Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Rising Mortgage Rates and the Bank of Canada’s Next Move: What Canadian Homeowners Need to Know

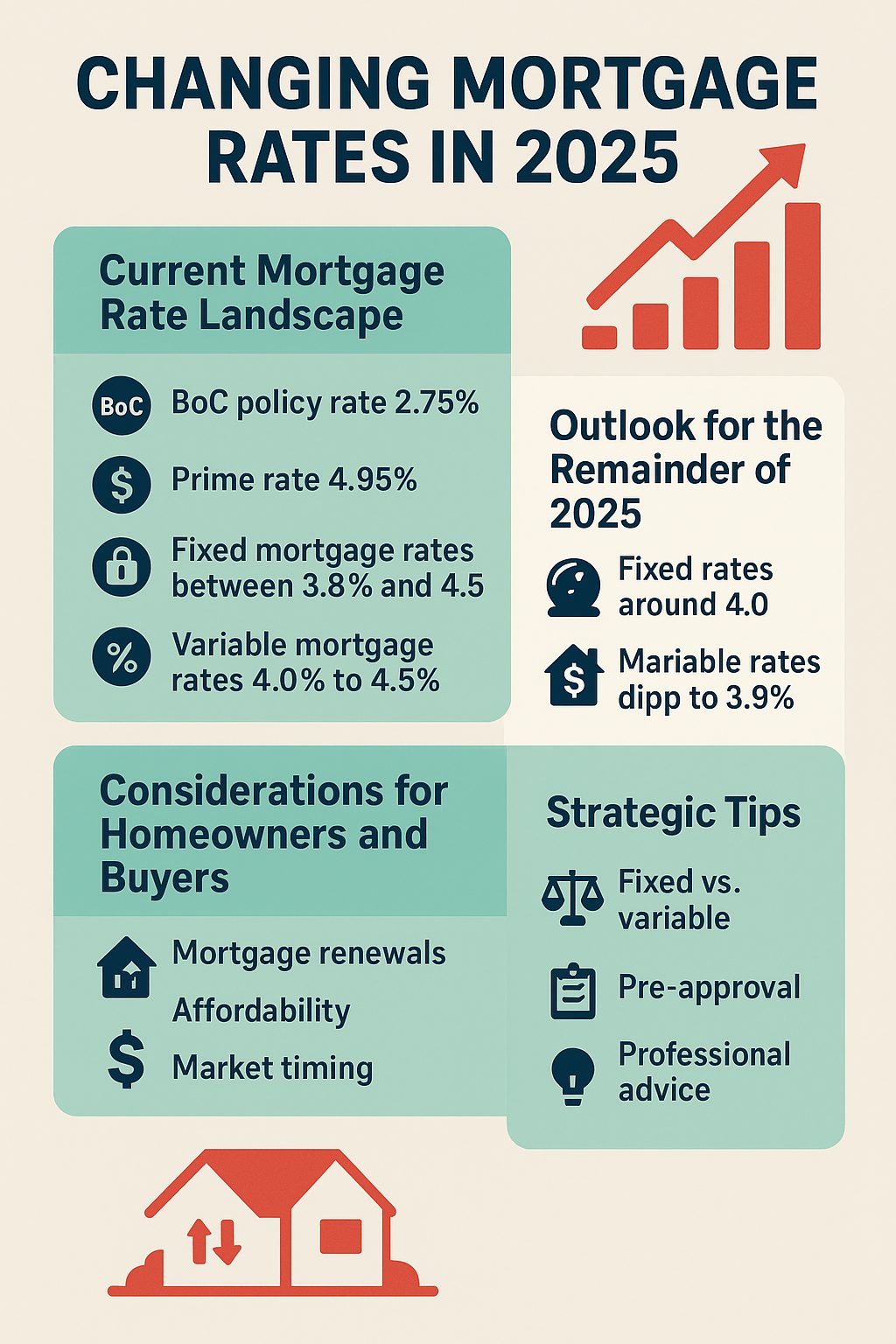

Canadian mortgage rates are rising while the Bank of Canada prepares its next rate decision. Learn what homeowners and buyers need to know about changing mortgage rates in 2025. Homebuyers and homeowners across Canada are navigating a shifting mortgage landscape as fixed mortgage rates climb and the Bank of Canada prepares for its next critical rate decision. With bond yields rising and lenders adjusting their strategies, understanding these changes is essential for making informed financial decisions.

Why Canadian Fixed Mortgage Rates Are Rising

Lenders Respond to Market Pressures

Canadian lenders have begun raising fixed mortgage rates after months of competitive pricing. This significant shift stems from several key factors:

- Higher bond yields directly impact fixed-rate mortgage costs

- Global inflation concerns affecting international lending markets

- Central bank caution worldwide signaling tighter monetary policy

- Reduced lender competition as aggressive pricing strategies wind down

The end of ultra-low fixed mortgage rates means Canadian borrowers face a new reality. Those seeking new mortgages or approaching renewal dates may encounter rates significantly higher than recent years, directly impacting monthly payment calculations.

Impact on Borrowing Costs

For mortgage shoppers, the most competitive rates that defined 2024 are becoming harder to find. This rate environment particularly affects:

- First-time homebuyers stretching affordability limits

- Homeowners with upcoming mortgage renewals

- Investors considering real estate purchases

- Those planning to refinance existing mortgages

Bank of Canada Rate Decision: What to Expect

Steady Policy Rate Likely

Despite rising fixed rates in the broader market, the Bank of Canada is expected to maintain its key overnight rate at the upcoming policy meeting. Several economic indicators support this measured approach:

Positive Economic Signals:

- Stronger-than-expected Canadian economic growth

- Resilient consumer spending patterns

- Stable employment levels

- Controlled inflation trends

Variable Rate Mortgage Stability

If the Bank of Canada holds rates steady, variable-rate mortgage holders can expect:

- No immediate payment changes on existing mortgages

- Continued affordability compared to fixed-rate options

- Stability amid market volatility

- Time to assess long-term mortgage strategies

Strategic Implications for Canadian Homeowners

Fixed-Rate Mortgage Holders

Homeowners with fixed-rate mortgages approaching renewal should prepare for potentially higher costs. Key considerations include:

- Review renewal timeline and current rate environment

- Explore early renewal options if beneficial

- Compare lenders for competitive offerings

- Consider switching to variable rates if appropriate

New Home Buyers

Prospective buyers face increased monthly payment obligations compared to earlier periods. Important factors include:

- Budget adjustment for higher mortgage costs

- Down payment strategies to reduce borrowing needs

- Pre-approval timing to secure current rates

- Market timing considerations

Variable-Rate Mortgage Holders

Current variable-rate borrowers enjoy short-term stability but should monitor:

- Future Bank of Canada decisions and economic indicators

- Payment shock preparation for potential rate increases

- Conversion options to fixed rates if needed

- Stress testing financial capacity for rate changes

Housing Market Outlook and Predictions

Market Cooling Expected

Higher mortgage rates typically influence housing market dynamics through:

- Reduced buyer affordability limiting demand

- Price stabilization in overheated markets

- Inventory increases as fewer buyers compete

- Regional variations based on local economic conditions

Economic Fundamentals Provide Support

Despite rate pressures, several factors may support housing market stability:

- Strong employment levels maintaining buyer confidence

- Population growth driving housing demand

- Limited housing supply in key markets

- Economic diversification supporting regional markets

Expert Recommendations for Canadian Homeowners

Immediate Action Steps

- Review current mortgage terms and renewal dates

- Monitor rate trends and Bank of Canada communications

- Assess financial capacity for higher payments

- Explore mortgage options with qualified professionals

Long-Term Planning Strategies

- Build payment flexibility into household budgets

- Consider mortgage acceleration during stable periods

- Maintain emergency funds for economic uncertainty

- Stay informed about policy changes and market trends

Professional Mortgage Guidance

Given the complexity of current mortgage markets, consulting with qualified mortgage professionals becomes increasingly valuable. Experienced advisors can help with:

- Rate comparison across multiple lenders

- Strategy development for individual circumstances

- Risk assessment for different mortgage products

- Timing optimization for renewals and purchases

Conclusion: Navigating Canada’s Changing Mortgage Landscape

Canadian mortgage markets are experiencing significant transitions as fixed rates rise and monetary policy remains cautious. While the Bank of Canada’s measured approach provides some stability for variable-rate borrowers, the overall trend suggests higher borrowing costs ahead.

Homeowners and prospective buyers must stay informed, plan strategically, and seek professional guidance to navigate these changes successfully. By understanding market dynamics and preparing for various scenarios, Canadians can make confident mortgage decisions despite economic uncertainty.

Stay updated on Bank of Canada announcements and mortgage rate trends to make the most informed decisions for your financial future.

For personalized mortgage advice and current rate information, consult with a licensed mortgage professional in your area.