Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Nova Scotia’s 2% Down Payment Program: What First-Time Homebuyers Need to Know

By Rob Lough, Broker/Owner at Century 21 Optimum Realty

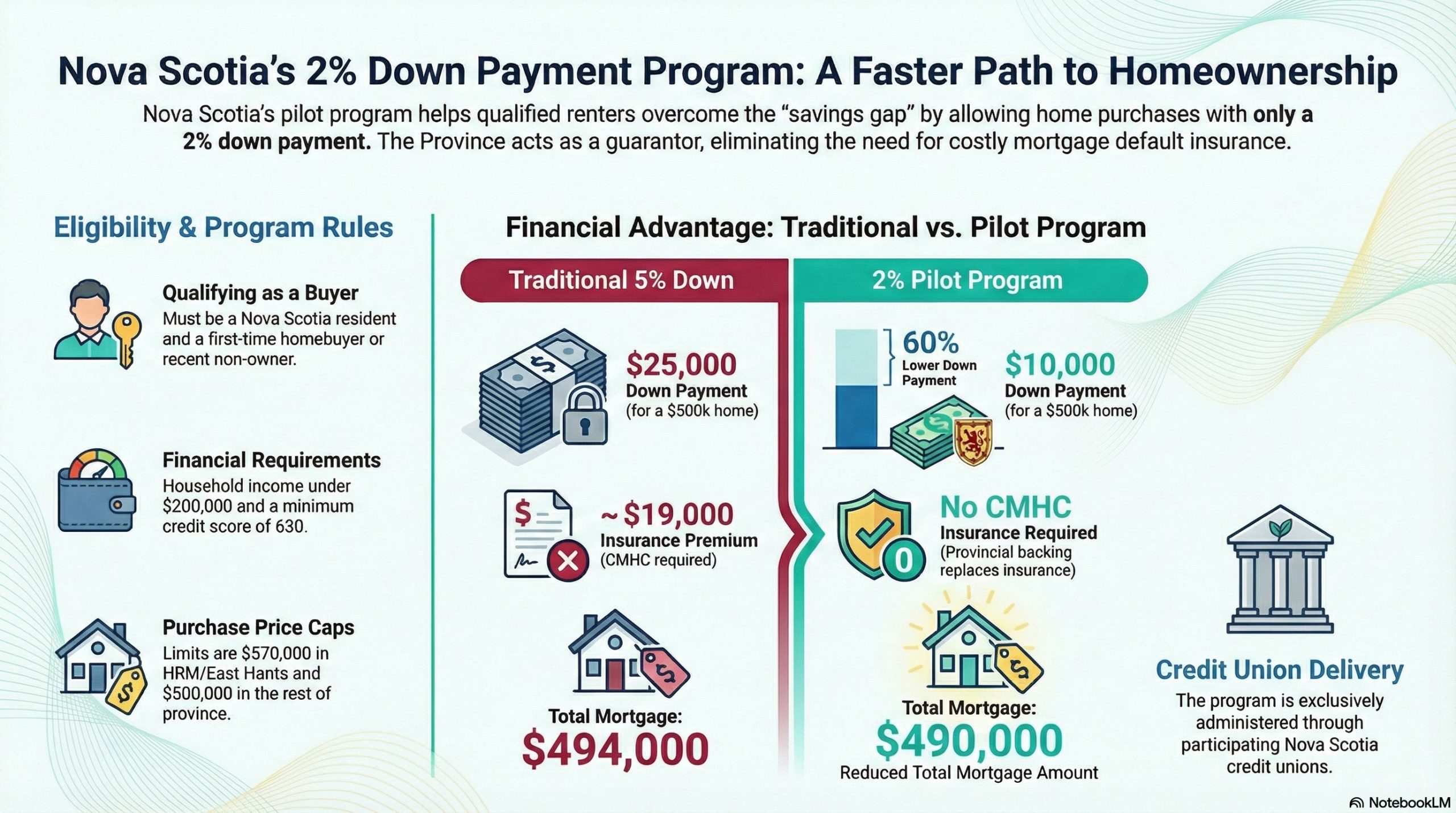

Saving for a down payment has become one of the biggest hurdles for renters ready to buy a home in Nova Scotia. While many qualified buyers can comfortably afford monthly mortgage payments, coming up with the traditional 5% down payment on a 500,000 home means finding 25,000 in cash—a tough ask when rental costs keep climbing and Nova Scotia home prices have risen steadily over the past several years.

The Province of Nova Scotia has launched a pilot program designed to tackle exactly this problem. The First-time Homebuyers Program allows qualified buyers to purchase with just 2% down, backed by a provincial guarantee that protects lenders and eliminates the need for traditional mortgage default insurance. It’s a gap that shows up clearly in new NSAR research on Nova Scotia housing affordability 73% of non-owners want to buy, but the upfront cash barrier is stopping them.

How the 2% Down Payment Works

Under standard mortgage rules, first-time buyers need at least 5% down on homes up to 500,000, and 5% on the first 500,000 plus 10% on any amount above that, up to the maximum insurable price of 570,000. For a 500,000 purchase, that’s 25,000 out of pocket.

With this new program, the same buyer would need just 10,000.

The program applies to purchase prices up to 570,000 in the Halifax Regional Municipality and East Hants, and up to 500,000 in the rest of Nova Scotia. The Province acts as guarantor for the mortgage, covering up to 90% of any shortfall if the home must be resold for less than the outstanding mortgage balance after a default.

Mortgages are delivered through participating credit unions across Nova Scotia, administered by Atlantic Central. If you want help finding suitable properties under these price caps, you can start by browsing our current listings or reviewing recent Nova Scotia market statistics to understand what’s available in your price range.

Who Qualifies for the Program

This isn’t a program for everyone—it’s targeted at buyers who are financially ready for homeownership but struggling with the upfront cash barrier.

Eligibility requirements include:

-

Must be a Nova Scotia resident and either a first-time homebuyer or someone who hasn’t owned a home in the last four years.

-

Combined household income of 200,000 or less.

-

Must pass the CMHC mortgage stress test to demonstrate ability to carry the mortgage.

-

Minimum credit score of 630.

-

Must be a Canadian citizen, permanent resident, or immigrant with a sponsorship letter from a Nova Scotia provincial immigration program.

-

Common-law partners can apply together if they’ve lived together at least 12 months, or are newlyweds.

The income cap and stress test requirement ensure that buyers can handle the monthly payments—this program tackles the savings gap, not long-term affordability. If you’re unsure whether you meet these criteria, a conversation with our team is a good first step—contact us anytime.

Financing Mechanics: No CMHC Insurance Required

One of the unique features of this program is that no separate mortgage default insurance is required, even though the down payment is well below the standard 20% threshold.

Normally, any mortgage with less than 20% down must carry CMHC insurance (or insurance from another approved provider), with the premium added to the mortgage amount or paid upfront. That premium can add thousands of dollars to the total cost.

Under the First-time Homebuyers Program, the Province’s guarantee effectively replaces that insurance layer. If a borrower defaults and the home sells for less than the mortgage balance, the Province covers 90% of the lender’s loss.

Key financing details:

-

Down payment: 2% from the buyer.

-

Interest rate capped at prime plus 2% maximum.

-

Administered through participating credit unions via Atlantic Central.

This structure keeps costs down for buyers while protecting lenders from excessive risk. If you’d like guidance on how this compares to the traditional insured mortgage route, our buyer services can walk you through both options, and our article on OSFI’s 2026 mortgage changes provides additional context on the lending environment.

Real-World Example: Cash Needed to Close

Let’s compare what it takes to buy a 500,000 home under traditional financing versus this new program.

Traditional 5% Down:

-

Down payment required: 25,000

-

CMHC insurance premium (approximate): 19,000

-

Total mortgage amount: 494,000

-

Cash needed at closing: 25,000 plus legal fees and other closing costs

2% Down Payment Program:

-

Down payment required: 10,000

-

No mortgage insurance premium

-

Total mortgage amount: 490,000

-

Cash needed at closing: 10,000 plus legal fees and other closing costs

For a qualified buyer, that’s 15,000 less cash required upfront—potentially shaving months or years off the time it takes to save enough to buy your first home. You can also compare these numbers with broader Nova Scotia housing market statistics for 2025 to see how prices and affordability have been shifting.

Why the Province Created This Program

The First-time Homebuyers Program is part of Nova Scotia’s broader Our Homes, Action for Housing plan, which the government says has exceeded all targets in its first two years and created conditions for more than 68,000 new housing units.

Housing starts are up 36% over the past two years, but the Province recognized that building more homes is only part of the solution. Many renters are “struggling to save the down payment to buy a new home,” according to the program announcement, even when they’re otherwise financially ready.

Atlantic Central, the organization administering the program on behalf of participating credit unions, describes the target group as people who are “capable, responsible and ready for homeownership, but who need the right support to take that next step.” If you want to understand how this fits into broader market trends, you can also explore our latest Nova Scotia market analyses and Nova Scotia market statistics for January 2026.

For a national or policy-level lens, you may also find it helpful to read our article on Canada’s government housing strategy and what it means for Nova Scotia.

Is This Program Right for You?

The 2% down payment option makes homeownership more accessible, but it’s not the right fit for every buyer. Here are a few things to consider:

This program works well if:

-

You have stable income and good credit but limited savings.

-

You’re spending a significant portion of your income on rent and struggling to save.

-

You can comfortably pass the mortgage stress test.

-

You’re planning to stay in Nova Scotia long-term.

You may want to explore other options if:

-

You’re close to saving a traditional 5% down payment.

-

Your income exceeds 200,000 as a household.

-

You don’t meet the residency or immigration requirements.

-

You’re concerned about carrying a higher mortgage balance relative to your home’s value.

It’s also worth noting that a smaller down payment means a larger mortgage, which translates to higher monthly payments and more interest paid over the life of the loan. Make sure you’re comfortable with the long-term commitment, and consider speaking with both your lender and a local REALTOR®—you can start with a no-obligation conversation with our team at C21 Optimum.

How to Apply

The First-time Homebuyers Program is delivered exclusively through participating credit unions in Nova Scotia. If you’re interested in applying, your first step is to connect with a participating credit union to discuss your eligibility and begin the pre-approval process.

As with any mortgage pre-approval, you’ll need to provide documentation of your income, employment, assets, debts, and credit history. The credit union will assess whether you meet the program’s requirements and can pass the stress test.

If you’d like support with the home search, offer strategy, and timelines that align with your financing approval, explore our buying resources and tips or reach out directly to get started with Century 21 Optimum Realty. You can also review our longer-term Nova Scotia real estate market analysis from 2021–2025 to see how this program fits into the bigger picture.

Frequently Asked Questions

Is Nova Scotia’s 2% down payment program worth it?

For many first-time buyers who are stuck renting because they can’t save 5% fast enough, this program can be worthwhile because it cuts the upfront cash needed almost in half while still giving access to standard mortgage rates through participating credit unions. The main trade-offs are that you must meet the program’s income, price cap, and credit union requirements, and you should be comfortable with homeownership costs right away rather than waiting longer to build a larger down payment cushion.

Does the 2% down payment program replace CMHC?

The program doesn’t replace CMHC as an institution, but in practice the Province’s guarantee fills the same risk‑management role that traditional mortgage default insurance would for these specific loans. Instead of paying a separate CMHC (or private insurer) premium on your mortgage, the lender relies on the provincial guarantee, which covers 90% of any shortfall if a borrower defaults and the home sells for less than the mortgage balance.

Is this the same as the Down Payment Assistance Program (DPAP)?

No, the new 2% down First-time Homebuyers Program is different from the existing Down Payment Assistance Program (DPAP). DPAP provides an interest‑free loan to help buyers top up their down payment to the usual minimum (for example 5%) and that loan is repaid separately over 10 years, while the 2% program changes the required minimum down payment itself and relies on a provincial guarantee rather than a separate down payment loan.

If you’d like, I can now tighten meta title/description and suggest specific H2/H3 refinements to align with “Nova Scotia 2% down payment program” and “First-time Homebuyers Program Nova Scotia” as your primary keywords.