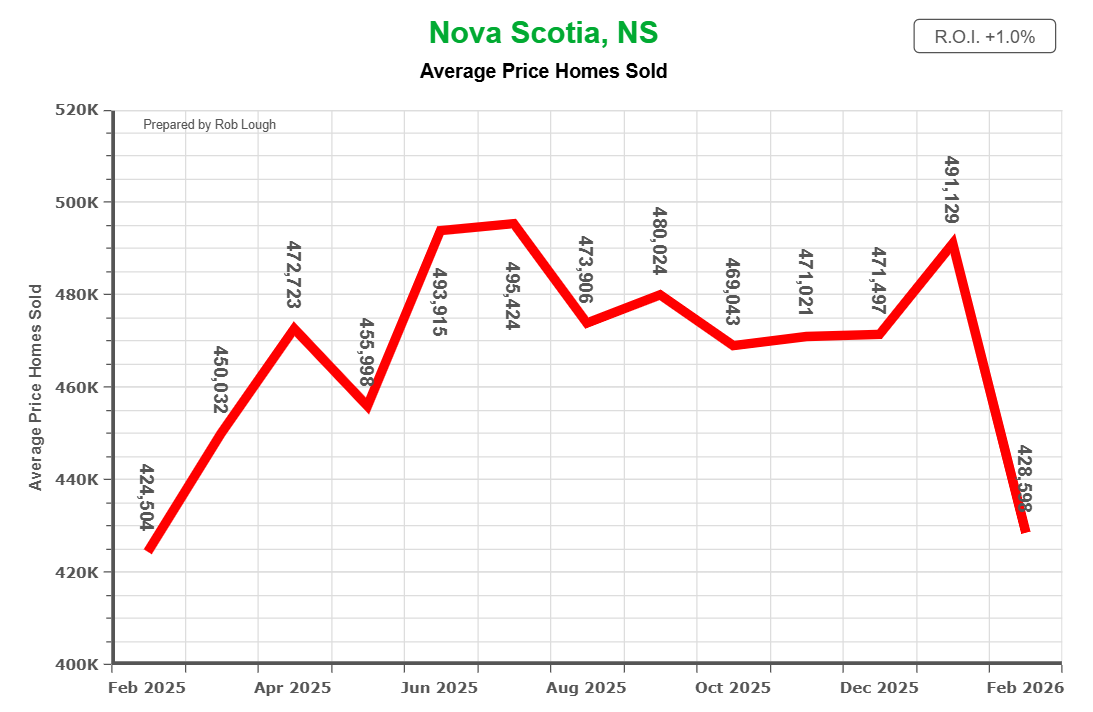

Average prices through the first quarter of 2026 have traced a classic seasonal arc: a record January high of $491,129 (up 11.3% year over year, the highest January average on record for the province), a predictable dip to $428,598 in February (essentially flat versus February 2025), and a March recovery to approximately $463,494, roughly 3% above March 2025.

That pattern, spike in January driven by higher-end closings, dip in February as the sales mix shifts, and a spring recovery as more properties transact, is textbook Nova Scotia seasonality. It does not signal a price correction. What it signals is a market behaving the way our market is supposed to behave.

For more detail on how January set up this year’s trends, see our Nova Scotia Real Estate Market Stats January 2026 report. And for a longer-range view of where this market has been, our Five Years of Nova Scotia Real Estate Market Analysis (2021–2025) puts today’s numbers in proper historical context.

Activity and Negotiation: Buyers Have Gained Leverage

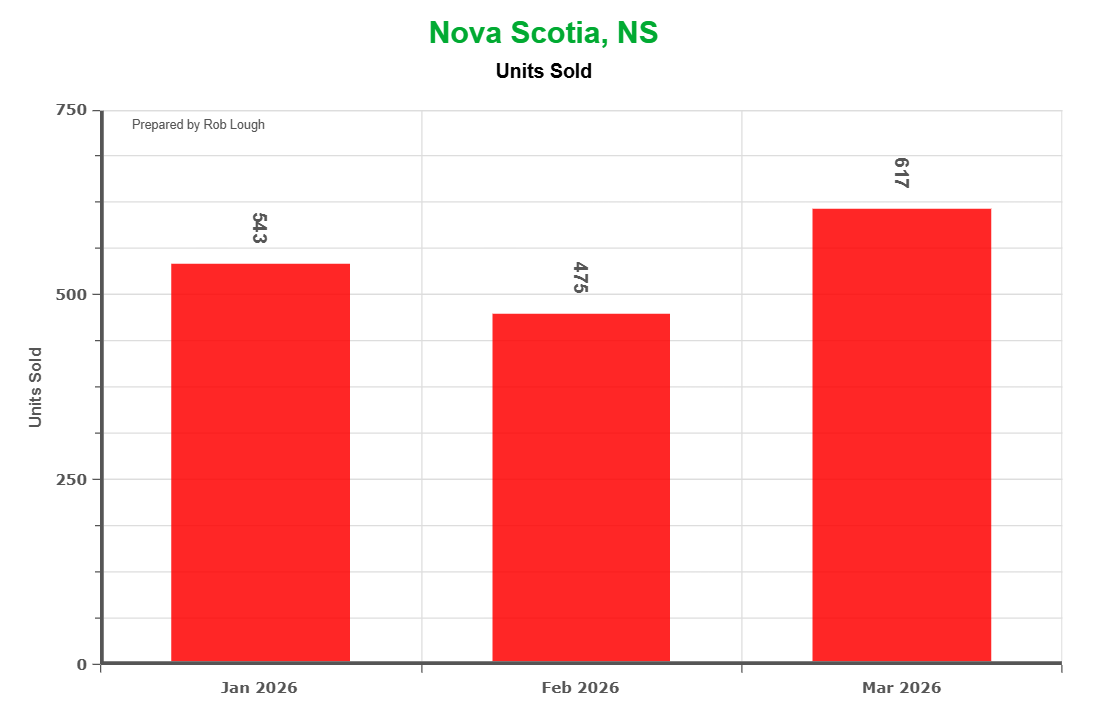

Number of homes Sold Spring 2026 Nova Scotia Real Estate

Fewer homes are selling, they’re taking longer to move, and buyers are negotiating harder. Those three facts are worth understanding together rather than in isolation.

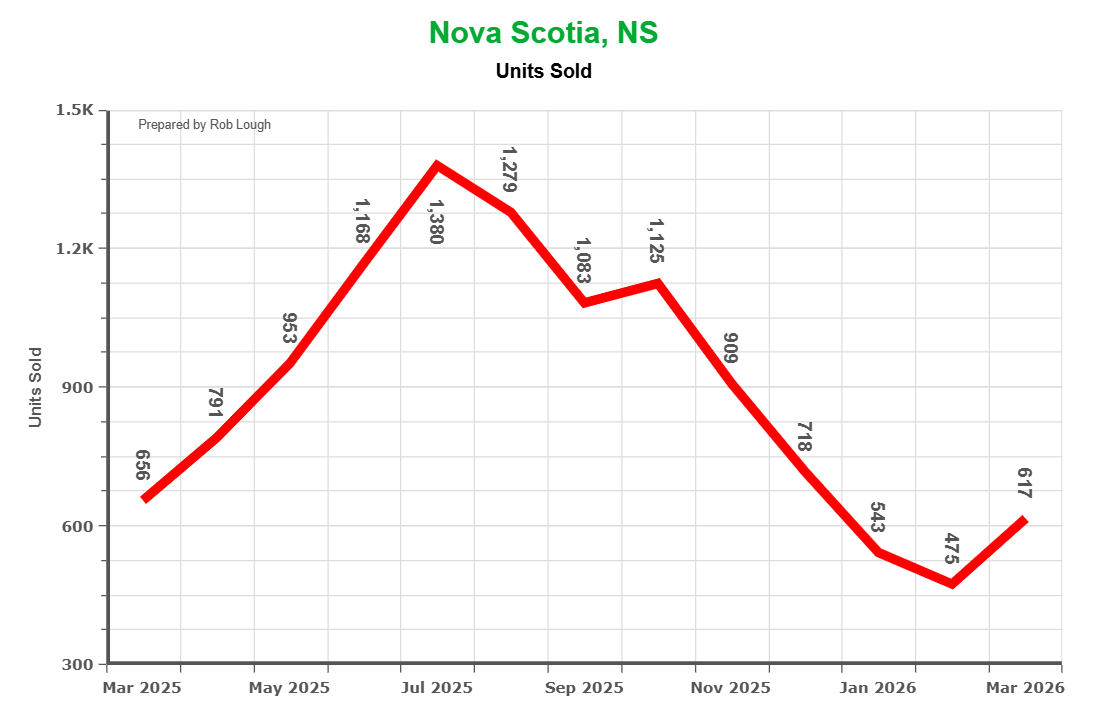

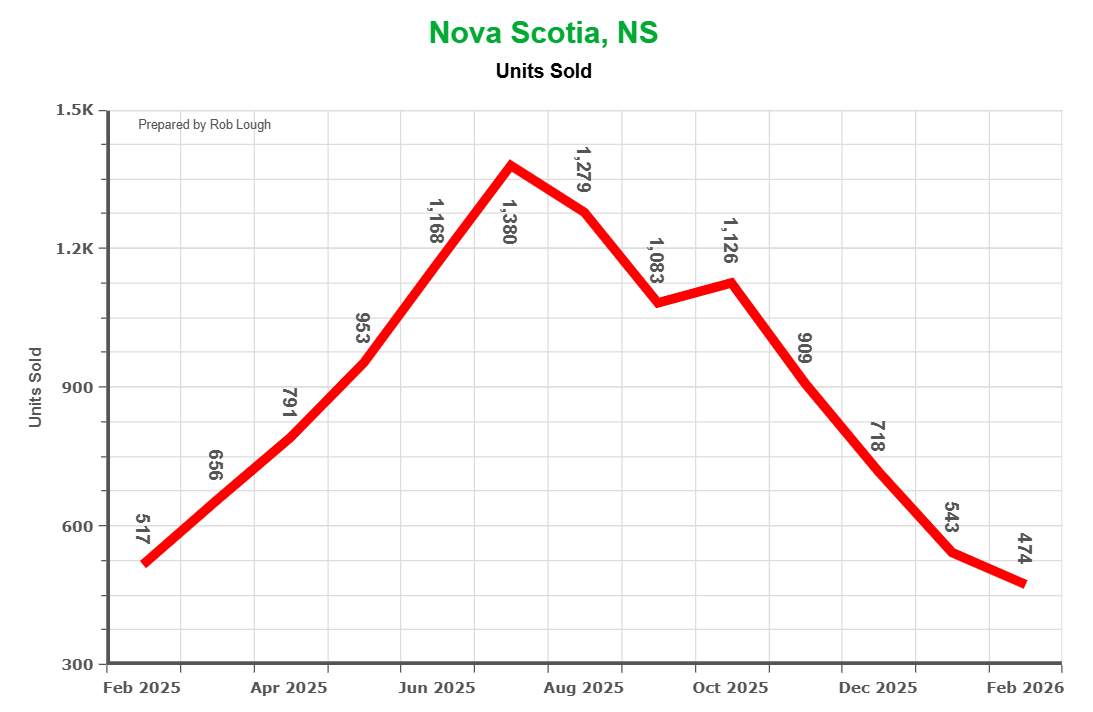

Units sold came in at 543 in January 2026, 474 in February, and 617 in March, all below the comparable 2025 months. The spring ramp is underway, but we’re not at last year’s summer pace of 1,000+ transactions per month yet.

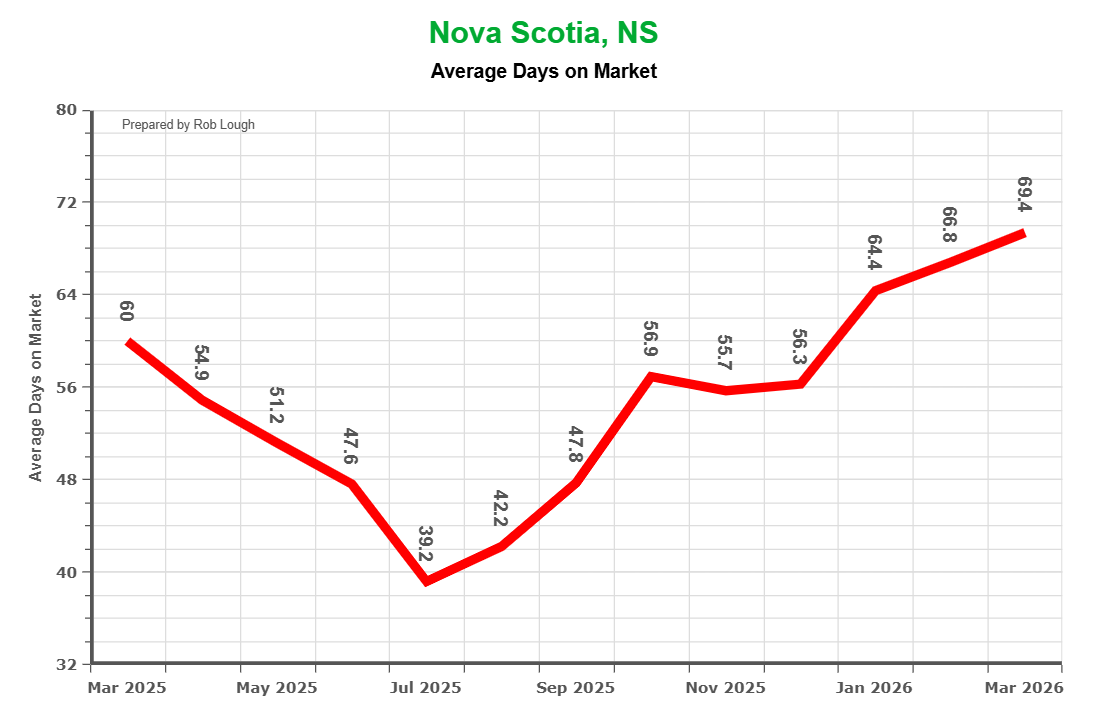

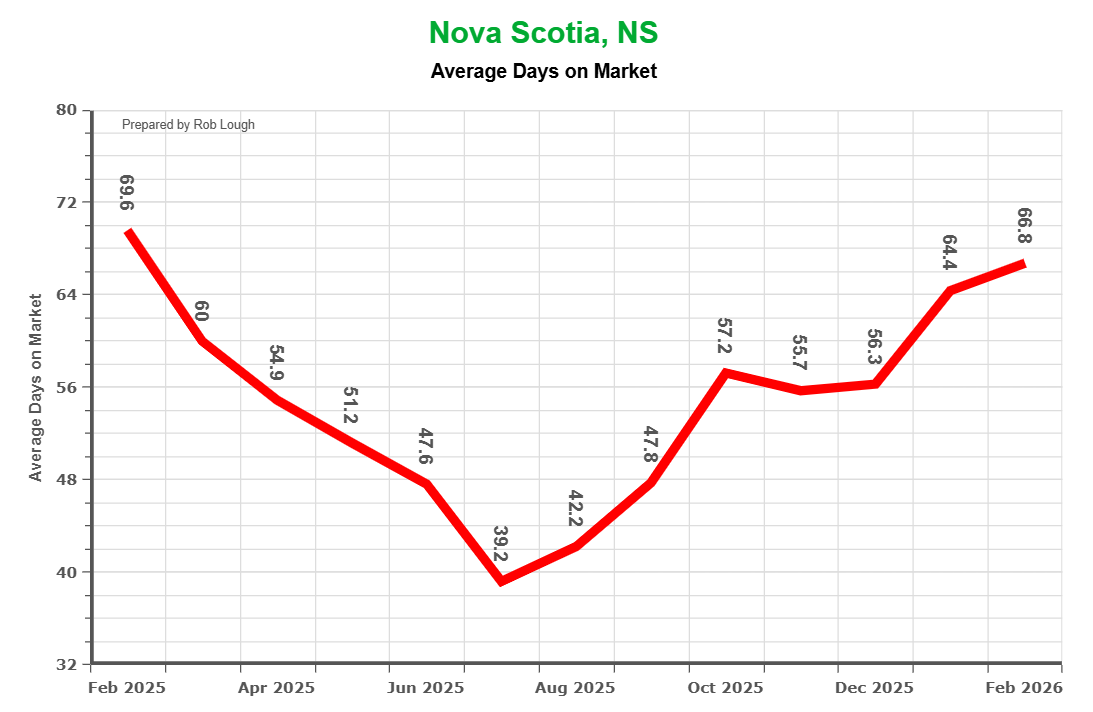

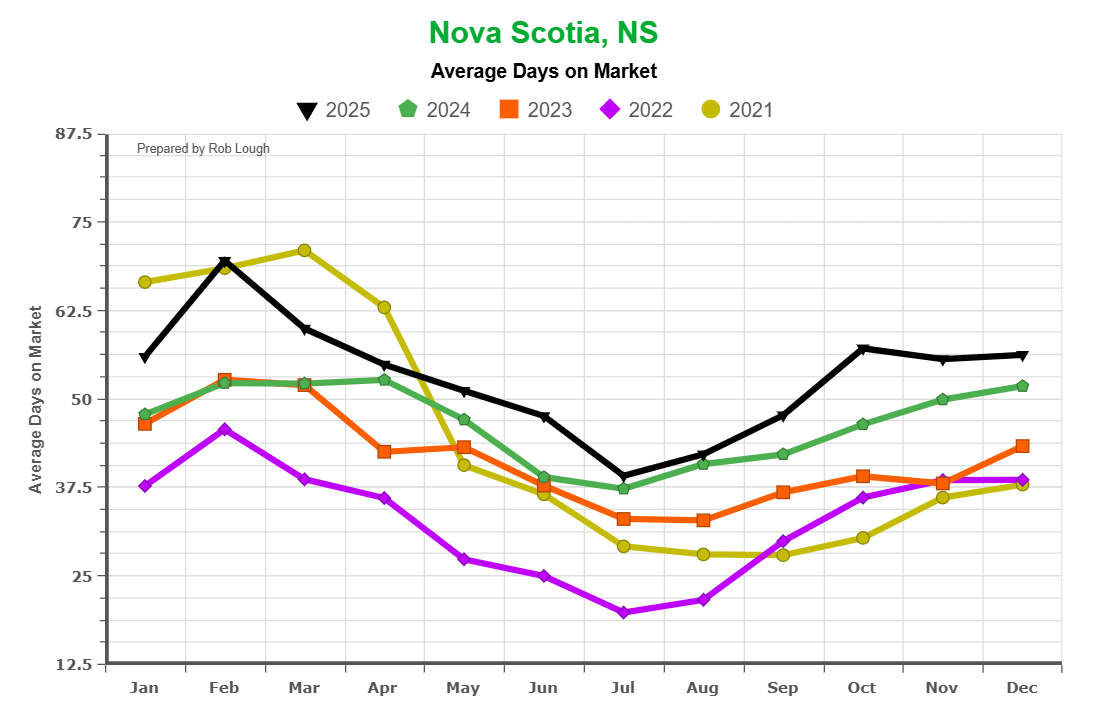

Days on market climbed from a summer 2025 low of 39.2 days all the way to 69.4 days in March 2026. Homes are sitting for more than two months on average before finding a buyer. That’s not alarming, our Ten Years of Nova Scotia Real Estate in Five Key Charts shows that pre-pandemic norms ran in the 60–90 day range, but it is a meaningful shift from what sellers experienced last year.

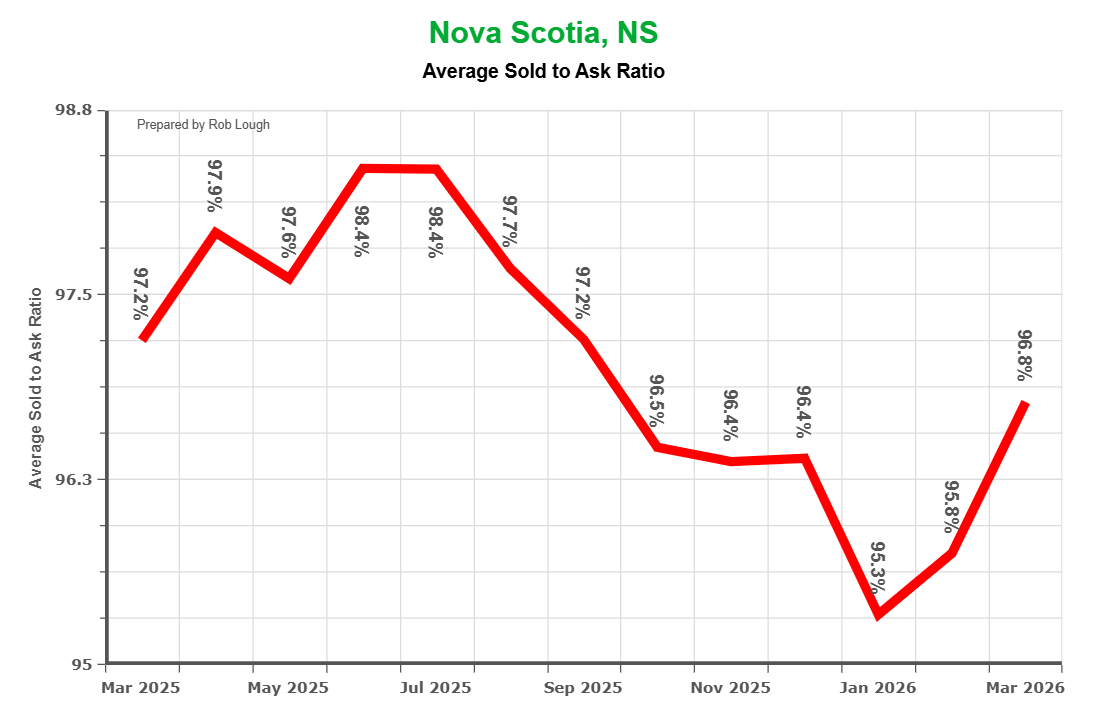

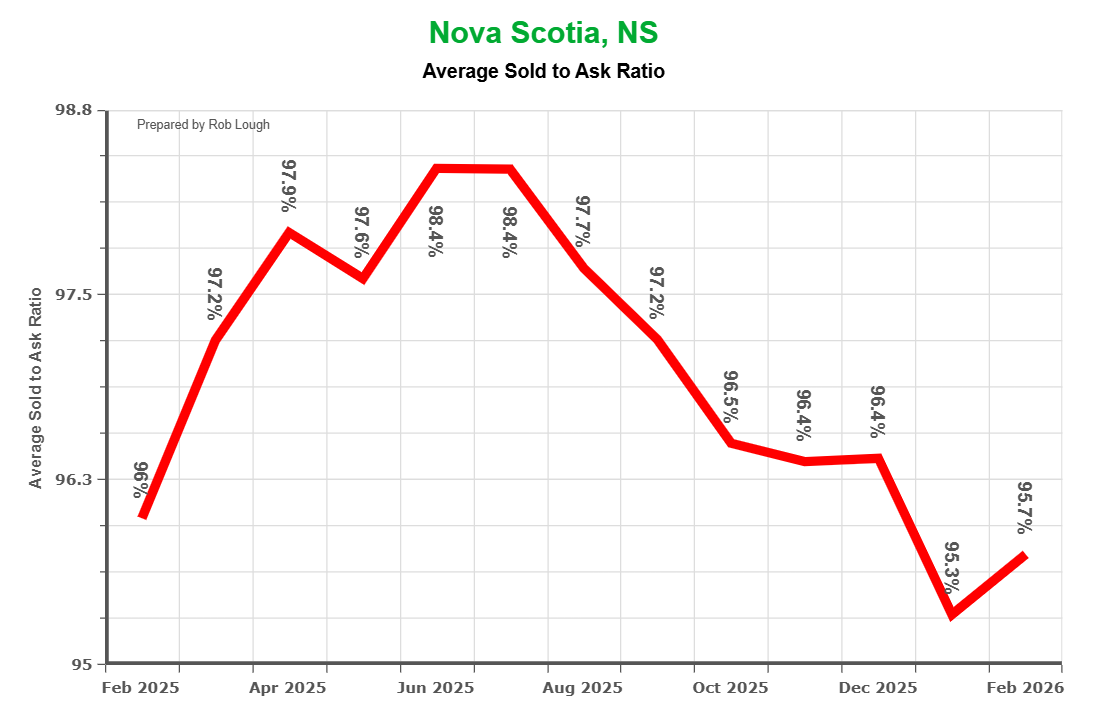

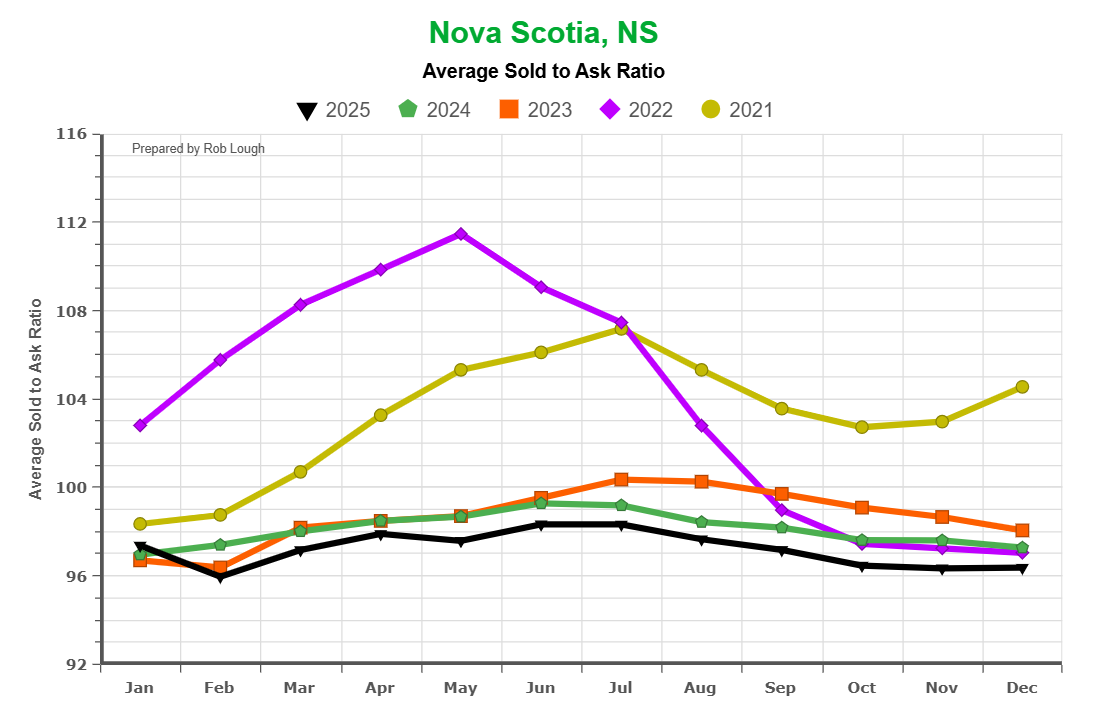

The sold-to-ask ratio tells a similar story. At 95.3% in January and 95.7% in February before recovering to 96.8% in March, buyers are typically negotiating roughly $14,000–$18,000 off the asking price on a $400–500K home. During the June–July 2025 peak, that ratio held at 98.4%, leaving buyers almost no room to move. That has changed.

For a closer look at our largest urban market through this period, the Halifax-Dartmouth Real Estate Market Stats January 2026 report shows how HRM’s numbers, including a 97% sold-to-ask ratio and 52.6 days on market, tracked slightly stronger than the provincial average, as the city typically does.

What to Expect This Spring

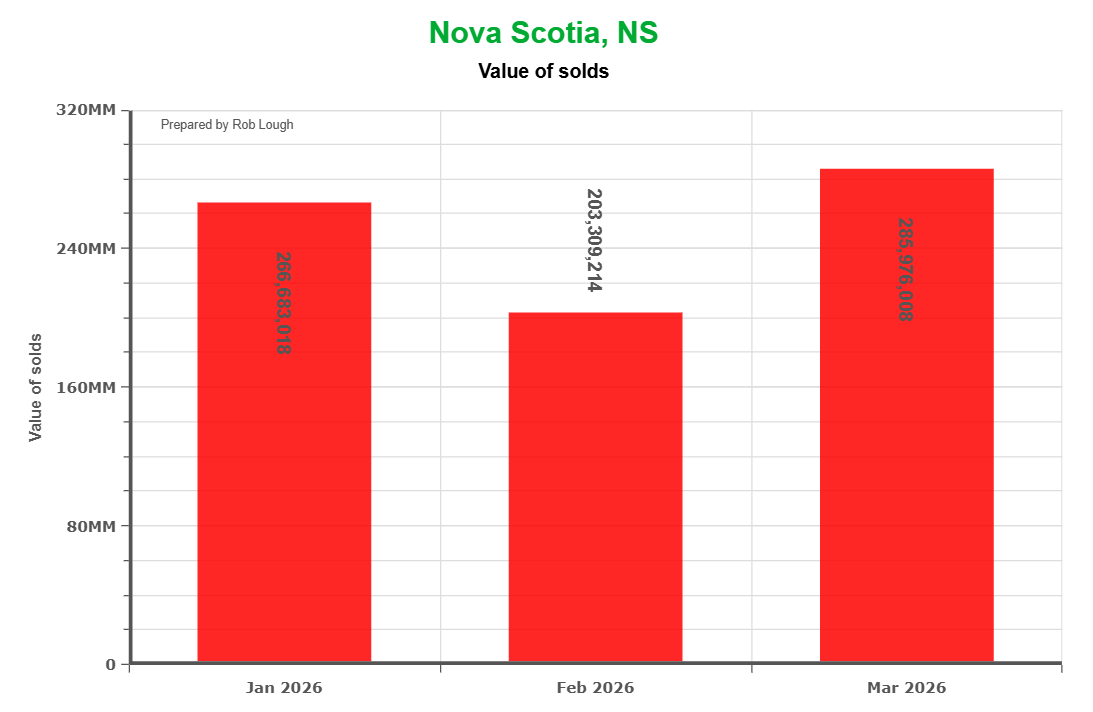

Value of homes Sold Spring 2026 Nova Scotia Real Estate

If past years are any guide, activity should pick up through April and May as the spring market takes shape. Listings increase, buyer foot traffic rises, and the sold-to-ask ratio firms as more competition returns to well-priced properties.

The seasonal arc in Nova Scotia is deeply embedded. We’ve seen it play out across multiple rate environments, supply conditions, and economic backdrops. Spring doesn’t erase the winter dynamics, but it does shift the balance. Sellers who sat through a quiet February and March will find more qualified buyers in front of their listings over the next sixty days. Buyers who have been shopping patiently will see more inventory arrive and in some pockets, more competition returning for the best properties.

The Bank of Canada holding its overnight rate at 2.25%, with prime sitting around 4.45%, means the borrowing environment is stable and predictable. That’s a meaningful support for buyer confidence heading into the busiest months of the year.

What This Means for Sellers

Price discipline is the single most important factor right now. With days on market approaching 70 days provincially and buyers negotiating 3–4% below asking on average, overpriced listings are not finding buyers, they’re training buyers to wait you out.

The good news: values have held. If you’re pricing from current, accurate comparables rather than summer 2025 nostalgia, you’re entering the spring market with a realistic chance of a timely sale. Our buying and selling tips page has practical guidance on positioning your property, and if you want to know what your home is actually worth in today’s conditions, our What’s My Home Worth? tool is the right starting point.

Sellers should also note that the first-time buyer pool is better supported right now than it’s been in years, with programs like Nova Scotia’s 2% Down Payment Program helping more entry-level buyers qualify. Properties priced at or below the first-time buyer threshold are well-positioned to attract motivated, program-eligible purchasers this spring.

What This Means for Buyers

This is one of the more favourable buying environments Nova Scotia has seen since before the pandemic surge. Days on market are long, negotiation room is real, and spring inventory is arriving. The urgency that pushed buyers into quick decisions with no conditions in 2022 and 2023 is not in this market right now.

That said, well-priced properties in desirable areas are still moving. Patience is an asset; complacency isn’t. When the right property comes along, being pre-approved and ready to act is what separates buyers who get the house from buyers who send another lowball offer on a listing that just sold.

Get pre-approved for a mortgage before you fall in love with a property. Use our mortgage calculator to model your monthly payments at today’s rates. And if you want to understand how programs can stack to make a new build significantly more affordable, our article on how Nova Scotia first-time buyers can stack federal and provincial programs is required reading.

What This Means for Investors

Flat year-over-year prices, softening sold-to-ask ratios, and longer days on market point to a potential entry window where fundamentals matter more than short-term appreciation. Underwriting should assume modest price growth and lean on rent income as the primary return driver. The 2026–27 Nova Scotia Budget introduced programs supporting rental housing supply, which shapes the competitive environment for income-property investors. Factor in the new investment property mortgage qualification rules that came into effect in January 2026 when running your numbers.

Bottom Line

Spring 2026 is arriving in a market that is normalizing, not collapsing. Prices are firm. Seasonal activity is returning. And buyers have more time, more inventory, and more negotiating power than they did at this point last year. A new province-wide NSAR survey puts hard numbers behind that sentiment — 73% of non-owners still want to buy, but 77% say housing is unaffordable.

For buyers, that’s opportunity. For sellers, it’s a call to meet the market rather than fight it. For investors, it’s a window to acquire with less competition and more realistic seller expectations.

Nova Scotia real estate remains fundamentally sound. Population growth, long-term economic investment in the region, and constrained new construction relative to demand all support the market over time. The question for spring 2026 is simply whether buyer confidence, and the listings to match it, can build into the kind of active market we saw a year ago.

We’ll be watching the April and May data closely.

Related Resources

- Nova Scotia Real Estate Market Stats March 2026

- Nova Scotia Real Estate Market Stats for February 2026

- Nova Scotia Real Estate Market Stats January 2026

- Nova Scotia Real Estate Market Statistics 2025

- Five Years of Nova Scotia Real Estate Market Analysis (2021–2025)

- Ten Years of Nova Scotia Real Estate in Five Key Charts

- Halifax-Dartmouth Real Estate Market Stats January 2026

- Nova Scotia’s 2% Down Payment Program

- How First-Time Buyers Can Stack Federal and Provincial Programs

- 2026–27 Nova Scotia Budget: What Buyers, Renters & Investors Need to Know

- Get Pre-Approved for a Mortgage

- Mortgage Calculator

- What’s My Home Worth?

- Buying and Selling Tips

Nova Scotia Real Estate Market Stats March 2026

Nova Scotia Real Estate Market Stats March 2026: Early Signs of Spring Stabilization

By Rob Lough | Century 21 Optimum Realty | April 2026

After a quiet winter stretch, Nova Scotia’s real estate market is showing familiar signs of seasonal life heading into spring 2026. March data reveals a bounce in prices, sales volume, and buyer activity, but with some important caveats for anyone thinking about buying or selling right now.

If you’ve been following our monthly reports, you’ll recognize the pattern: February hit a seasonal floor across nearly every metric, and March is now doing what March usually does. Here’s what the numbers are telling us this month.

Average Sale Price: Recovering from the February Dip

Average Price of homes sold Nova Scotia Real Estate Market stats March 2026

The average sale price in Nova Scotia rebounded to approximately $463,494 in March 2026, recovering from a sharp February dip to around $428,000. That puts prices roughly 3% above where they were in March 2025 (~$450,032), consistent with the R.O.I. figure shown on the chart.

What this means in plain terms: values have held up reasonably well over the past year, even as activity slowed through winter. Buyers who purchased in early 2025 have seen modest gains, and sellers who are priced correctly still have real equity working in their favour.

The broader pattern through 2025 showed prices plateauing in the $469–$495K range through summer and fall, before softening into the new year. If you want to see how that arc played out in full detail, our Nova Scotia Real Estate Market Statistics 2025 year-end report covers the complete picture. The March recovery suggests that seasonal demand is returning, but we’re not yet back to last spring’s peak territory.

Units Sold: Volume Improving, But Off Last Year’s Pace

Number of Units sold Nova Scotia Real Estate Market stats March 2026

Residential sales province-wide came in at 617 units in March 2026, up from 475 units in February and 543 units in January. That’s a meaningful improvement in momentum as the spring market gets underway.

For context, though, March 2025 saw 656 units change hands, and the market kept accelerating from there, hitting 1,083–1,380 sales per month through the peak summer period. Our February 2026 market report flagged this seasonal trough clearly, and March is now confirming that the market is stabilizing rather than deteriorating further.

We’re not at last year’s summer levels yet, and it’s worth watching whether the spring of 2026 follows a similar ramp-up or settles in at a more measured pace.

If you’re a seller wondering whether the buyers are out there, the answer is yes, however, they’re just more selective than they were eighteen months ago.

Days on Market: Listings Taking Longer to Sell

Average Days on market in Nova Scotia Real Estate Market stats March 2026

This is the chart that deserves the most attention from sellers right now. Average days on market climbed to 69.4 days in March 2026, the longest time-to-sell we’ve seen in the past year, and meaningfully higher than:

- The ~39–42 day lows recorded in July and August 2025

- The ~60 day starting point from March 2025

For a longer-range view of this trend, our Ten Years of Nova Scotia Real Estate in Five Key Charts article puts today’s days-on-market numbers in proper historical context, current absorption times are actually in line with pre-pandemic norms, even though they feel slow compared to the frenzied 2021–2022 period.

Properties are taking more than two months on average to find a buyer. That’s not a crisis, but it is a market that rewards preparation. Homes that are well-presented, properly staged, and accurately priced are still selling, they’re just competing against more inventory and more patient buyers than sellers were dealing with last summer.

This is exactly the kind of market where a proper comparative market analysis makes the difference between sitting on the market and actually closing.

Sale-to-List Ratio: Buyers Negotiating, But Not Winning Deeply

Average list to ask ratio in Nova Scotia Real Estate Market stats March 2026

The average sale-to-list ratio ticked up to 96.8% in March 2026, recovering from a January low of 95.3% — the weakest reading in the entire period tracked. For comparison, this ratio held in the 97–98.4% range through the spring and summer of 2025, when competition was higher and multiple offers were more common.

At 96.8%, buyers are typically negotiating approximately $14,000–$18,000 off the asking price on a $400–$500K home. That’s real money, and it reflects a market where sellers who overprice are getting pushed back.

The January low we flagged in our January 2026 market stats now looks like a seasonal floor. The slight uptick in March suggests that buyer confidence is returning as spring listing activity picks up, which is consistent with the seasonal patterns our Five Years of Nova Scotia Real Estate Market Analysis shows are deeply embedded in this market.

Total Sales Volume: Well Below 2025 Peaks

Value of Solds in Nova Scotia Real Estate Market stats March 2026

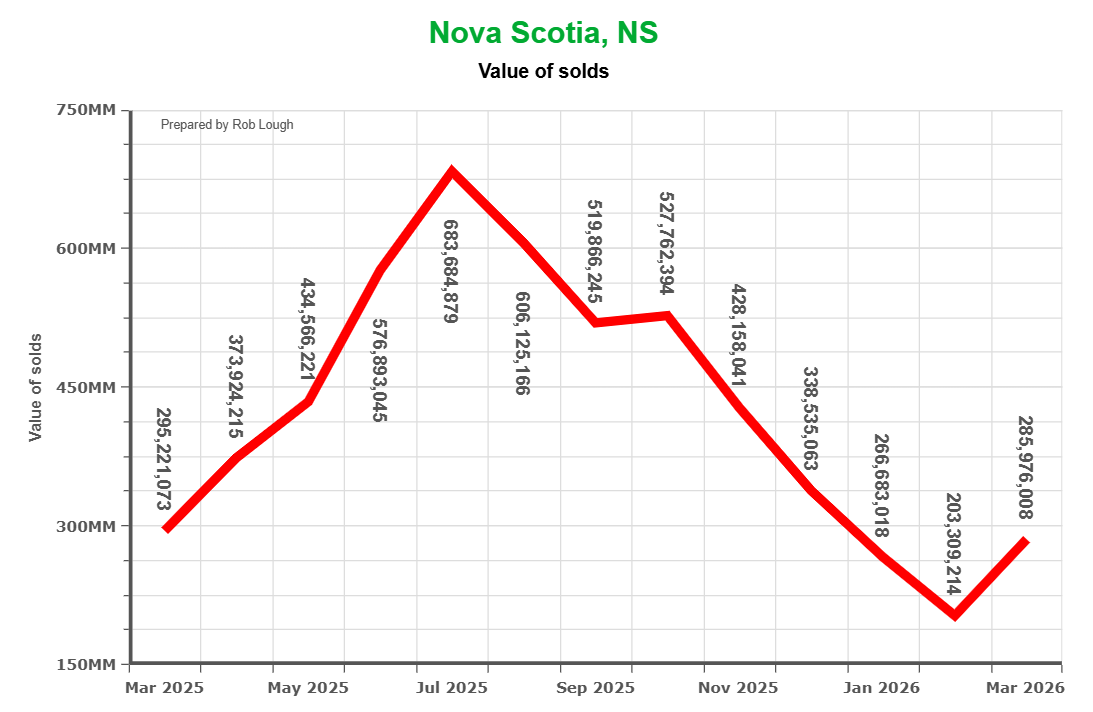

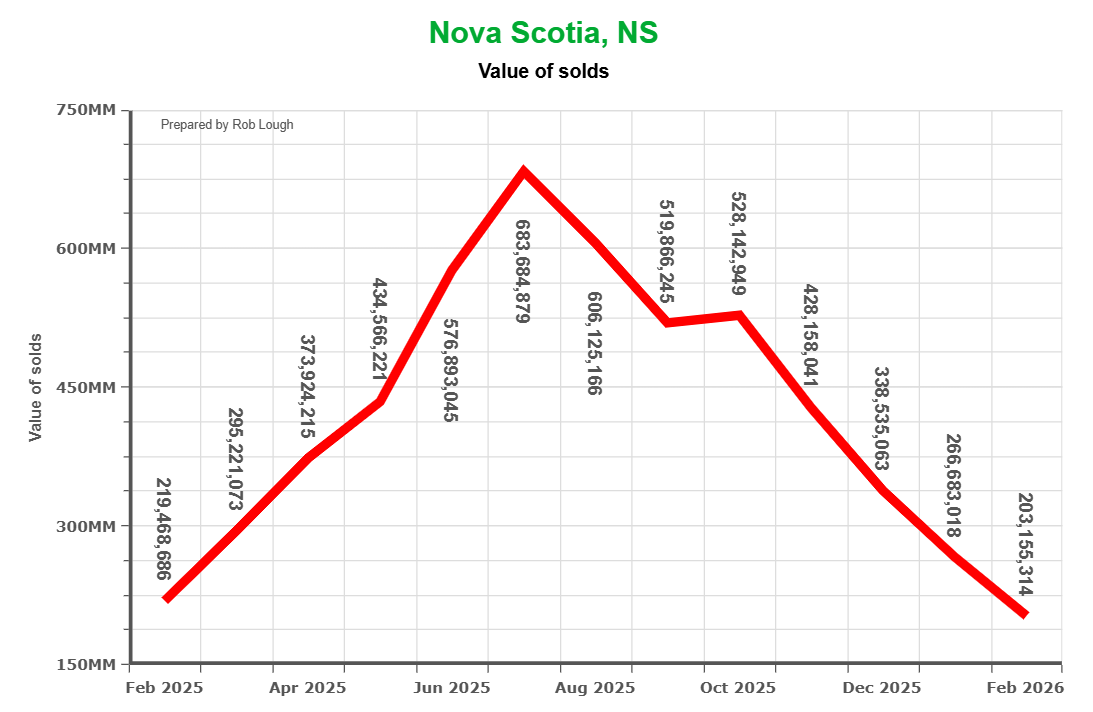

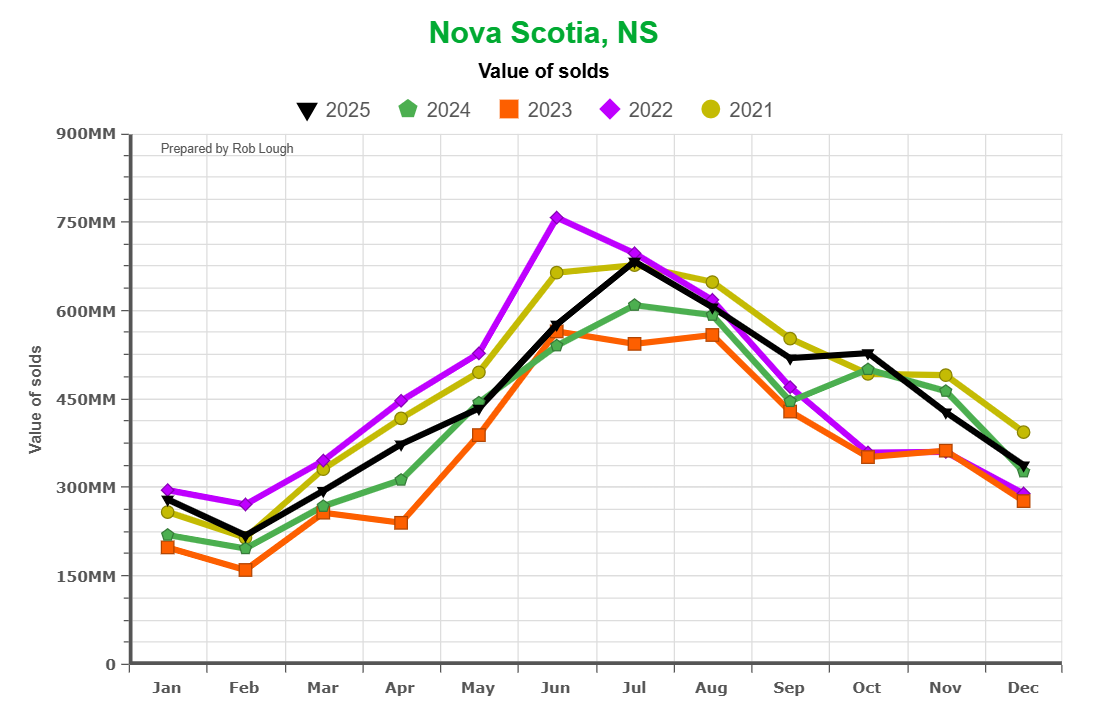

Total residential sales volume for March 2026 came in at approximately $285,976,008, nearly doubling February’s ~$203M low, but still well below the $606M–$683M monthly figures recorded at the height of the 2025 spring and summer market.

This reflects the combination of fewer sales and prices that, while stable, haven’t pushed into new territory. As we detailed in our November 2025 market stats, the May-through-August window accounts for a disproportionate share of annual dollar volume, the spring ramp-up is what we’ll be watching closely over the next 60–90 days.

For investors and developers watching aggregate market signals, total volume remains a useful barometer of overall market health. Right now it’s telling a story of a market in transition rather than acceleration. If you’re weighing investment decisions in that context, our breakdown of OSFI’s 2026 mortgage rule changes is required reading.

What This Means for Buyers and Sellers This Spring

For Buyers: You have more negotiating room than you did a year ago, and more time to make decisions. Days on market are up, sale-to-list ratios have softened, and spring inventory is beginning to arrive. First-time buyers in particular should know that Nova Scotia currently offers meaningful support through the 2% Down Payment Program, and there are ways to stack federal and provincial programs together to make new construction significantly more affordable. That said, well-priced homes in desirable areas are still moving. Get your mortgage pre-approval in order now so you’re ready to act when the right property appears. New NSAR research confirms that 77% of Nova Scotians consider housing unaffordable right now here’s what that data means for buyers and sellers in 2026.

For Sellers: Price discipline matters more than it has in years. With average days on market approaching 70 days and buyers negotiating down 3%+ from asking, overpriced listings are sitting. The good news is that values have held, but you need to meet the market, not fight it. The 2026–27 Nova Scotia Budget introduced new programs supporting first-time buyers and rental housing supply, both trends that support the buyer pool available to you this spring. Presentation, pricing, and professional marketing are the levers you control. If you’re thinking about listing, start with our sellers page or request a current market evaluation.

Bottom Line

March 2026 looks like the beginning of a spring stabilization after a soft winter. Prices are recovering, sales are climbing from seasonal lows, and the sale-to-list ratio is firming, all positive signals. But days on market are longer than last year, volume is well off the 2025 highs, and buyers are approaching the market with more patience and more negotiating confidence.

Nova Scotia real estate remains fundamentally sound. As we showed in our comprehensive 2025 market analysis, population growth, limited new construction relative to demand, and long-term economic investment in the region all support the market over time. The question for spring 2026 is whether buyer confidence and the listing inventory to meet it, can build into a more active market than last winter suggested.

We’ll be watching closely.

Related Resources

- Nova Scotia Real Estate Market Stats – February 2026

- Nova Scotia Real Estate Market Stats – January 2026

- Nova Scotia Real Estate Market Statistics 2025 – Year in Review

- Ten Years of Nova Scotia Real Estate in Five Key Charts

- Five Years of Nova Scotia Real Estate Market Analysis (2021–2025)

- Nova Scotia’s 2% Down Payment Program

- How First-Time Buyers Can Stack Federal and Provincial Programs

- OSFI’s 2026 Mortgage Changes: Impact on Investors

- 2026–27 Nova Scotia Budget: What Buyers, Renters & Investors Need to Know

How Nova Scotia First-Time Buyers Can Stack Federal and Provincial Programs to Make New Construction More Affordable

How Nova Scotia First-Time Buyers Can Stack Federal and Provincial Programs to Make New Construction More Affordable

By Rob Lough, Broker/Owner | Century 21 Optimum Realty | Halifax-Dartmouth, Nova Scotia Published: March 2026

Buying a brand-new home in Nova Scotia has never come with more government support than it does right now. Between a new federal GST rebate, provincial down payment programs, and changes to mortgage rules, first-time buyers of new construction have access to a combination of tools that can meaningfully lower the cost of getting into the market. That gap is backed by data, a 2026 NSAR survey found 77% of Nova Scotians say housing is unaffordable, while 73% of non-owners still want to own someday.

The challenge for most buyers is that these programs exist in different places, administered by different levels of government, and rarely explained together in one place. This article does exactly that. Think of it as your plain-language guide to understanding every major program available to you, how each one works independently, and how they stack together to improve your overall affordability picture.

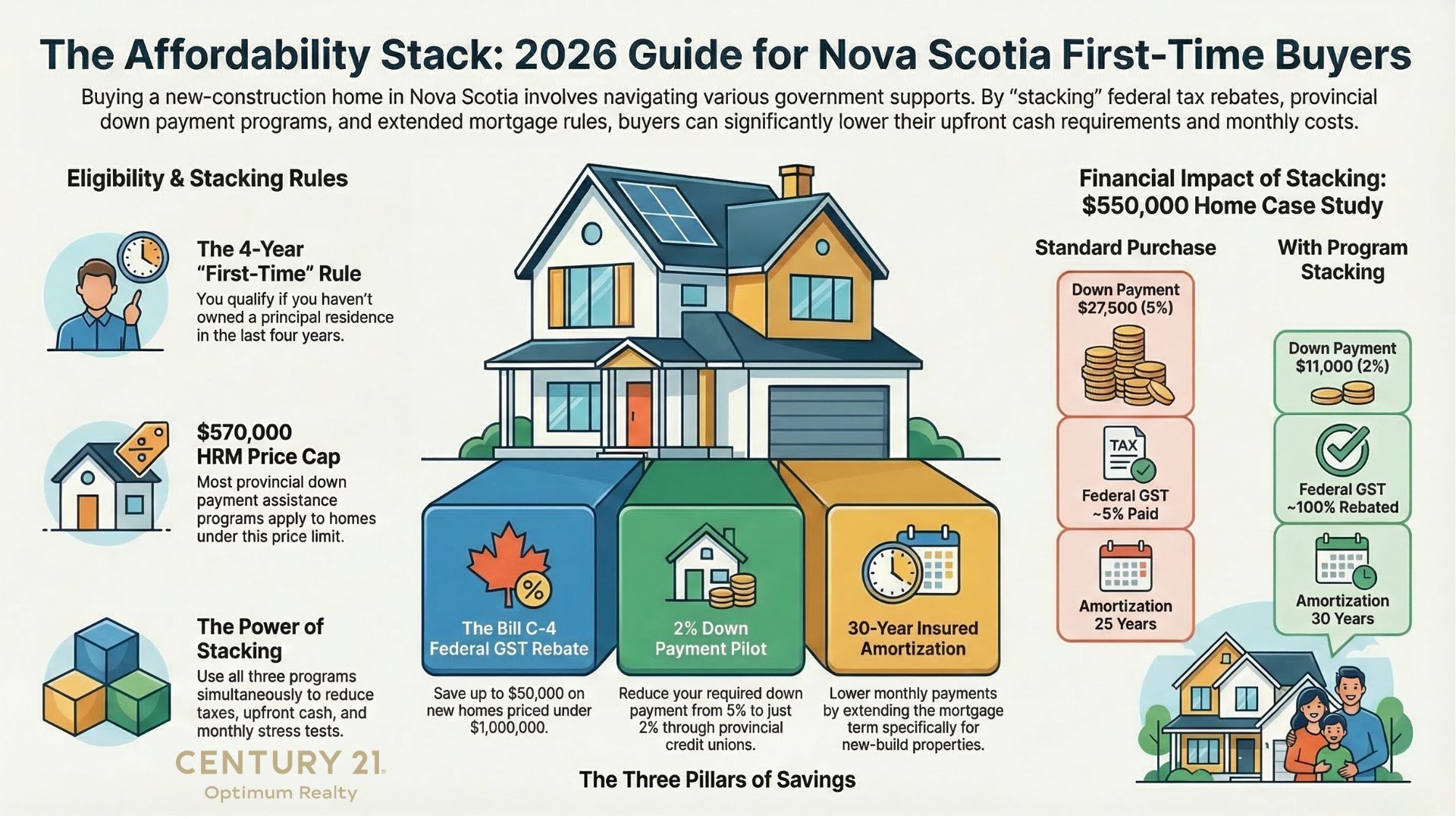

Start With the Biggest New Tool: The Federal GST Rebate Under Bill C-4

The most significant recent change is the passage of Bill C-4, the Making Life More Affordable for Canadians Act, which received Royal Assent on March 12, 2026. This legislation amends the Excise Tax Act to create an enhanced GST rebate specifically for first-time buyers of new homes.

Here is the core of how it works:

The program removes the 5% federal GST (or the federal portion of HST) on qualifying new homes priced up to $1,000,000. On a home priced at $1,000,000, the maximum federal savings are approximately $50,000. Between $1,000,000 and $1,500,000, the benefit phases out proportionally. Above $1,500,000, the enhanced rebate disappears.

To be eligible, the home must be new construction or substantially renovated, not a resale property. The Agreement of Purchase and Sale with the builder must be dated on or after March 20, 2025, and before 2031. You must occupy the home as your primary residence and be the first occupant after construction is complete.

For buyers in HRM, this matters a great deal. A large share of new-build townhomes and condos across Halifax Regional Municipality are priced under $1,000,000, putting the full rebate within reach for many local first-time buyers, not just buyers in Toronto or Vancouver.

Understanding the Eligibility Test for “First-Time Buyer”

Before layering programs, it helps to understand what “first-time buyer” means under federal rules, because not all programs use identical definitions.

Under the federal framework, a first-time buyer is generally someone who has not owned a home used as their principal residence at any time during the preceding four years. There is also a provision for buyers who have gone through a separation or divorce, which may allow them to qualify even if they previously owned a home with a former spouse. You can read more about how that works in the context of Nova Scotia programs at the Century 21 Optimum Realty listings and resources page.

The important takeaway is that first-time buyer status is not just for people who have never owned anything. It is worth reviewing your personal history carefully, especially if you owned a home that was sold more than four years ago.

Layer Two: Nova Scotia’s 2% Down Payment Program

The second tool available to qualifying buyers is Nova Scotia’s First-Time Homebuyers Program, a provincial pilot that allows eligible buyers to purchase a home with as little as a 2% down payment, backed by a provincial guarantee. Under standard rules, most buyers need at least 5% down, which on a $500,000 home means $25,000 in cash. Under this program, that drops to $10,000, potentially shaving months or years off the time it takes to save enough to buy.

The program is delivered through participating credit unions in Nova Scotia. There is no traditional CMHC mortgage default insurance required, which eliminates a cost that would otherwise be added to the mortgage amount for high-ratio purchases.

Eligibility requirements include being a Nova Scotia resident, meeting the first-time buyer definition, passing a standard mortgage stress test, and staying within purchase price limits. In HRM and East Hants, the maximum eligible purchase price is $570,000.

The full details are covered in the Nova Scotia 2% Down Payment Program explainer on the C21 Optimum site.

Key point for stacking: This program applies to the purchase price, not the GST component. A buyer using the 2% down program on a new build under $570,000 could potentially access both the reduced down payment and the federal GST rebate on the same transaction, subject to meeting all eligibility criteria for each.

Layer Three: Nova Scotia’s Down Payment Assistance Program

Separate from the 2% pilot, Nova Scotia also has a Down Payment Assistance Program (DPAP) administered directly by the province. This program provides an interest-free loan of up to 5% of the purchase price to qualified buyers who cannot afford the down payment on their own.

The price cap in HRM is $570,000. Buyers must be first-time purchasers, the home must be their primary residence, and they must not already have the financial means to cover the 5% requirement independently.

The Nova Scotia Down Payment Assistance Program overview walks through the specific documentation requirements, application timelines, and eligibility rules in full detail.

Layer Four: The 30-Year Insured Amortization for New Builds

On top of the rebate and down payment programs, federal mortgage rule changes now allow first-time buyers of new construction to extend their insured mortgage to a 30-year amortization, up from the standard 25 years.

Why does this matter? A longer amortization reduces your monthly mortgage payment, which can make a real difference in whether you pass the mortgage stress test and how much home you can afford. The reduction in monthly payments does mean you pay more interest over the life of the loan, so it is a trade-off worth discussing with your mortgage broker, but for buyers whose primary hurdle is qualifying, it is a meaningful tool.

This rule is specifically available to first-time buyers purchasing new builds, not resale homes, which makes it particularly relevant to anyone considering the types of new construction projects where the Bill C-4 GST rebate would also apply.

Layer Five: The Nova Scotia Budget and HST Relief for New Rental Construction

The 2026-27 Nova Scotia provincial budget also introduced HST relief for developers building new multi-unit rental housing. While this does not directly benefit individual first-time buyers, it is worth understanding because it will gradually increase the supply of new-build units across HRM and surrounding areas, which affects pricing and availability over time.

The full breakdown of the 2026-27 Nova Scotia Budget housing measures covers all the supply-side programs in detail.

How These Programs Work Together: A Practical Example

Consider a qualifying first-time buyer purchasing a new-build townhome in HRM for $550,000:

Under Bill C-4, the full 5% GST on the $550,000 purchase price could be rebated. That is approximately $27,500 returned to the buyer, either credited by the builder at closing or claimed directly from CRA.

Under the 2% Down Payment Program, that same buyer could enter with $11,000 down instead of $27,500, freeing up capital for closing costs, moving expenses, or an emergency fund.

With a 30-year insured amortization, the monthly payment on the resulting mortgage is lower than it would be under the standard 25-year term, potentially improving stress-test qualification.

None of these programs replace each other. They address different parts of the affordability challenge: one reduces the tax cost of the purchase, one reduces the cash required upfront, and one improves monthly payment qualification. When used together by an eligible buyer on an eligible property, the cumulative effect is substantial.

What Buyers Need to Do Next

Understanding the programs is step one. The practical steps that follow matter just as much.

Get pre-approved first. Before approaching any builder or making any offers, you need to know your budget with precision. Pre-approval also locks in your rate for 90 to 120 days while you search. The current market context, including price trends and what inventory looks like across the province, is covered in the Nova Scotia Real Estate Market Stats for January 2026.

Confirm your Agreement of Purchase and Sale date. The Bill C-4 rebate requires that your agreement with the builder be dated on or after March 20, 2025. If you are unsure whether your purchase qualifies, your lawyer or REALTOR can help you confirm.

Apply for DPAP at least two weeks before your financing deadline. The Nova Scotia Down Payment Assistance Program requires an application window before your offer goes firm. Missing this deadline means missing the program for that transaction.

Work with professionals who understand how these programs interact. A mortgage broker familiar with the provincial credit union 2% program, a real estate lawyer who understands CRA rebate mechanics, and a REALTOR who works in the new construction segment are all valuable on the same transaction.

Bold Buyer Takeaway

If you are a first-time buyer of new construction in Nova Scotia in 2026, you are operating in the most program-supported environment we have seen in years. The federal GST rebate is law, provincial down payment tools are active, and 30-year insured amortizations are available for new builds. No single program solves the affordability challenge on its own. Used together, they change the math significantly.

Ready to start the conversation? Contact us at Century 21 Optimum Realty for a no-obligation discussion about what these programs mean for your specific situation.

Related Resources

- Nova Scotia’s 2% Down Payment Program

- Nova Scotia Down Payment Assistance Program

- 2026-27 Nova Scotia Budget: Housing Measures Explained

- Nova Scotia Real Estate Market Stats January 2026

- Nova Scotia Housing Market 2025: Comprehensive Analysis

- Browse Current Listings

- Contact Century 21 Optimum Realty

Nova Scotia Real Estate Market Stats for February 2026

Nova Scotia Real Estate Market Stats for February 2026

By Rob Lough, Broker/Owner | Century 21 Optimum Realty Published: March 2026

February’s numbers are in, and they paint a clear picture of where Nova Scotia’s real estate market stands heading into spring 2026. The frenzy of mid-2025 has given way to a more measured pace, with longer days on market, softer sold-to-ask ratios, and fewer transactions. But before anyone hits the panic button, the headline worth remembering is this: prices are essentially flat year over year, and the seasonal patterns we’re seeing are entirely normal for our province.

If you missed the year-end wrap-up, our Nova Scotia Real Estate Market Statistics 2025 article provides the full context for how we got here. And for a longer-range view of where this market has been, our Five Years of Nova Scotia Real Estate Market Analysis (2021-2025) breaks down the full transformation.

Let’s dig into the February 2026 data.

Average Home Prices: Flat Year Over Year

The average sale price for Nova Scotia homes in February 2026 came in at $428,598, down from a January 2026 spike to $491,129 but sitting just about 1% above where we were in February 2025 ($424,504). That +1.0% year-over-year return on investment tells an important story: this is not a market in freefall.

Average Price home sold Nova Scotia Real Estate Market Stats for February 2026

Prices climbed steadily through the spring and summer of 2025, peaking in the high $490s in June and July before oscillating in the $469,000 to $491,000 range through the fall and early winter. The February dip reflects the seasonal compression we see every year when buyer activity drops and the mix of properties closing shifts toward lower price points.

For sellers, your property’s value hasn’t evaporated. The market has simply reset to its normal seasonal rhythm after an unusually active 2025. Pricing strategy matters more than ever right now, and if you’re thinking about listing this spring, our sellers guide is worth a look.

For buyers, the flattening of prices means you’re not chasing a runaway market. There is breathing room to make smart, informed decisions without feeling like every week of hesitation costs you thousands.

Units Sold: Winter Slowdown Is Textbook

Nova Scotia recorded 474 home sales in February 2026, down from 543 in January and a significant step back from the summer 2025 peak of 1,380 units in July. For context, February 2025 saw 517 sales, so we’re looking at a modest year-over-year decline of about 8%.

Number of Units Sold Nova Scotia Real Estate Market Stats for February 2026

The seasonal arc here is textbook for our province. Sales ramp from roughly 500 in the late winter months through the spring, peak in the 1,100 to 1,400 range during summer, and then bleed off steadily through fall and winter. Nothing in this data suggests anything other than normal cyclical behaviour.

Total Dollar Volume: Following the Seasonal Script

The total value of homes sold in February 2026 was $203,155,314, representing the lowest point in the trailing 12-month period. At the summer peak in July 2025, that figure was $683,684,879, more than triple February’s total.

Value of sold properties Nova Scotia Real Estate Market Stats for February 2026

This drop reflects both fewer transactions and the seasonal pricing dip working together. It does not indicate a structural shift in market fundamentals. As listing activity picks up through March and April, expect this number to climb in step with the spring buying season.

Days on Market: Buyers Have Time to Think

Average days on market in February 2026 reached 66.8 days, nearly back to February 2025’s reading of 69.6 days. This represents a dramatic shift from the summer trough of just 39.2 days in July 2025, when well-priced homes were moving in under six weeks.

Average Days on Market Nova Scotia Real Estate Market Stats for February 2026

The DOM trend has traced a clear U-shape over the past year: falling from the low 70s in winter 2025 through to the high 30s at the summer peak, then climbing steadily back to current winter levels. This pattern reflects strong spring and summer absorption followed by the predictable seasonal slowdown.

For sellers, plan for 60 to 70 days on market rather than assuming a two-week sale. Staging, professional photography, and strategic pricing are your best tools for standing out when buyers have more options and more time to shop. Our buying and selling tips page has practical guidance for positioning your property.

For buyers, the current DOM environment works in your favour. You have time to do your due diligence, schedule inspections without pressure, and negotiate without feeling rushed. If you haven’t started the mortgage process yet, getting pre-approved should be your first step.

Sold-to-Ask Ratio: Room to Negotiate

The average sold-to-ask ratio for February 2026 was 95.7%, a slight uptick from January’s 95.3% but well below the summer 2025 highs of 98.4% in June and July.

Sold to ask Ratio Nova Scotia Real Estate Market Stats for February 2026

This is a meaningful shift from where we were six months ago. During the competitive summer months, homes were selling at near-full asking price and sometimes over ask. Today, typical discounts are running in the 4% to 5% range, indicating less competitive bidding and significantly more room for negotiation.

Ratios rose from about 96% in February 2025 to just under 99% by late spring, then steadily trended downward through the fall and into 2026. That trajectory tells us the urgency that defined last year’s peak season has faded, and the balance of power has shifted modestly toward buyers.

Interest Rates and the Broader Picture

The Bank of Canada held its overnight rate at 2.25% at its January 28 announcement, with the next decision date set for March 18, 2026. Most analysts expect rates to hold steady through the spring, providing a predictable borrowing environment for both buyers and sellers.

With prime rate sitting around 4.45%, variable rate mortgage holders are in a stable position, and fixed rate offerings remain competitive. If you’re considering a purchase, our mortgage calculator can help you run the numbers for your situation.

For first-time buyers, it’s also worth knowing about Nova Scotia’s 2% Down Payment Program, which can significantly reduce the upfront cash required to enter the market. We’ve also covered how first-time buyers in Canada face a tougher climb than past generations and what strategies are working right now.

What This Means for You

If you’re selling: Pricing sharply matters again. The days of listing high and letting the market come to you are behind us for now. Expect more conditional offers, longer timelines, and buyers who are doing their homework. Differentiation is key because buyers have options. Invest in staging, quality photography, and a realistic pricing strategy informed by current comparables, not summer 2025 comps. If you want to understand what your home is worth in today’s conditions, our free home valuation tool is a good starting point.

If you’re buying: This is a more balanced to mildly buyer-leaning environment than anything we’ve seen since 2021. You can negotiate on price and terms, look at listings that have been sitting for a while, and take the time to find the right property rather than scrambling to compete. Don’t let early spring optimism push you into a decision without solid comparable sales data backing it up. Our buyers guide walks through the process step by step.

If you’re investing: Flat year-over-year prices, softening ratios, and rising days on market point to a potential entry window where cash flow and yield matter more than quick appreciation. Underwriting should assume modest or zero short-term price growth and focus on rent fundamentals. Keep in mind that investment property mortgage rules changed in January 2026, so factor those new qualification requirements into your planning.

Looking Ahead to Spring 2026

If you’ve been watching from the sidelines, our recent Spring 2026 in Halifax article outlines exactly what to expect and how to prepare. The spring market typically brings a surge in both listings and buyer activity, and this year should be no exception.

Nova Scotia’s population growth continues to support housing demand, even as the pace has moderated from pandemic-era highs. Combined with stable interest rates and a construction sector that’s been ramping up new starts, the outlook for 2026 is one of measured activity and incremental price stability rather than dramatic swings in either direction. New province-wide NSAR research backs this up, 77% of Nova Scotians say housing in their area is unaffordable, with aspiring owners the most concerned of any group surveyed.

Whether you’re buying, selling, or investing in Nova Scotia real estate, the most successful transactions start with a plan, not a reaction. If you’d like to talk strategy for the spring market, don’t hesitate to reach out.

Related Resources

- Nova Scotia Real Estate Market Statistics 2025

- Five Years of Nova Scotia Real Estate Market Analysis (2021-2025)

- Nova Scotia Real Estate Stats for November 2025

- Halifax-Dartmouth Real Estate Market Stats January 2026

- Truro-Bible Hill Real Estate Market Stats January 2026

- Bank of Canada Holds Overnight Rate at 2.25%

- Nova Scotia’s 2% Down Payment Program

- Spring 2026 in Halifax: Your Complete Guide

- Get Pre-Approved for a Mortgage

- What’s My Home Worth?

Five Years of Nova Scotia Real Estate Market Analysis

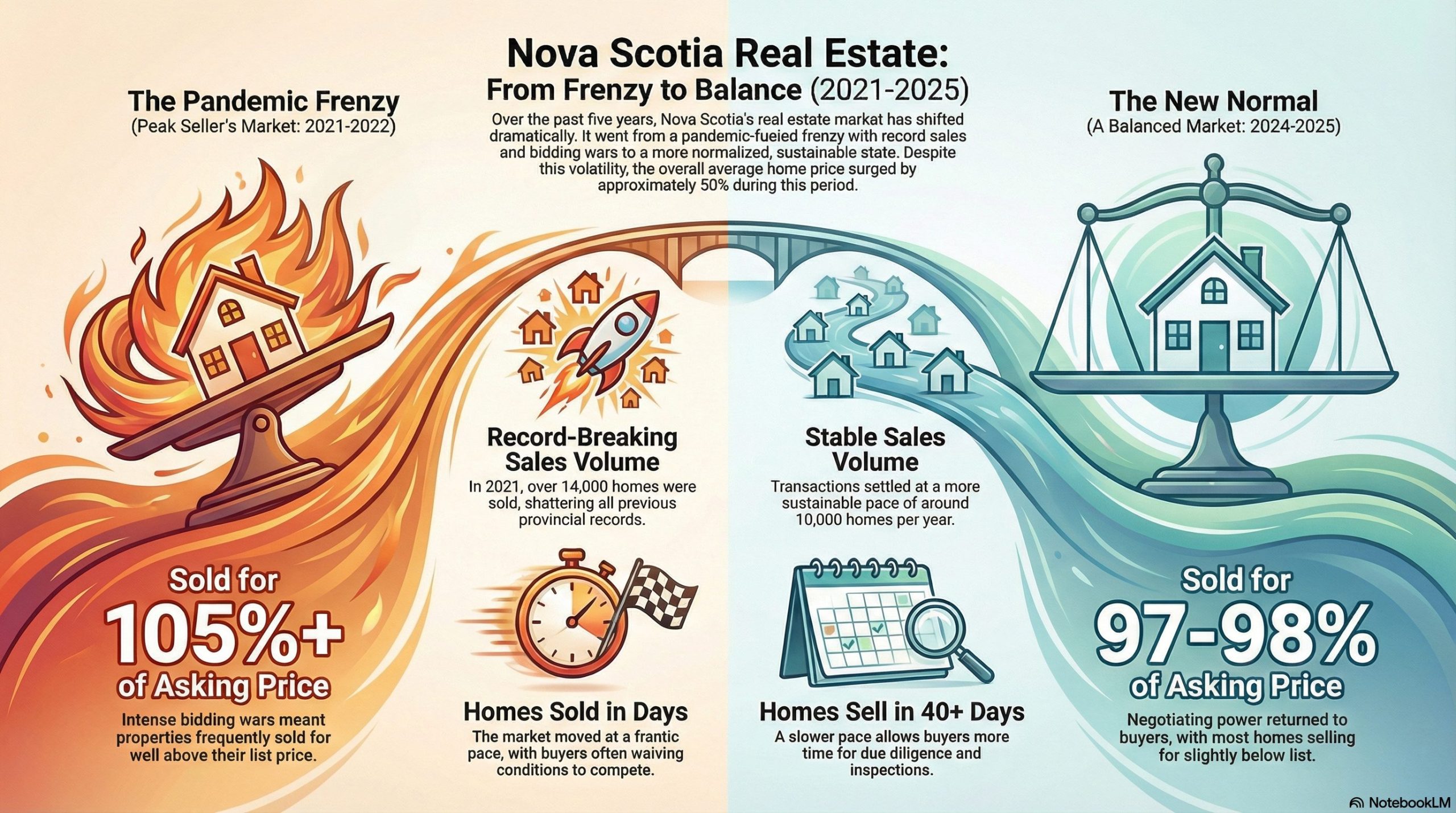

Five Years of Nova Scotia Real Estate Market Analysis: Transformation from (2021-2025)

By Rob Lough, Broker/Owner at Century 21 Optimum Realty

Nova Scotia’s residential real estate market has undergone a remarkable transformation over the past five years. From the pandemic-fueled frenzy of 2021 to today’s more balanced conditions, the province has experienced dramatic shifts in pricing, sales volume, and market dynamics. Interested in seeing the end of year market stats for 2025?

This comprehensive analysis examines the key trends that have shaped the market, providing valuable insights for both buyers and sellers navigating Nova Scotia’s evolving real estate landscape. For an even broader view, see our Ten Years of Nova Scotia Real Estate Market Analysisers.

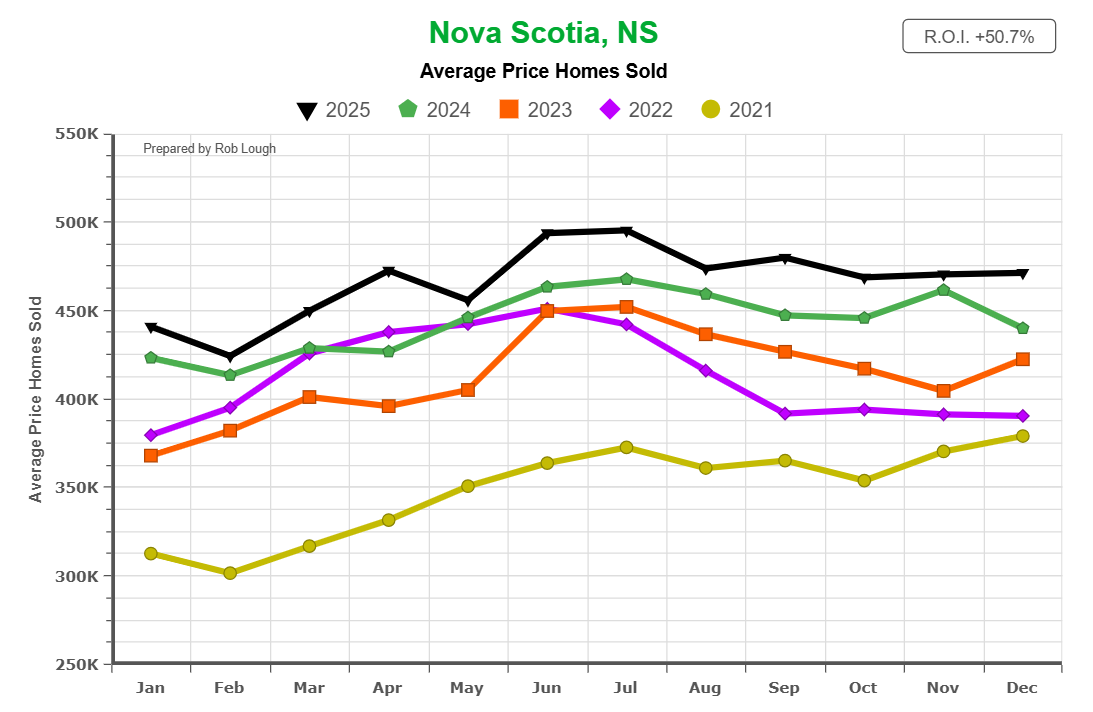

The most striking feature of Nova Scotia’s real estate market over the past five years has been the sustained price appreciation. Average home prices have surged approximately 50% since early 2021, transforming the province’s housing affordability landscape.

Nova Scotia average home sale prices by month 2021-2025 with 50.7% ROI showing steady price appreciation from $312K in 2021 to $485K in 2025

From the low $300,000s in January 2021, the average sale price has climbed to approximately $485,000 by the end of 2025. This represents a remarkable 50.7% return on investment for homeowners who purchased at the start of this period.

While price growth has moderated from the explosive gains of 2021–2022, values remain elevated. Year-over-year, 2025 prices are up roughly 5% from 2024 levels and nearly 40% above 2020 benchmarks. Despite higher mortgage rates and affordability concerns, the market has maintained its upward trajectory.

What This Means for Buyers: While prices remain significantly higher than five years ago, the pace of appreciation has slowed considerably. This creates a more sustainable market environment where buyers have time to make informed decisions without the pressure of rapid price escalation. However, waiting for substantial price corrections may not be a viable strategy, as the market has demonstrated resilience despite higher borrowing costs.

What This Means for Sellers: Homeowners who purchased in 2020 or earlier have seen exceptional equity gains. While the days of automatic multiple offers and above-asking sales are largely over, properly priced homes continue to sell at historically elevated values. The key is realistic pricing aligned with current market conditions rather than peak 2022 expectations.

Sales Volumes Normalize After Record-Breaking 2021

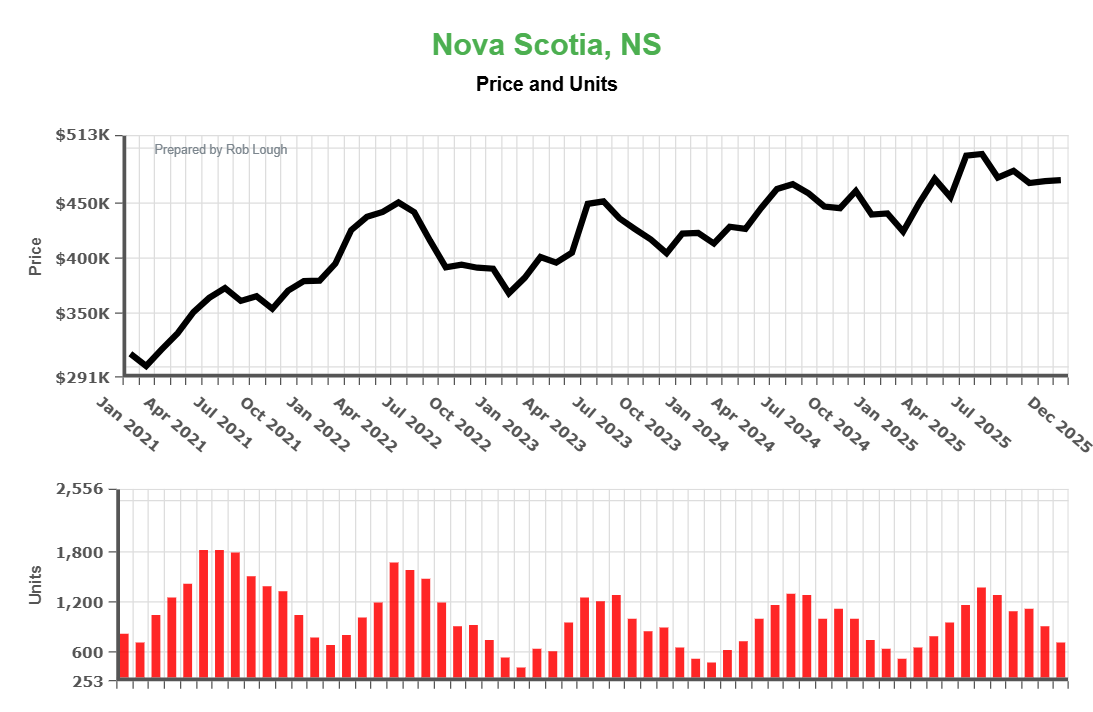

The pandemic era triggered unprecedented transaction volumes across Nova Scotia. In 2021, the province recorded over 14,000 residential sales, shattering previous records as buyers rushed to secure properties amid rock-bottom interest rates and lifestyle changes driven by remote work.

Nova Scotia average home prices and units sold 2021-2025 displaying price increase from $291K to $485K with inverse relationship between price growth and sales volume

However, the market cooled dramatically in 2022 and 2023 as the Bank of Canada implemented aggressive rate hikes. Sales volumes plummeted to their lowest levels since before the pandemic, with many potential buyers sidelined by reduced affordability and economic uncertainty.

By 2024-2025, transaction volumes stabilized at just over 10,000 units annually. While this represents a significant decline from 2021’s peak, it’s important to note that total dollar volume has remained robust due to higher average prices. The market has essentially traded quantity for quality, with fewer but more valuable transactions.

What This Means for Buyers: Lower transaction volumes indicate reduced competition compared to the frenzied conditions of 2021-2022. Buyers now have more time to conduct thorough inspections, negotiate terms, and make conditional offers. The return to more normalized sales volumes has shifted power back toward buyers after years of seller dominance.

What This Means for Sellers: With fewer buyers actively searching, sellers must be more strategic in their approach. Professional photography, competitive pricing, and proper marketing are no longer optional but essential. The days when any listing would generate immediate interest are over—homes must be well-presented and realistically priced to attract today’s more selective buyers.

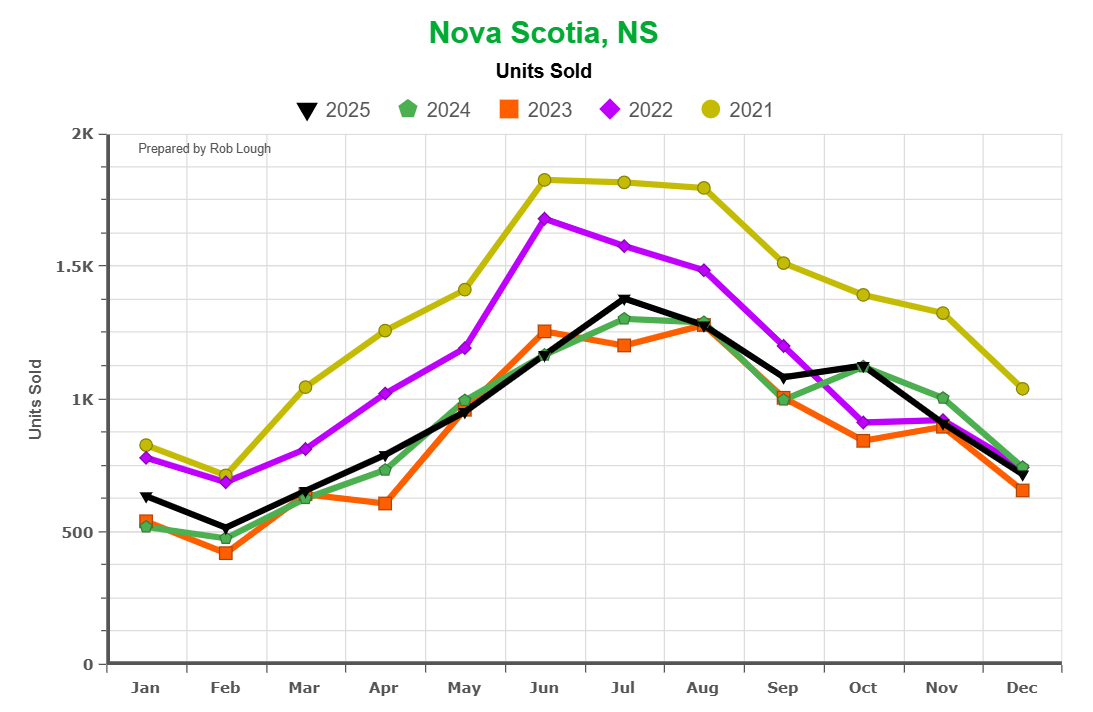

Traditional Seasonal Patterns Re-Emerge

One of the most notable developments in recent years has been the return of traditional seasonal patterns to the Nova Scotia market. During the pandemic boom of 2021, market activity remained elevated year-round, defying historical norms.

Nova Scotia monthly home sales by year 2021-2025 comparing seasonal patterns with peak sales in June-August and lowest activity in winter months

The data reveals strong seasonal peaks in late spring and summer across all five years, with 2021 showing the most pronounced spikes—often reaching 1,700-1,800 units per month. However, the seasonal amplitude has moderated in subsequent years as the market cooled.

Winter troughs have become more pronounced since 2022, particularly in January and February. This reflects the return to more rate-sensitive, deliberate buyer behavior rather than the year-round urgency that characterized the early pandemic period.

The traditional spring market has reasserted itself as the prime selling season, with buyers actively house-hunting as weather improves and families plan moves around the school calendar.

What This Means for Buyers: Strategic timing can provide advantages in today’s market. Shopping during the slower winter months may yield more negotiating leverage and less competition. Conversely, spring and summer offer the widest selection of available properties. Understanding these seasonal dynamics allows buyers to align their search strategy with their priorities—whether that’s selection or negotiating power.

What This Means for Sellers: Listing timing matters more now than during the pandemic boom. Properties listed in late winter or early spring typically benefit from pent-up buyer demand and face less competition from other sellers. However, sellers with flexibility should avoid listing during peak winter months unless they’re prepared for longer market times and potentially more aggressive negotiations.

Market Time Extends as Power Shifts

Perhaps no metric better illustrates the market’s transformation than average days on market (DOM). During the height of the pandemic boom in 2021-2022, well-presented homes often sold within days, sometimes with multiple offers on the same day of listing.

Nova Scotia average days on market 2021-2025 comparing years showing fastest sales of 20-30 days in summer 2022 to current 50-56 day average in 2025

Fast forward to 2025, and the picture has changed dramatically. Current data shows average DOM hovering in the high 40-day range—significantly longer than the frenzied early pandemic period but still reasonable by historical standards.

This extended market time reflects buyers’ restored ability to conduct thorough due diligence, compare multiple properties, and negotiate terms. The rushed, waive-all-conditions approach that defined 2021-2022 has given way to more conventional transaction timelines.

Complementing this trend, the average sold-to-ask ratio has drifted downward to the 97-98% range by late 2025. This represents a significant shift from 2021-2022 when properties routinely sold at or above asking price. Today’s market sees more conditional offers, fewer bidding wars, and greater scrutiny from increasingly selective buyers.

What This Means for Buyers: Extended market times and declining sold-to-ask ratios create opportunities for buyers to negotiate. Don’t be afraid to make offers below asking price on properties that have been listed for several weeks. Include standard conditions like financing and inspection, which are once again becoming the norm. Take time to conduct proper due diligence—the pressure to decide immediately has largely dissipated.

What This Means for Sellers: Realistic pricing has never been more critical. Overpriced homes sit on the market longer and often sell for less than they would have with competitive initial pricing. Work with your realtor to analyze recent comparable sales and price accordingly from day one. Be prepared to negotiate and accept reasonable conditions—the unconditional, above-asking offers of 2021-2022 are largely a thing of the past.

Market Value Remains Elevated Despite Volatility

While unit sales have declined from their 2021 peak, the total value of real estate transactions tells a more nuanced story. The monthly value of sales has remained relatively stable, fluctuating between seasonal highs and lows rather than showing sustained decline.

Nova Scotia real estate value of sales 2021-2025 showing monthly transaction volumes ranging from $150M to $750M with seasonal peaks in spring and summer

Peak months in 2022 saw transaction values exceeding $750 million, while even the slower periods of 2023-2025 typically generated $300-400 million in monthly sales. This consistency in dollar volume, despite lower unit sales, underscores how rising prices have offset declining transaction counts.

The data reveals a market that has shifted from high-volume, moderate-price transactions to lower-volume, high-price transactions. This evolution reflects both the maturation of Nova Scotia’s real estate market and the province’s ongoing challenge with housing affordability.

The Inverse Relationship: Prices Rise as Volume Falls

A striking feature of the past five years has been the inverse relationship between transaction volumes and average prices. As unit sales declined from their 2021 peak, prices continued their upward march with only brief plateaus.

Nova Scotia average home prices and units sold 2021-2025 displaying price increase from $291K to $485K with inverse relationship between price growth and sales volume

This pattern reflects a fundamental characteristic of Nova Scotia’s market: persistent demand meeting limited supply. Even as higher interest rates and reduced affordability pushed some buyers to the sidelines, the remaining pool of qualified buyers competed for a still-constrained inventory of available homes.

The province’s ongoing population growth, driven by both interprovincial migration and international immigration, has maintained upward pressure on prices even as transaction volumes normalized. This demographic tailwind shows no signs of abating, suggesting continued support for home values in the medium term.

Negotiating Power Returns to Buyers

The sold-to-ask ratio serves as an excellent barometer of negotiating leverage in any market. The five-year data reveals a clear evolution from extreme seller’s market conditions to today’s more balanced environment.

Nova Scotia average sold-to-ask ratio 2021-2025 showing decline from 112% peak in 2022 to 97-98% range in 2025 indicating return to balanced market conditions

In 2021 and 2022, the ratio frequently exceeded 105%, with peak months seeing properties sell for 107-112% of asking price. This reflected the bidding war environment where desperate buyers competed against multiple offers, often waiving conditions to secure properties.

By contrast, 2024 and 2025 have seen ratios stabilize in the 97-98% range. Properties are selling, but generally at slight discounts to asking price. This normalized ratio indicates that sellers are pricing optimistically (as they traditionally do) and buyers are successfully negotiating reductions during the transaction process.

The return to sub-100% ratios represents one of the most significant shifts in market dynamics. It signals that buyers have regained negotiating leverage after years of being price-takers in a seller-dominated market. However, the fact that ratios remain above 95% suggests the market hasn’t swung to a buyer’s market in the extreme sense—rather, it has achieved a more balanced equilibrium.

What This Means for Buyers: The current sold-to-ask environment favors buyers who do their homework. Make offers based on comparable sales and property condition, not just asking price. Most properties are selling for 2-3% below asking, so don’t be intimidated by list prices. Use professional home inspections and appraisals as negotiating tools if issues emerge. The key is to be reasonable but assertive in your offers.

What This Means for Sellers: Gone are the days of pricing 10% above market value and still receiving above-asking offers. Today’s successful sellers price at or slightly above recent comparable sales, not the peak values from 2022. Remember that your asking price is the starting point for negotiations, and most deals close at 97-98% of list. Price strategically to attract buyer interest while leaving minimal room for negotiation.

Looking Ahead: A Stable, Mature Market

As we move into 2026, Nova Scotia’s real estate market presents a dramatically different landscape than the frenzied conditions of just four years ago. The transformation from seller’s market to balanced conditions represents a return to normalcy after an unprecedented pandemic-era boom.

Several factors support continued market stability:

Ongoing population growth through interprovincial migration and immigration continues to drive housing demand across the province. Nova Scotia remains one of the fastest-growing provinces in Canada, with new residents attracted by relative affordability, quality of life, and economic opportunities.

Interest rates have stabilized after the aggressive hiking cycle of 2022–2023, with some economists predicting modest cuts in 2026. This could provide a modest boost to buyer affordability and transaction volumes without triggering another unsustainable boom. That price run has real consequences, new NSAR data shows 77% of Nova Scotians now consider housing unaffordable, even as 73% of non-owners say they still want to own.reased, it remains insufficient to fully address the housing shortage accumulated over decades of underbuilding.

The consensus forecast points to modest price appreciation of 2-4% annually over the next few years, with sales volumes likely remaining in the 10,000-11,000 unit range. This represents a healthy, sustainable market rather than the speculative environment of 2021-2022.

What This Means for Buyers: The current environment offers the best conditions for buyers since before the pandemic. Competition has eased, sellers are negotiable, and you can make informed decisions without artificial time pressure. However, waiting for significant price declines is likely a losing strategy, demographic trends and supply constraints suggest continued modest appreciation. If you’re financially prepared and have found the right property, current market conditions favor action over waiting.

What This Means for Sellers: While market conditions have moderated from the extreme seller’s market of 2021-2022, well-priced, well-presented homes continue to sell successfully. The key is adjusting expectations to current reality rather than peak pandemic conditions. Work with experienced real estate professionals who understand local market nuances, invest in proper staging and marketing, and price competitively from the start. The fundamental strength of Nova Scotia’s real estate market remains intact—it just requires more professional execution than the anything-sells environment of recent memory.

The Bottom Line

Nova Scotia’s real estate journey from 2021 to 2025 tells the story of a market that experienced extraordinary conditions and has gradually normalized into a sustainable equilibrium. Prices have risen approximately 50% over five years, unit sales have declined from record highs but stabilized at healthy levels, and market dynamics have shifted from extreme seller’s market to balanced conditions.

For buyers and sellers navigating today’s market, understanding these trends is essential for making informed decisions. The frenzied bidding wars and instant sales are gone, replaced by a more deliberate, traditional real estate environment where due diligence, strategic pricing, and professional representation matter once again.

Whether you’re considering buying your first home, comparing a condo to a house, trading up to accommodate a growing family, or selling to downsize or relocate, the current market offers opportunities for those who approach it with realistic expectations and sound strategy. At Century 21 Optimum Realty, we’re committed to helping you navigate Nova Scotia’s evolving real estate landscape with expert guidance tailored to your unique circumstances.

Ready to buy or sell in Nova Scotia? Contact the experienced team at Century 21 Optimum Realty for expert guidance tailored to your unique real estate goals.

Related Resources

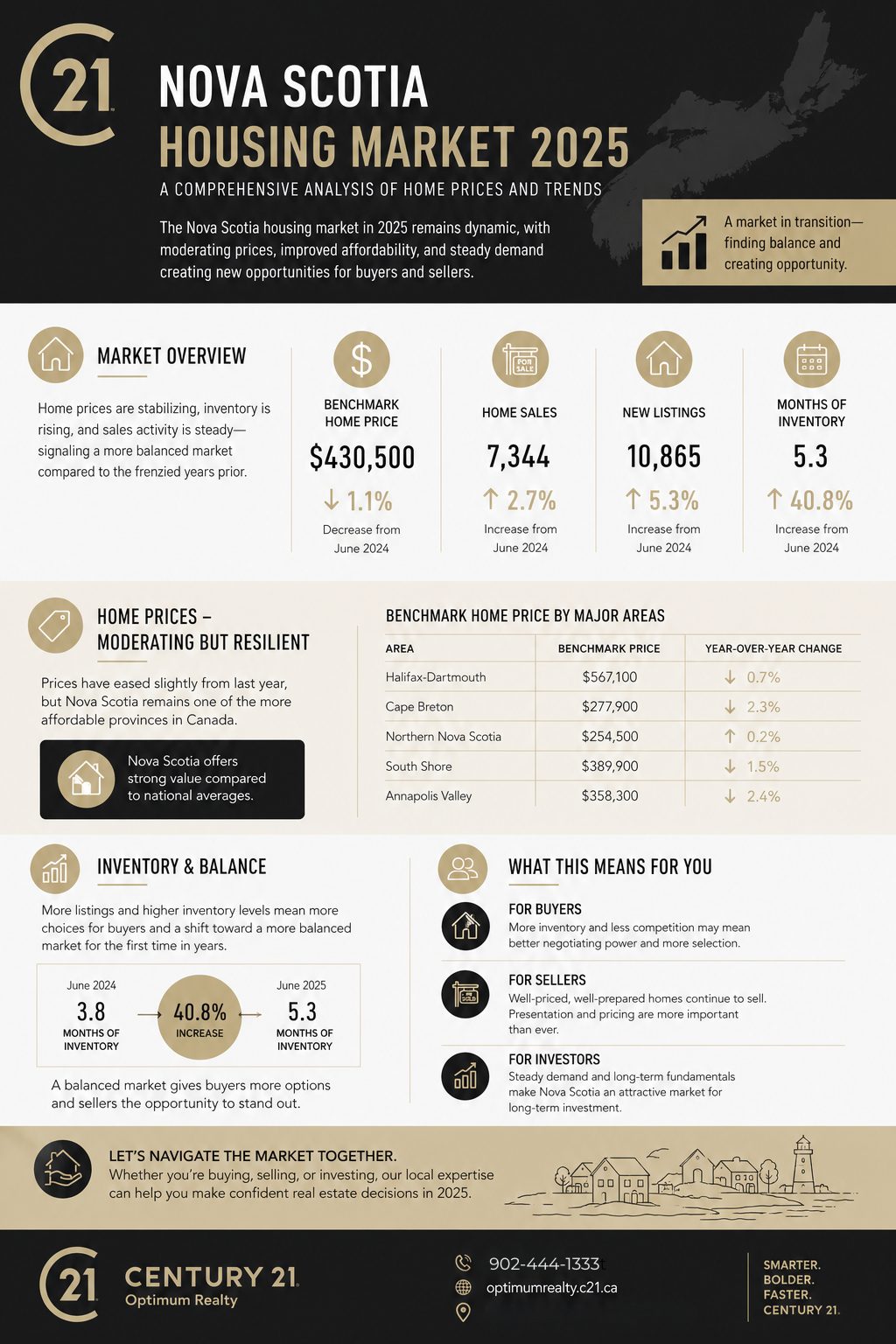

- Nova Scotia Housing Market 2025: A Comprehensive Analysis of Home Prices and Trends

- Ten Years of Nova Scotia Real Estate Market Analysis

- Nova Scotia Real Estate Market Statistics 2025: A Year of Transition

- Canadian Real Estate 2025: Why Nova Scotia’s Housing Market Outshines Major Cities

- Halifax Real Estate Market Insights: 4 Surprises

- Halifax & Bedford Housing Boom

- Nova Scotia Real Estate Market Stats – January 2026

Nova Scotia Real Estate Stats for November 2025

Nova Scotia Real Estate Stats for November 2025

As 2025 draws to a close, it’s time to take stock of Nova Scotia’s real estate market performance over the past twelve months. The data tells a compelling story of seasonal rhythms, strong price growth, and a market that’s finding its sustainable pace after years of pandemic-era volatility.

Total Sales Volume: Classic Seasonal Pattern Emerges

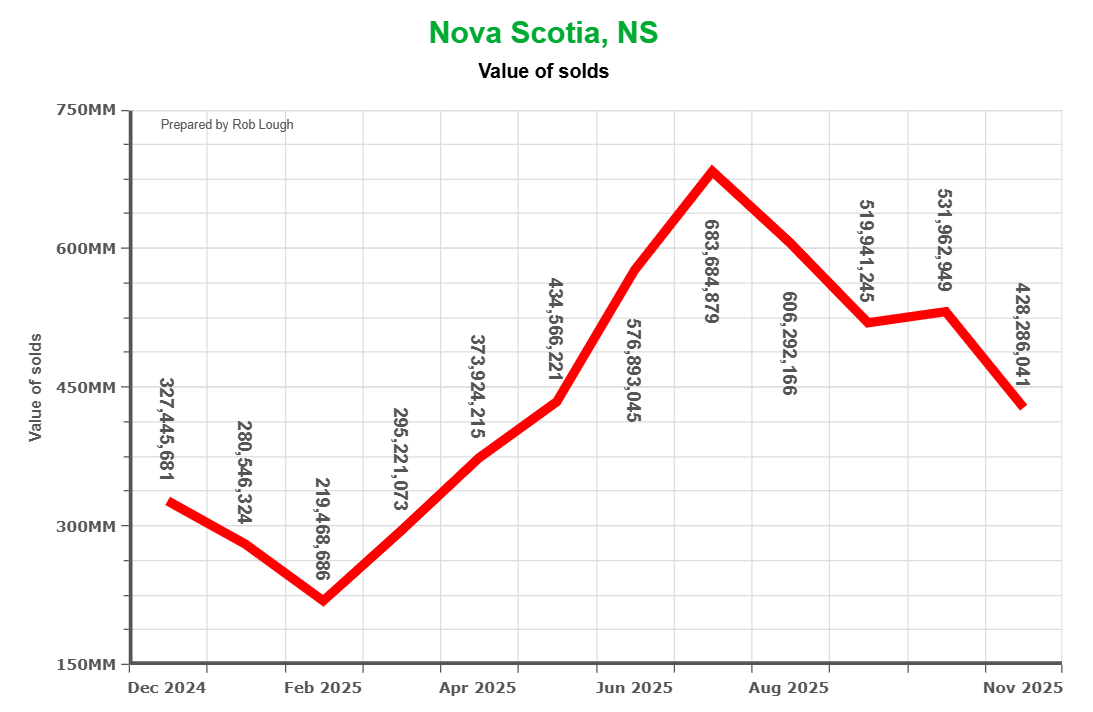

Nova Scotia Real Estate Stats November 2025 value of sold

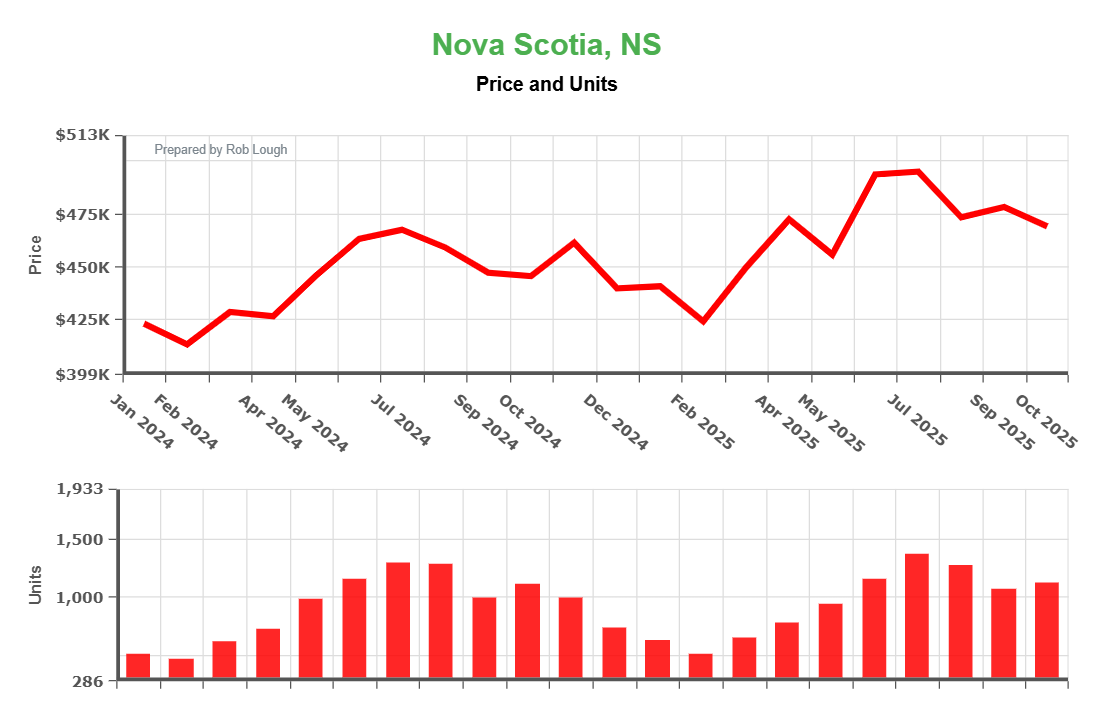

The total dollar volume of real estate transactions followed a predictable arc throughout the year. Starting at $327 million in December 2024, the market hit its lowest point in February at just $219 million, a typical winter trough reflecting harsh weather and post-holiday financial caution.

Spring brought renewed energy, with March climbing to $295 million and April surging to $373 million. The market peaked in midsummer, with July recording an impressive $683 million in transactions, more than triple the February low. This summer surge accounted for a disproportionate share of annual activity, with May through August consistently exceeding $500 million monthly.

As expected, fall brought gradual cooling. By November, monthly sales had settled back into the mid-$400 million range at $428 million. While down from summer highs, this represents healthy ongoing activity and demonstrates the market’s underlying strength heading into winter. This pattern aligns with our October 2025 market analysis, which showed clear seasonal transitions taking hold.

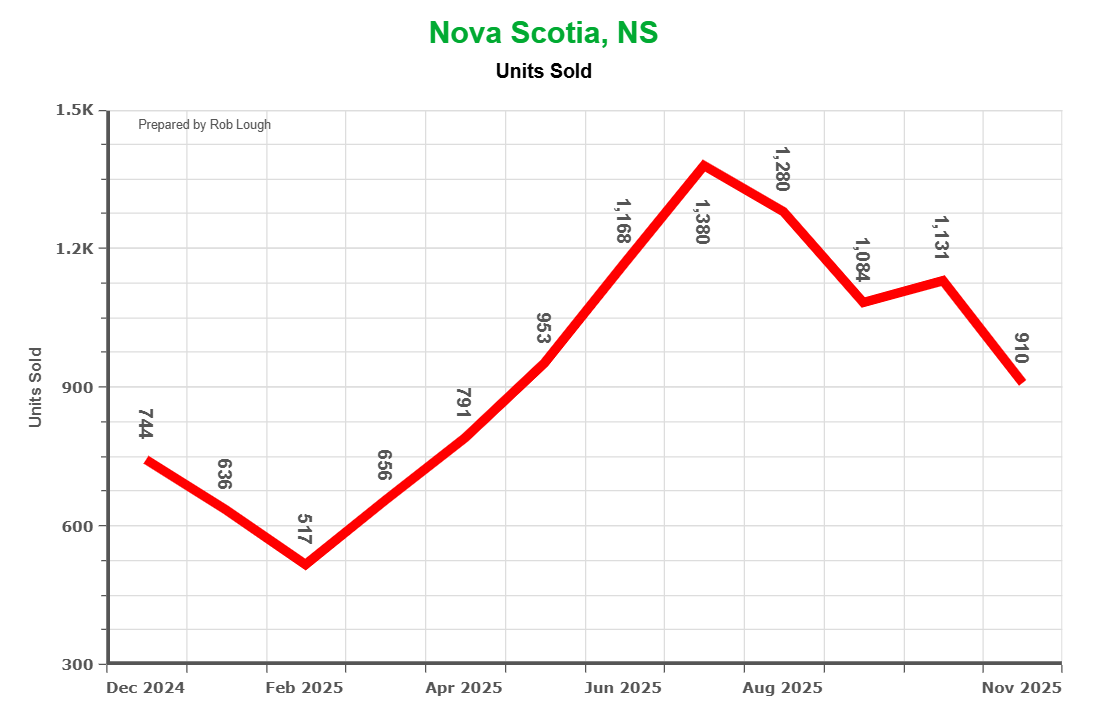

Units Sold: Summer Dominance Clear

Nova Scotia Real Estate Stats for November 2025 Units Sold

The number of homes changing hands mirrored the dollar volume pattern. February’s winter low of 517 units sold gave way to steady spring acceleration, with April recording 791 sales and May jumping to 953 transactions.

Summer delivered peak activity: June reached 1,168 sales, July hit the annual high at 1,390 units, and August maintained momentum with 1,280 transactions. These four months (May through August) accounted for more than 40% of annual sales, underscoring how critical proper timing is for sellers looking to maximize exposure and competition.

The fall cooldown was orderly rather than abrupt, with September recording 1,084 sales, October at 1,131, and November closing at 910 units. These figures remained well above winter lows, suggesting continued buyer confidence and healthy market fundamentals.

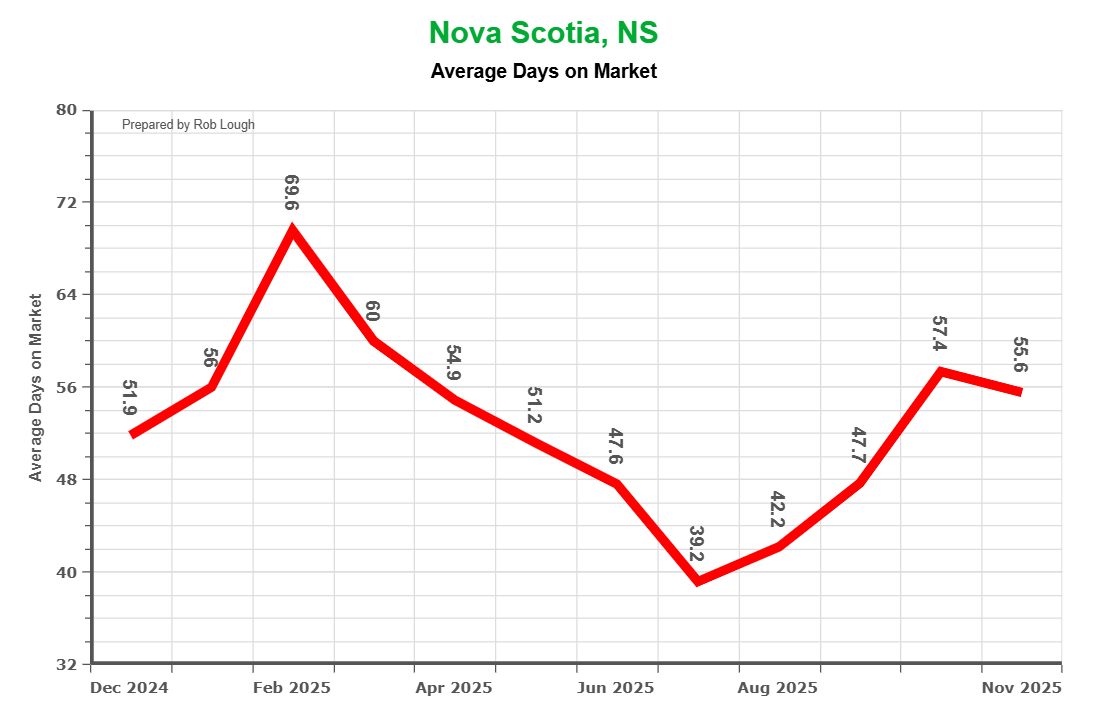

Average Days on Market: Speed Varies Dramatically by Season

Nova Scotia Real Estate Stats for November 2025 Average Days on Market

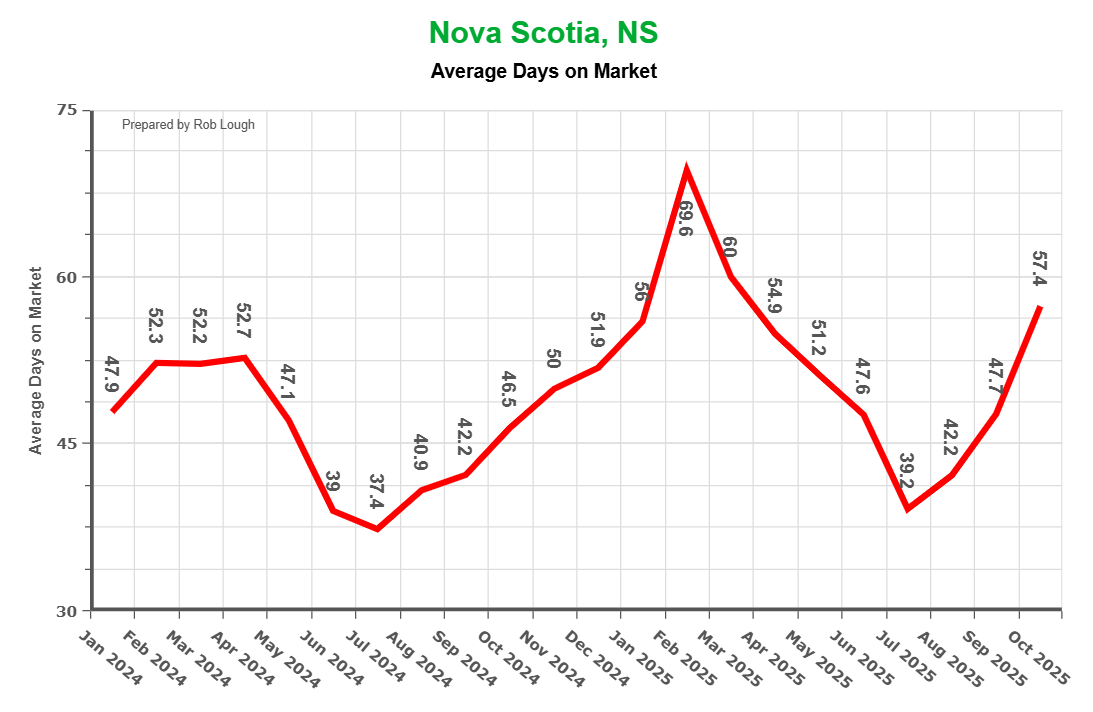

Days on market proved highly seasonal, starting at 51.9 days in December and spiking to the year’s slowest point in February at 69.6 days. This winter peak reflects reduced buyer urgency, weather challenges, and limited inventory turnover.

The market accelerated through spring, improving to 60 days in March and 54.9 days by April. Summer brought the fastest conditions: June averaged 47.6 days, while July hit the year’s low at just 39.2 days, a true seller’s market where well-priced homes received multiple offers quickly.

Fall saw gradual lengthening: September at 47.1 days, October extending to 57.4 days, and November at 55.6 days. This represents a healthy middle ground, faster than winter but without summer’s frenzy, creating balanced conditions for both buyers and sellers.

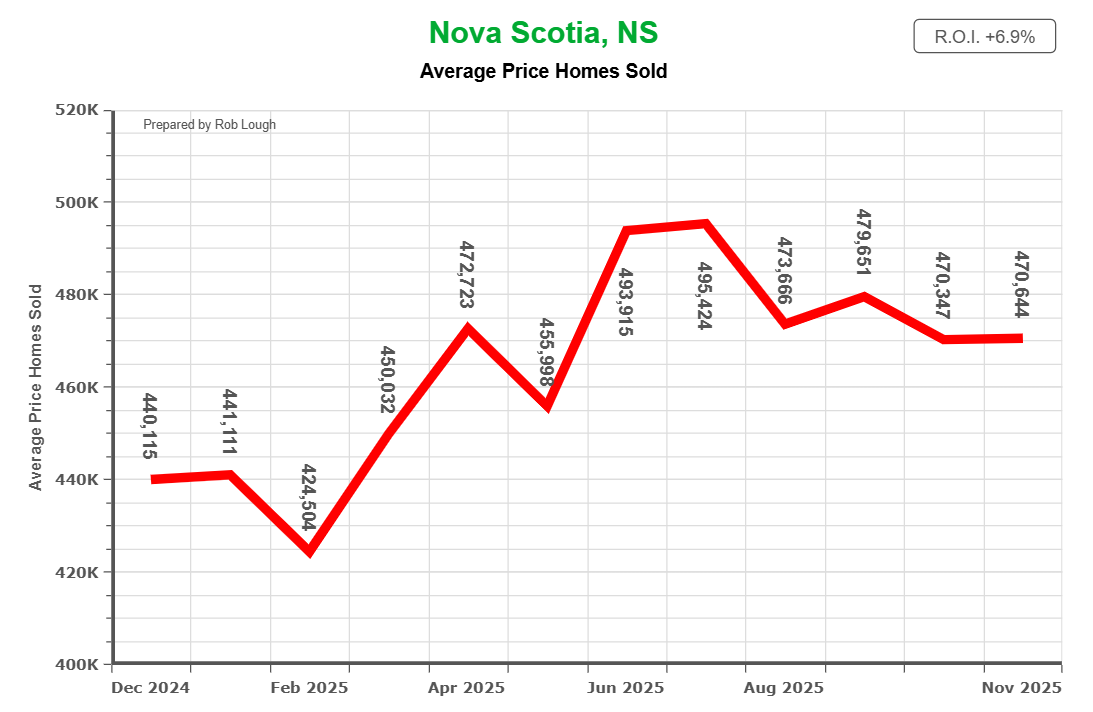

Average Home Prices: Strong 6.9% Annual Growth

Nova Scotia Real Estate Stats for November 2025 Average Price of Homes Sold

Perhaps the year’s most significant story is the steady price appreciation. Average home prices started in the low-$440,000 range in December 2024, dipped briefly to $424,500 in February during the winter slowdown, then began climbing through spring.

April marked a breakthrough as prices surged to $472,723, and summer saw averages flirting with the $500,000 mark. July peaked at $495,424, while prices remained elevated through August at $473,666. Fall brought stabilization rather than decline, with September through November holding steady in the high-$470,000 range. This growth continues the upward trajectory detailed in our comprehensive 2025 Nova Scotia housing market analysis.

The year-over-year return on investment of 6.9% represents substantial value creation for homeowners, well above inflation and most traditional investments. Starting near $440,000 and finishing around $470,000 demonstrates that Nova Scotia real estate continues rewarding long-term holders while maintaining relative affordability compared to larger Canadian markets.

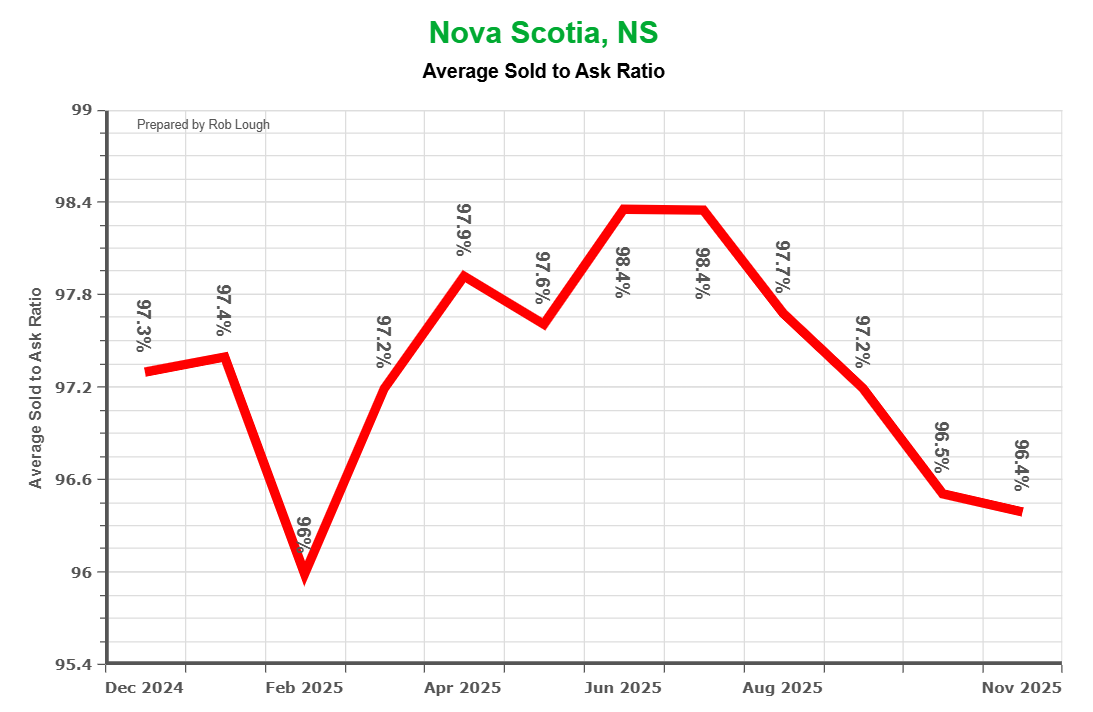

Sold-to-Ask Ratio: Sellers Maintain Strong Pricing Power

Nova Scotia Real Estate Stats for November 2025 Average Sold to Ask Ratio

The sold-to-ask ratio remained impressively consistent throughout the year, fluctuating only between 96% and just under 99% of listing prices. This tight range demonstrates market health, realistic pricing strategies, and strong underlying demand.

Even during the winter slowdown, sellers averaged better than 96% of asking prices. February’s 96% represented the year’s low point but still indicated limited buyer leverage. Spring and summer brought peak seller power, with April through July consistently achieving 97.5% to 98.4% of asking prices, suggesting multiple-offer situations became common during peak season.

Fall saw modest easing to the 96.5% range by November, giving buyers slightly more negotiating room as competition decreased. However, the fact that sellers still achieved better than 96% of asking prices year-round demonstrates the continued strength and balance in Nova Scotia’s housing market.

Market Context and Long-Term Trends

The 2024 to 2025 data reveals a market that has found its sustainable rhythm after years of pandemic-driven volatility. The clear seasonal patterns, winter slowdown, spring surge, summer peak, and fall moderation, represent a return to historical norms that benefit market stability. As highlighted in our analysis of why Nova Scotia’s housing market outshines major Canadian cities, the province continues benefiting from strong interprovincial migration while offering better value than markets like Toronto or Vancouver.

Nova Scotia continues benefiting from strong interprovincial migration, expanding job opportunities in technology and healthcare, and relative affordability compared to larger Canadian markets. These fundamentals support ongoing demand even as the market transitions from the frenzy of recent years to more measured growth.

Takeaway for Buyers and Sellers

For Buyers: Winter and early spring offer the best negotiating conditions, with fewer competing buyers and more time for due diligence. However, inventory selection is limited. Summer provides maximum choice but intense competition. Fall represents the sweet spot, decent inventory without summer’s frenzy, making it ideal for buyers who can move quickly when they find the right property. Getting mortgage pre-approved before shopping is essential in any season to strengthen your negotiating position.

For Sellers: The data strongly supports late spring and summer listing strategies when possible. Properties listed from May through August benefit from maximum buyer activity, fastest sale times, and strongest pricing power. Those who must sell during off-peak periods should price competitively and expect longer marketing times, though the consistently high sold-to-ask ratios suggest properly priced homes sell well year-round. Learn more in our seller’s guide.

Note for investors: If you’re considering investment properties, be aware of the significant OSFI mortgage rule changes coming in January 2026, which will fundamentally alter qualification requirements for investment property mortgages.

The Nova Scotia real estate market has demonstrated remarkable resilience and growth over the past year. With 6.9% price appreciation, healthy transaction volumes, and clear seasonal patterns, the market is positioned well heading into 2026. Whether you’re buying your first home, upgrading for a growing family, or preparing to downsize, understanding these trends helps you make informed decisions in Atlantic Canada’s dynamic housing market.

OSFI’s 2026 Mortgage Changes

OSFI’s 2026 Mortgage Changes: The Real Impact on Canadian Real Estate Investors

If you’re a real estate investor in Canada, January 2026 marks a turning point. The Office of the Superintendent of Financial Institutions (OSFI) is implementing new mortgage qualification rules that will fundamentally change how you build and manage your investment portfolio. These aren’t minor adjustments, they’re game-changing regulations that will affect everything from your acquisition strategy to your refinancing options.

Let’s dive into exactly how these changes will impact you as an investor and what you need to do about it.

The Core Change That Affects Every Investor

At the heart of OSFI’s new framework is one critical shift: the end of income leverage across multiple properties.

Until now, you’ve been able to use your personal income and existing rental income as a combined qualification tool across your entire portfolio. Earning $100,000 a year with three rental properties generating $4,000 monthly? You could use that full income picture to qualify for property number four, five, and beyond.

Starting January 2026, that strategy dies.

Each investment property mortgage must now qualify independently, standing on its own financial merit. Your personal employment income can help you qualify for one property. After that? Every additional investment property must qualify based primarily on its own rental income, period.

This isn’t just a policy tweak. It’s a complete restructuring of how investment property financing works in Canada.

Your Acquisition Strategy Just Got Complicated

Let’s talk about what this means for buying additional properties.

The Math That No Longer Works

Previously, you could build a portfolio like this:

Property 1: Qualified using your $90K personal income plus $1,500/month rental income

Property 2: Qualified using that same $90K income plus rental income from both properties ($3,000/month total)

Property 3: Qualified using your $90K income plus all portfolio rental income ($4,500/month total)

Under the new rules, here’s how it works:

Property 1: Qualifies using your $90K personal income plus its $1,500/month rental income

Property 2: Must qualify using ONLY its own $1,500/month rental income (your $90K is already “used”)

Property 3: Must also qualify using ONLY its own $1,500/month rental income

See the problem? Properties 2 and 3 need to generate enough rental income on their own to cover their mortgage payments, property taxes, insurance, condo fees, and pass debt service ratio tests, without any help from your personal income or income from other properties.

What This Means for Property Selection

You’ll need to become significantly more selective about which properties you acquire. Here’s what matters now:

Cash flow becomes non-negotiable. Properties that barely break even or require you to subsidize them monthly? They won’t qualify under the new rules. You need properties generating substantial positive cash flow that can clearly cover all expenses independently.

Purchase price relative to rent matters more than ever. Markets with high rent-to-price ratios become far more attractive. If you’re looking at a $500,000 condo that rents for $2,000/month, the math probably doesn’t work. But a $400,000 duplex generating $3,200/month? That might qualify.

Location strategy needs recalibration. You might need to shift away from high-appreciation, low-yield markets (like some parts of Toronto or Vancouver) toward markets where rental income is stronger relative to purchase prices, think certain neighborhoods in Halifax, Moncton, or areas of Alberta and Saskatchewan.

Property type considerations change. Single-family homes with basement suites, duplexes, or multi-unit properties that generate higher rental income relative to purchase price become more valuable from a financing perspective.

Your Portfolio Growth Timeline Just Extended

Here’s an uncomfortable truth: building a large portfolio is going to take significantly longer for most investors.

The Slowed Scaling Reality

Under the previous system, an investor with strong income and good credit could potentially acquire 3 to 5 properties within 18 to 24 months by leveraging their income and growing rental income across applications. It was aggressive, but achievable.

Under the new rules, that timeline extends dramatically. Between acquisitions, you’ll need to:

Build additional personal capital since you can’t leverage your income across properties

Wait for existing properties to appreciate to potentially use equity (though even that comes with new challenges)

Generate or save substantial down payments for each property independently

Find properties with exceptional cash flow that meet the strict independent qualification requirements

Realistically, many investors should expect to acquire one property every 2 to 3 years rather than multiple properties per year. That’s not necessarily bad, it encourages more sustainable growth, but it’s a significant shift from what’s been possible.

The End of Aggressive Leverage Strategies

Popular leverage-based strategies face serious challenges:

The Traditional Leverage Play: Buy property, build equity, refinance to pull out down payment for next property, repeat. This still technically exists, but remember, when you refinance, that property must still qualify independently under the new rules. If it can’t generate enough rental income on its own to support the new, larger mortgage, the refinance doesn’t happen.

The Income Snowball: Use growing rental income from multiple properties to qualify for increasingly expensive properties. This strategy relied entirely on income aggregation, which is now prohibited. Each new property starts from zero in terms of qualification.

The Portfolio Leverage Approach: Present lenders with your entire portfolio’s strong performance to secure better terms on new acquisitions. While portfolio strength might help with relationship lending decisions, it can’t be used for qualification calculations under the new framework.

The Refinancing Challenge You’re Not Thinking About

Here’s where many investors are going to get blindsided: existing properties coming up for renewal or refinancing.

When Your Current Strategy Collides With New Rules

Let’s say you bought three properties between 2020 and 2024, qualifying for each using your combined income and portfolio rental income. Those mortgages were approved under the old rules.

When those mortgages come up for renewal between 2025 and 2029, you’ll face the new qualification standards. If you want to:

Refinance to access equity

Switch lenders for better rates

Adjust mortgage terms significantly

Each property must now prove it can qualify independently. Properties that were marginal on cash flow when you bought them, counting on appreciation or subsidizing from your income, might not qualify for refinancing under the new rules.

Your Options When Refinancing Gets Difficult

If you have properties that won’t qualify independently, you have limited choices:

Stay with your current lender: At renewal, if you don’t make changes to the mortgage size or terms, many lenders will simply renew without full re-qualification. You might not get the best rate, but you maintain financing. However, you’re essentially locked in with that lender until you can improve the property’s financial position.