Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

How Nova Scotia First-Time Buyers Can Stack Federal and Provincial Programs to Make New Construction More Affordable

By Rob Lough, Broker/Owner | Century 21 Optimum Realty | Halifax-Dartmouth, Nova Scotia Published: March 2026

Buying a brand-new home in Nova Scotia has never come with more government support than it does right now. Between a new federal GST rebate, provincial down payment programs, and changes to mortgage rules, first-time buyers of new construction have access to a combination of tools that can meaningfully lower the cost of getting into the market. That gap is backed by data, a 2026 NSAR survey found 77% of Nova Scotians say housing is unaffordable, while 73% of non-owners still want to own someday.

The challenge for most buyers is that these programs exist in different places, administered by different levels of government, and rarely explained together in one place. This article does exactly that. Think of it as your plain-language guide to understanding every major program available to you, how each one works independently, and how they stack together to improve your overall affordability picture.

Start With the Biggest New Tool: The Federal GST Rebate Under Bill C-4

The most significant recent change is the passage of Bill C-4, the Making Life More Affordable for Canadians Act, which received Royal Assent on March 12, 2026. This legislation amends the Excise Tax Act to create an enhanced GST rebate specifically for first-time buyers of new homes.

Here is the core of how it works:

The program removes the 5% federal GST (or the federal portion of HST) on qualifying new homes priced up to $1,000,000. On a home priced at $1,000,000, the maximum federal savings are approximately $50,000. Between $1,000,000 and $1,500,000, the benefit phases out proportionally. Above $1,500,000, the enhanced rebate disappears.

To be eligible, the home must be new construction or substantially renovated, not a resale property. The Agreement of Purchase and Sale with the builder must be dated on or after March 20, 2025, and before 2031. You must occupy the home as your primary residence and be the first occupant after construction is complete.

For buyers in HRM, this matters a great deal. A large share of new-build townhomes and condos across Halifax Regional Municipality are priced under $1,000,000, putting the full rebate within reach for many local first-time buyers, not just buyers in Toronto or Vancouver.

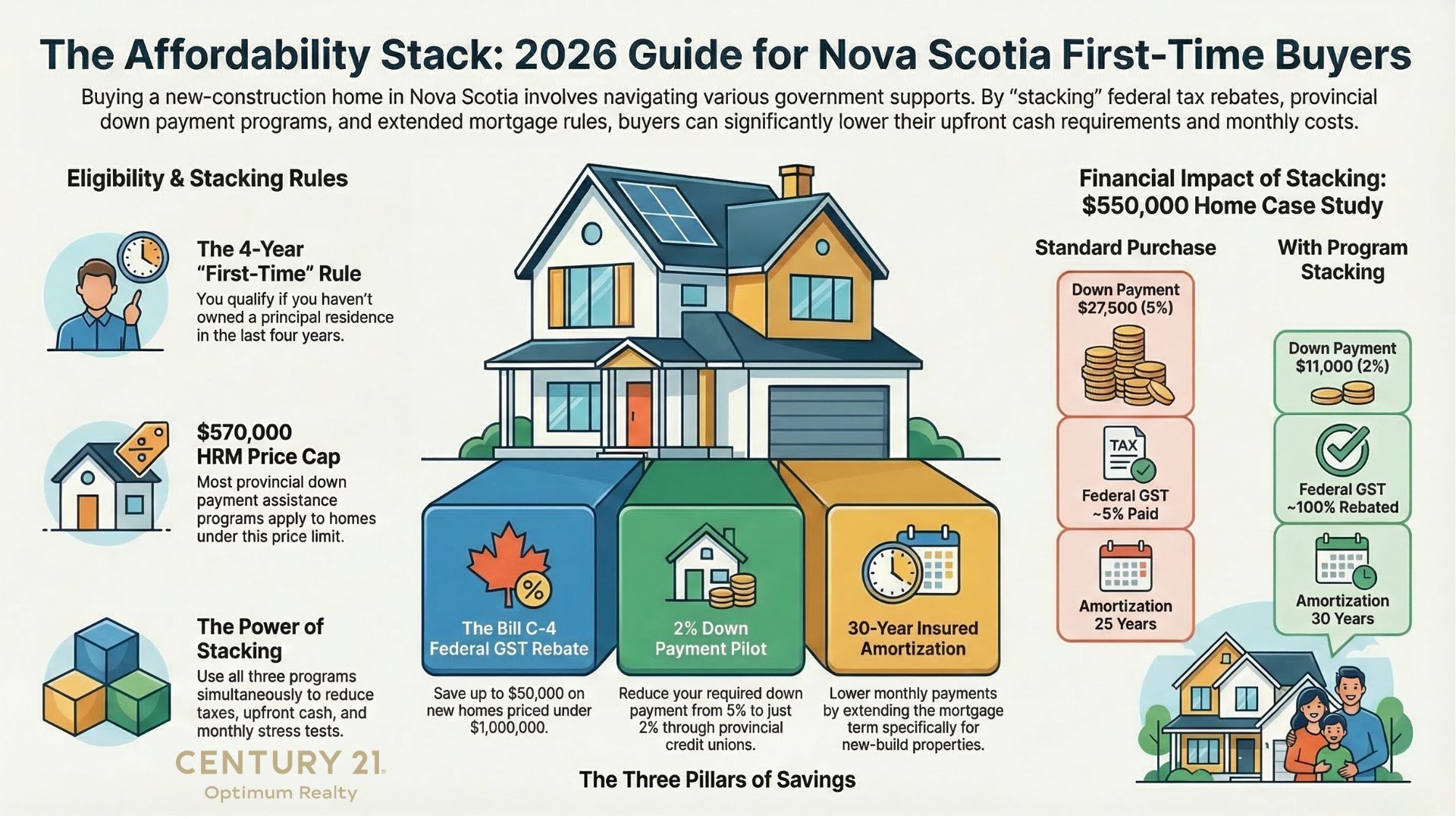

Understanding the Eligibility Test for “First-Time Buyer”

Before layering programs, it helps to understand what “first-time buyer” means under federal rules, because not all programs use identical definitions.

Under the federal framework, a first-time buyer is generally someone who has not owned a home used as their principal residence at any time during the preceding four years. There is also a provision for buyers who have gone through a separation or divorce, which may allow them to qualify even if they previously owned a home with a former spouse. You can read more about how that works in the context of Nova Scotia programs at the Century 21 Optimum Realty listings and resources page.

The important takeaway is that first-time buyer status is not just for people who have never owned anything. It is worth reviewing your personal history carefully, especially if you owned a home that was sold more than four years ago.

Layer Two: Nova Scotia’s 2% Down Payment Program

The second tool available to qualifying buyers is Nova Scotia’s First-Time Homebuyers Program, a provincial pilot that allows eligible buyers to purchase a home with as little as a 2% down payment, backed by a provincial guarantee. Under standard rules, most buyers need at least 5% down, which on a $500,000 home means $25,000 in cash. Under this program, that drops to $10,000, potentially shaving months or years off the time it takes to save enough to buy.

The program is delivered through participating credit unions in Nova Scotia. There is no traditional CMHC mortgage default insurance required, which eliminates a cost that would otherwise be added to the mortgage amount for high-ratio purchases.

Eligibility requirements include being a Nova Scotia resident, meeting the first-time buyer definition, passing a standard mortgage stress test, and staying within purchase price limits. In HRM and East Hants, the maximum eligible purchase price is $570,000.

The full details are covered in the Nova Scotia 2% Down Payment Program explainer on the C21 Optimum site.

Key point for stacking: This program applies to the purchase price, not the GST component. A buyer using the 2% down program on a new build under $570,000 could potentially access both the reduced down payment and the federal GST rebate on the same transaction, subject to meeting all eligibility criteria for each.

Layer Three: Nova Scotia’s Down Payment Assistance Program

Separate from the 2% pilot, Nova Scotia also has a Down Payment Assistance Program (DPAP) administered directly by the province. This program provides an interest-free loan of up to 5% of the purchase price to qualified buyers who cannot afford the down payment on their own.

The price cap in HRM is $570,000. Buyers must be first-time purchasers, the home must be their primary residence, and they must not already have the financial means to cover the 5% requirement independently.

The Nova Scotia Down Payment Assistance Program overview walks through the specific documentation requirements, application timelines, and eligibility rules in full detail.

Layer Four: The 30-Year Insured Amortization for New Builds

On top of the rebate and down payment programs, federal mortgage rule changes now allow first-time buyers of new construction to extend their insured mortgage to a 30-year amortization, up from the standard 25 years.

Why does this matter? A longer amortization reduces your monthly mortgage payment, which can make a real difference in whether you pass the mortgage stress test and how much home you can afford. The reduction in monthly payments does mean you pay more interest over the life of the loan, so it is a trade-off worth discussing with your mortgage broker, but for buyers whose primary hurdle is qualifying, it is a meaningful tool.

This rule is specifically available to first-time buyers purchasing new builds, not resale homes, which makes it particularly relevant to anyone considering the types of new construction projects where the Bill C-4 GST rebate would also apply.

Layer Five: The Nova Scotia Budget and HST Relief for New Rental Construction

The 2026-27 Nova Scotia provincial budget also introduced HST relief for developers building new multi-unit rental housing. While this does not directly benefit individual first-time buyers, it is worth understanding because it will gradually increase the supply of new-build units across HRM and surrounding areas, which affects pricing and availability over time.

The full breakdown of the 2026-27 Nova Scotia Budget housing measures covers all the supply-side programs in detail.

How These Programs Work Together: A Practical Example

Consider a qualifying first-time buyer purchasing a new-build townhome in HRM for $550,000:

Under Bill C-4, the full 5% GST on the $550,000 purchase price could be rebated. That is approximately $27,500 returned to the buyer, either credited by the builder at closing or claimed directly from CRA.

Under the 2% Down Payment Program, that same buyer could enter with $11,000 down instead of $27,500, freeing up capital for closing costs, moving expenses, or an emergency fund.

With a 30-year insured amortization, the monthly payment on the resulting mortgage is lower than it would be under the standard 25-year term, potentially improving stress-test qualification.

None of these programs replace each other. They address different parts of the affordability challenge: one reduces the tax cost of the purchase, one reduces the cash required upfront, and one improves monthly payment qualification. When used together by an eligible buyer on an eligible property, the cumulative effect is substantial.

What Buyers Need to Do Next

Understanding the programs is step one. The practical steps that follow matter just as much.

Get pre-approved first. Before approaching any builder or making any offers, you need to know your budget with precision. Pre-approval also locks in your rate for 90 to 120 days while you search. The current market context, including price trends and what inventory looks like across the province, is covered in the Nova Scotia Real Estate Market Stats for January 2026.

Confirm your Agreement of Purchase and Sale date. The Bill C-4 rebate requires that your agreement with the builder be dated on or after March 20, 2025. If you are unsure whether your purchase qualifies, your lawyer or REALTOR can help you confirm.

Apply for DPAP at least two weeks before your financing deadline. The Nova Scotia Down Payment Assistance Program requires an application window before your offer goes firm. Missing this deadline means missing the program for that transaction.

Work with professionals who understand how these programs interact. A mortgage broker familiar with the provincial credit union 2% program, a real estate lawyer who understands CRA rebate mechanics, and a REALTOR who works in the new construction segment are all valuable on the same transaction.

Bold Buyer Takeaway

If you are a first-time buyer of new construction in Nova Scotia in 2026, you are operating in the most program-supported environment we have seen in years. The federal GST rebate is law, provincial down payment tools are active, and 30-year insured amortizations are available for new builds. No single program solves the affordability challenge on its own. Used together, they change the math significantly.

Ready to start the conversation? Contact us at Century 21 Optimum Realty for a no-obligation discussion about what these programs mean for your specific situation.

Related Resources

- Nova Scotia’s 2% Down Payment Program

- Nova Scotia Down Payment Assistance Program

- 2026-27 Nova Scotia Budget: Housing Measures Explained

- Nova Scotia Real Estate Market Stats January 2026

- Nova Scotia Housing Market 2025: Comprehensive Analysis

- Browse Current Listings

- Contact Century 21 Optimum Realty