Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Understanding the 2026 Mortgage Stress Test: Can You Qualify?

By Rob Lough, Broker/Owner — Century 21 Optimum Realty

If you’re planning to buy a home in Nova Scotia this year, the mortgage stress test is one of the first hurdles you’ll need to clear. It’s not a credit check or a property appraisal, it’s a math test designed to make sure you can still afford your mortgage payments if interest rates rise after you sign.

Here’s what you need to know before you start shopping.

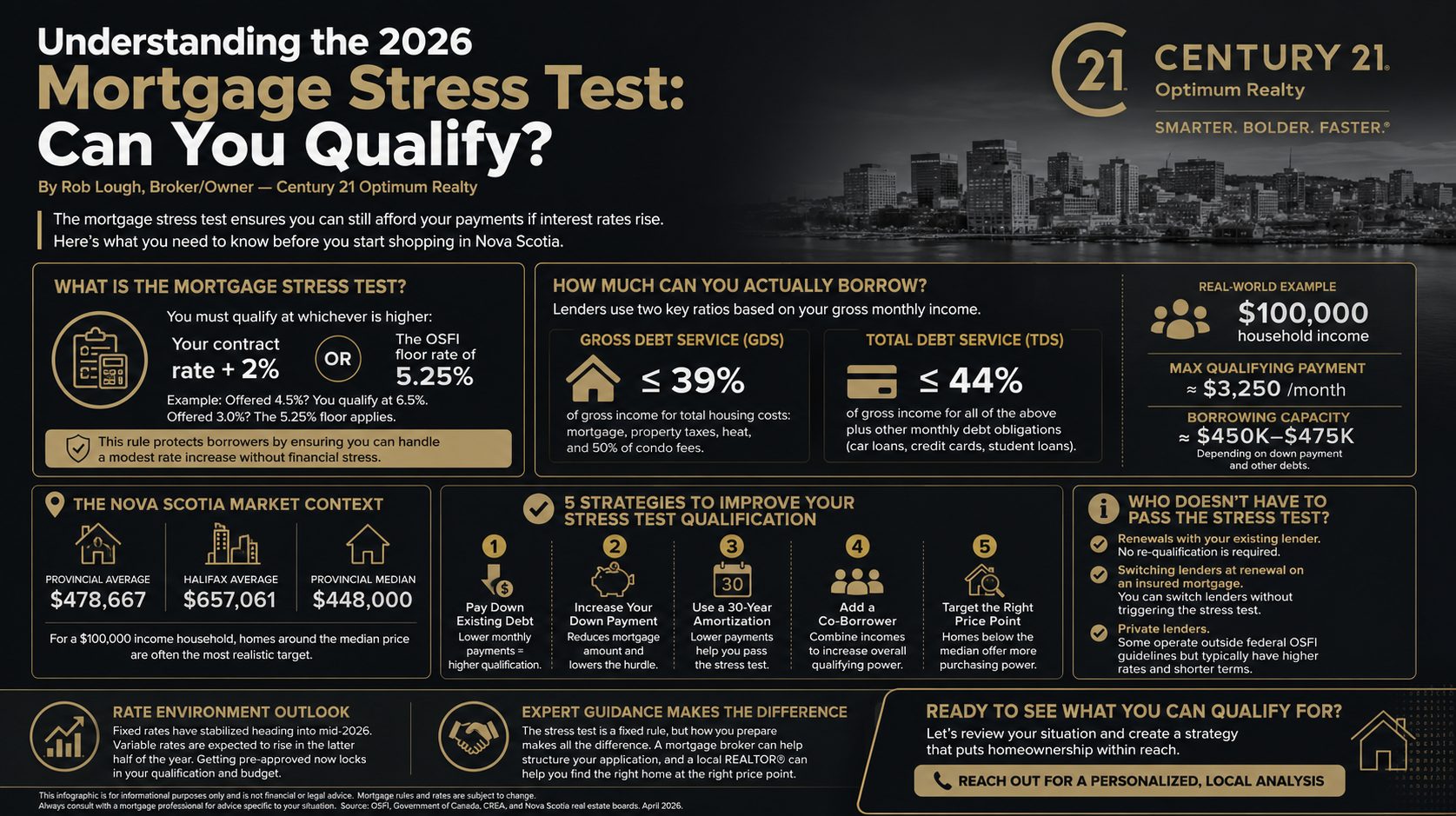

What Is the Mortgage Stress Test?

The stress test requires that you qualify for your mortgage at a higher rate than the one you’ll actually pay. Specifically, federally regulated lenders, banks, credit unions, and most mortgage companies, must qualify you at whichever is higher: your contract rate plus 2%, or the OSFI floor rate of 5.25%.

So if you’re offered a 4.5% fixed rate, you’ll need to qualify as if your rate is 6.5%. If rates were to drop and you secured a 3.0% rate, the 5.25% floor would apply instead.

This rule exists to protect borrowers, not to penalize them. The goal is to make sure you’re not stretched so thin that a modest rate increase forces a financial crisis. For a full look at what changed heading into 2026, see our article on OSFI’s 2026 Mortgage Changes.

How Much Can You Actually Borrow?

Two ratios govern how much a lender will approve you for:

Gross Debt Service (GDS): Your total housing costs, mortgage payment, property taxes, heat, and 50% of condo fees, cannot exceed 39% of your gross monthly income.

Total Debt Service (TDS): All of the above, plus your other monthly debt obligations (car loans, credit cards, student loans), cannot exceed 44% of your gross income.

Here’s a real-world example: On a household income of $100,000 per year, your maximum qualifying payment at the stress test rate works out to roughly $3,250/month. That typically translates to a borrowing capacity of approximately $450,000–$475,000, depending on your down payment and other debts.

Use our Mortgage Calculator to plug in your own numbers and see where you stand.

What This Means in the Nova Scotia Market

The stress test hits hardest in higher-priced markets and Halifax is exactly that.

The provincial average home price sits at $478,667. The Halifax average is $657,061. The median sale price across Nova Scotia is around $448,000 and that’s often where a household with a $100,000 income is realistically shopping.

For buyers with typical incomes, Halifax’s price point may require a larger down payment, a co-borrower, or a shift in search area. For full current pricing data across the province, see our Nova Scotia Real Estate Market Stats April 2026.

5 Strategies to Improve Your Stress Test Qualification

1. Pay Down Existing Debt

Your TDS ratio includes every monthly debt obligation. Eliminating $200/month in debt payments can increase your mortgage qualification by $30,000–$40,000. If you’re carrying a car payment or credit card balance you can realistically eliminate before applying, do it first.

2. Increase Your Down Payment

A larger down payment reduces the mortgage amount, which directly lowers the stress test hurdle. Nova Scotia buyers have access to two provincial programs worth knowing: the Nova Scotia 2% Down Payment Program and the Nova Scotia Down Payment Assistance Program, which offers a 5% interest-free loan for eligible buyers.

3. Use a 30-Year Amortization

First-time buyers now qualify for 30-year amortizations on insured mortgages. Spreading payments over 30 years lowers your monthly payment, which makes it easier to pass the stress test even at the qualifying rate. This stacks well with other programs, see How Nova Scotia First-Time Buyers Can Stack Federal and Provincial Programs for a full breakdown.

4. Add a Co-Borrower

Combining incomes is one of the most effective ways to increase qualifying power. Both applicants must pass the stress test individually, but the combined income and debt picture is what the lender uses to set the limit.

5. Target the Right Price Point

Sometimes the most practical move is adjusting where you’re shopping. Properties priced below the median ($448K) see more balanced competition, and areas outside HRM, offer significantly more purchasing power at equivalent income levels.

Who Doesn’t Have to Pass the Stress Test?

There are a few scenarios where the stress test doesn’t apply:

- Renewals with your existing lender. If you’re renewing and staying with the same lender, no re-qualification is required.

- Switching lenders at renewal on an insured mortgage. You can now switch lenders at renewal without triggering the stress test on insured mortgages, a meaningful change for many homeowners.

- Private lenders. Some private lenders and provincially regulated credit unions operate outside federal OSFI guidelines, though these typically come with higher rates and shorter terms.

For more on how renewal rules have changed, see our breakdown of New Mortgage Rules in Canada.

A Word on the Current Rate Environment

Fixed rates have stabilized heading into mid-2026, and variable rates are expected to see some upward movement in the latter half of the year. Getting pre-approved now locks in your qualification and gives you a defined budget before rate conditions shift.

For context on where rates have been and where they may be heading, our article Mortgage Rates Hit 3-Year Low: What This Means for Halifax Homebuyers provides useful historical perspective.

Working With the Right Team Matters

The stress test is a fixed rule, but how you position yourself before applying makes a significant difference. An experienced mortgage broker can help you time your application, structure your down payment, and identify which lender profile fits your situation.

On the real estate side, working with an agent who understands the local market means identifying properties that fit your real budget, not just your pre-approval ceiling. Browse our Buying & Selling Tips for more practical guidance, or reach out directly to talk through where you stand.

Related Resources